The excitement around the next iPhone cycle is already building, and this time it’s not just about faster cameras or sleeker designs. Apple (AAPL) is expected to step into the foldable arena as early as September, alongside a redesigned glass-heavy iPhone Pro. If that plays out, it could open a fresh upgrade cycle and, more importantly, ignite demand deep inside the supply chain, where chipmakers stand to gain the most.

That’s exactly where Barclays sees an opportunity. Heading into earnings season, the brokerage firm reshuffled its semiconductor coverage, arguing that most of the sector’s growth story is understood and already priced in through 2027. In such a crowded trade, investors are hunting value.

Against this backdrop, analyst Tom O’Malley zeroed in on hard semiconductor component makers and radio frequency chipmakers as overlooked pockets of upside. Names like Skyworks Solutions (SWKS) and Qorvo (QRVO) fit that bill, and both were upgraded to “Overweight” by Barclays. While recent timing shifts in Apple’s lower-end launches have created short-term pressure, Barclays sees the current weakness as a “Buy the Cut” moment.

With foldables and a major iPhone anniversary cycle ahead, these two chip stocks could be wise buys right now.

Chip Stock #1: Skyworks Solutions

Skyworks Solutions, with a market cap of $9.3 billion, is a key player in the global wireless connectivity space. Based in Irvine, California, the company designs and manufactures analog and mixed-signal semiconductors that power communication across smartphones, automotive systems, and a growing range of connected devices.

Its chips sit at the center of modern connectivity – linking everything from smart homes and wearables to industrial systems and defense applications. As demand for faster, more reliable wireless networks grows, Skyworks continues to position itself as an essential supplier behind the scenes of this increasingly connected world.

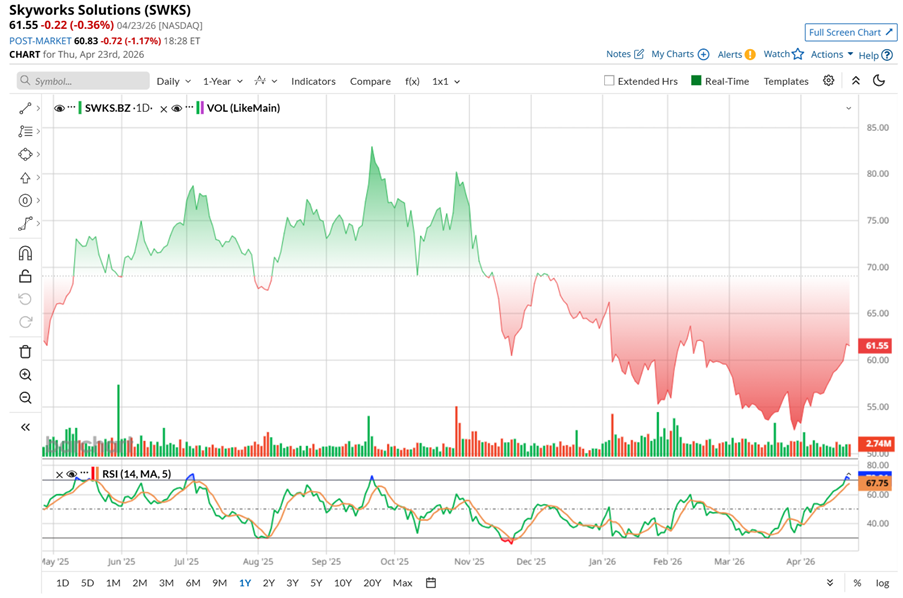

Shares of the wireless chipmaker have had a volatile stretch over the past year, swinging between sharp highs and lows. SWKS stock peaked around $90.90 in October before sliding to a low of $51.93 in March, leaving the stock down 43% from its high. Still, over the past 52 weeks, the stock has held onto a modest gain of 2.58%.

The past six months have been weak, with SWKS down nearly 14.8%, but recent action suggests a shift. The stock has climbed 13.95% over the past month, including a 6.94% gain in just the last five days.

Technically, the 14-day RSI had pushed into overbought territory of 74.95 but now appears to be easing, hinting at a possible pause after the recent run.

Valuation-wise, SWKS is hard to ignore. The stock trades at roughly 13.15 times forward earnings and about 2.46 times sales, both sitting below sector averages and its own historical medians. It is priced cheaper than usual.

What adds to the appeal is its steady approach to rewarding shareholders. The company has raised its dividend for 11 consecutive years and now pays about $2.84 per share annually, offering an annualized yield of 4.6%. With a payout ratio around 48%, there’s still room to keep those increases going.

Skyworks Solutions stepped into its latest earnings season with a steady backdrop, but walked out with a solid surprise. The company reported its fiscal Q1 2026 results on Feb. 3, and the headline numbers did not look flashy at first glance. Revenue dipped 3.1% year-over-year (YOY) to $1 billion, and adjusted EPS declined 3.8% annually to $1.54. But both still came in ahead of Wall Street's predictions, and that was enough to spark a 5.5% jump in the stock the next day.

The Mobile segment held steady, doing the heavy lifting with consistent execution, while the Broad Markets business quietly gained traction. That segment, which spans areas like automotive, IoT, and cloud infrastructure, grew both sequentially and YOY, helped by rising demand for Wi-Fi 7 and data center programs.

Meanwhile, the company’s financial position strengthened. Cash & cash equivalents and marketable securities amounted to $1.57 billion as of Jan. 2, 2026, while long-term debt edged up to $996.2 million. Operating cash flow nearly doubled to $395.5 million, driving free cash flow to $339 million, with a strong 32.7% margin.

The company is all set to discuss its second-quarter fiscal 2026 results and business outlook on Tuesday, May 5, after the market closes. The management is setting a fairly measured tone for the next quarter. While revenue is anticipated to be between $875 million and $925 million, non-GAAP EPS is expected to be around $1.04.

The Mobile segment is expected to see about a 20% sequential drop, highlighting the usual ups and downs tied to smartphone cycles. On the other hand, the Broad Markets business is holding steady, with revenue projected to remain roughly flat quarter-over-quarter. Even so, that segment continues to gain importance. It is expected to make up about 44% of total revenue and grow at a high single-digit pace compared to last year.

Meanwhile, Wall Street analysts project EPS for the quarter to be $0.67, down 21.2% YOY, while revenue is projected to be around $901.8 million. Looking further ahead to fiscal 2026, profit is estimated at $3.25 per share, marking a roughly 29.2% annual dip, but then rise by 7.4% YOY to $3.49 in fiscal 2027.

SWKS just got a lift from analyst Tom O'Malley, who upgraded the stock to “Overweight” and bumped the price target to $70 from $60. The setup looks shaky at first glance. Apple’s delay in launching lower-end iPhones is pushing volumes into 2027, which means a weaker-than-usual festive cycle – traditionally Skyworks’ sweet spot.

Since Skyworks is heavily tied to these lower-end models, the near-term hit is real. Adding concerns around flat content growth and potential share loss, the story gets even tougher. But here’s the twist. Barclays sees this as a timing issue, not a structural one. With Apple’s bigger product cycles, including foldables and anniversary devices, still ahead, O’Malley believes the positives could eventually outweigh the noise.

