The artificial intelligence (AI) market is maturing rapidly, which is perfectly normal. As I noted in a recent piece on the paradigm shift in AI stocks, we are likely exiting the phase of “blind faith” for good. The days of handing out blank checks for bold claims of a tech revolution have come to an end. Instead, investors are starting to demand hard numbers, real cash flows, and sustainable business models.

No catastrophic bubble burst is happening here — the technology works and delivers results. However, the valuation methodology itself is shifting.

In this new reality, looking at companies through the lens of future competition is absolutely vital. The macroeconomic law remains immutable. Aggregate demand has limits. Corporate AI budgets represent one giant pie, and it physically cannot be eaten three times by different vendors simultaneously.

Palantir Technologies (PLTR) possesses truly unique technology. That seems to be a hard fact. But PLTR stock trades at a massive premium that appears to have already priced in every conceivable success for decades to come. Today, the company's market capitalization exceeds $340 billion, while its trailing price-to-earnings (P/E) ratio has climbed to 240 times. The market prices this asset as if it will grow exponentially forever, assuming it will remain the absolute market leader in its specific niche.

But business does not exist in a vacuum. Palantir will likely enter a phase of brutal competition, and current multiples are completely unprepared for this scenario. Investors often miss the developmental dynamics of base AI models. What makes a product unique today might simply become a standardized feature within tech giants' ecosystems tomorrow. When that happens, such a lofty valuation risks proving mathematically unjustified.

Palantir’s Golden Window and the Illusion of the Gap

To understand why the market values Palantir so generously today, we need to acknowledge the company's current merits. Before the mass adoption of generative AI, Palantir's main superpower was Foundry and its ability to extract fragmented, chaotic data from various enterprise departments and stitch it into a single logical, semantic layer. This was heavy, almost manual engineering work.

The launch of the Artificial Intelligence Platform (AIP) became pure rocket fuel for Palantir. The algorithms perfectly layered over its existing stitched data architecture. If platform implementation previously took months and required complex integrations, machine learning accelerated the process exponentially. Clients started seeing results on the fly.

This caused a massive sensation in the commercial sector. The numbers don't lie. The dynamics of the final quarters of 2025 demonstrate solid business acceleration.

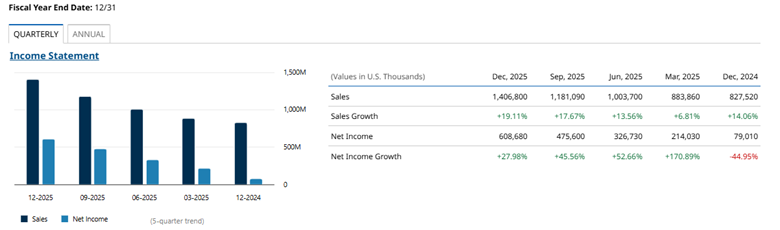

Pay attention to this spike. While in December 2024 quarterly net income was just $79 million on $827 million in revenue, the company made a huge leap in just one year. In the fourth quarter of 2025, revenue reached $1.41 billion — showing 19% sequential growth — while net income skyrocketed to $608.68 million. The margins boggle the mind.

The market fell into pure euphoria seeing these figures. The retail and institutional crowd extrapolated this success into infinity. Many likely believed that, because Palantir was the first to successfully arm its tech with AI, the firm would continue to capture the market alone. The illusion of an insurmountable gap began to form.

But right here — at the very peak of this “golden window” — the main existential threat to the company's current capitalization is likely brewing.

Technological Parity and the Big Tech Threat

The core issue with the "Palantir is an eternal leader" investment thesis lies in underestimating the nature of AI itself. Artificial intelligence is most likely the great technological equalizer.

In business, like in naval warfare, you cannot ignore the speed of the enemy even if they are currently just a speck on the horizon. Competitors already exist. Yes, they are at the beginning of their journeys. From Microsoft (MSFT) Fabric to Databricks' initiatives or ecosystem agents from Salesforce (CRM), other solutions objectively lose to Palantir right now in the depth of complex data integration. But this is likely temporary. Armed with bleeding-edge AI and deep pockets, the giants will try and play catch-up — and they will probably catch up.

Competitors will ostensibly try to automate what serves as Palantir's exclusive advantage today. I suspect that we are on the verge of seeing next-generation AI agents from Microsoft, Alphabet (GOOGL), and other heavyweights. These agents will not be designed merely as chatbots. They will be autonomous entities capable of understanding database structures, independently scanning ERP systems, cloud storage, and corporate email.

If Palantir managed to create algorithms for rapid data structuring, won't Google or Microsoft be able to do exactly the same? The very corporations possessing vastly superior resources and the best base models in the world? I assume they can — and they might pull it off quite quickly.

In the next year or two, we could hit a point of technological parity. Advanced agents within Microsoft Copilot Studio or Google Vertex AI will likely learn to execute the exact same data stitching Foundry currently does, entirely removing the need to hire an army of expensive consulting engineers. A user will simply drop a prompt, and a fourth or fifth generation AI model could execute the task on the fly.

Here lies the fatal vulnerability for Palantir's multiples.

Microsoft and Google already control the base enterprise infrastructure. Their solutions won't require integration as heavy, third-party software. They will likely be delivered as a natural update to Windows, Azure, or Workspace. Palantir's technological window of opportunity is rapidly shrinking. In my view, the company may have no more than 12 to 18 months of solitary dominance in this narrow niche. If that exclusivity vanishes, the rules of the game for Palantir will probably change forever.

An Expansion Slowdown and Price War

As soon as comparable solutions from tech giants hit the market, the rules will shift dramatically. A unique technology might morph into a standardized service. The commoditization of the product will likely occur. For a company whose valuation is built on the expectation of an eternal lack of rivals, this could mark the beginning of the end for the current investment thesis.

What happens to Palantir when the corporate client gets a choice? A choice between implementing the heavy, boutique AIP product or activating built-in agents within an already paid Microsoft or Google subscription.

First, price competition could hit Palantir hard. Right now, they can dictate terms and maintain high margins simply because clients lack a clear alternative for tasks of such complexity. But if analogs emerge, closing multi-million-dollar deals will become physically difficult. To sustain new client acquisition rates, Palantir will likely be forced to either slash prices or massively ramp up marketing and sales expenses. Both scenarios lead to potential margin compression.

Second, the aggressive outward expansion could halt. Palantir will certainly not disappear. Corporations and government agencies that have already deeply integrated Foundry into their processes will most likely stay put. The cost and headache of switching systems are just too high, so Palantir should retain its sticky client base.

But for investors, this is probably a weak consolation. Halting expansion and splitting the addressable market will mean the company transitions from a hyper-growth star into a stable, mature business. And the market never awards a mature business a P/E multiple above 200 times.

A Financial Reality Check

To definitively stress-test the illusion of eternal, zero-competition growth, we just need to translate our reasoning into the language of hard numbers. Fundamental math is hard to fool.

Currently, Palantir's market cap is an astronomical $340 billion. Meanwhile, the company's trailing net income sits just over $1.6 billion. The P/E ratio is shattering all conceivable records, hovering around 240 times.

Let's do the math.

What does the company need to do to fundamentally justify a $340 billion valuation under normal, mature tech sector conditions? If we assign a very generous forward P/E of 35 times to 40 times for an established company, Palantir would need to generate roughly $8 billion to $10 billion in annual net profit. This means quarterly net income would need to hit a stable run rate of $2 billion to $2.5 billion.

Now let's look at reality. In Q4 2025, the company posted $1.4 billion in total revenue. So, to justify today's share price, Palantir's quarterly net profit must become nearly twice as large as its entire revenue right now. This demands colossal, exponential scaling.

Here, we return to the time factor. If we assume the technological window of leadership closes in late 2027 with the release of new corporate AI solutions from Big Tech, Palantir has slightly over a year left. Can the company balloon its quarterly net profit from $608.7 million to $2.5 billion in just five or six quarters, factoring in the growing base effect? Most likely not.

Even maintaining its current breakneck growth rates, calculations suggest the company simply won't reach those numbers before competitors clip the wings of its unhindered expansion. The race against time appears mathematically lost. Competitors might catch up faster or slower than my hypothetical timeline. But the main takeaway is that rival technologies will eventually, probably, catch Palantir.

Palantir Likely Faces Multiple Compression

The market is making a classic mistake. It is buying a magnificent technology while completely ignoring the price tag and turning a blind eye to industry dynamics. Palantir is genuinely a strong company with an excellent product, which will continue to print money and hold its market share. I don't foresee a business catastrophe. But a valuation catastrophe is highly likely.

Current valuations are a projection of a future where Palantir alone holds the keys to corporate artificial intelligence. But there is only one end market for everyone. Tech giants are already aggressively prepping their tools to seize this territory. The ability of AI agents to autonomously stitch disparate data together will likely strip Palantir of its primary unique advantage.

As soon as investors realize technological parity has been reached, a painful but entirely logical multiple compression could occur. The company's valuation risks deflating from an illusory 240-plus P/E down to grounded figures reflecting a real competitive environment. Shares overheated by the lack of dense present competition will hardly withstand the crushing pressure of future rivalry.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)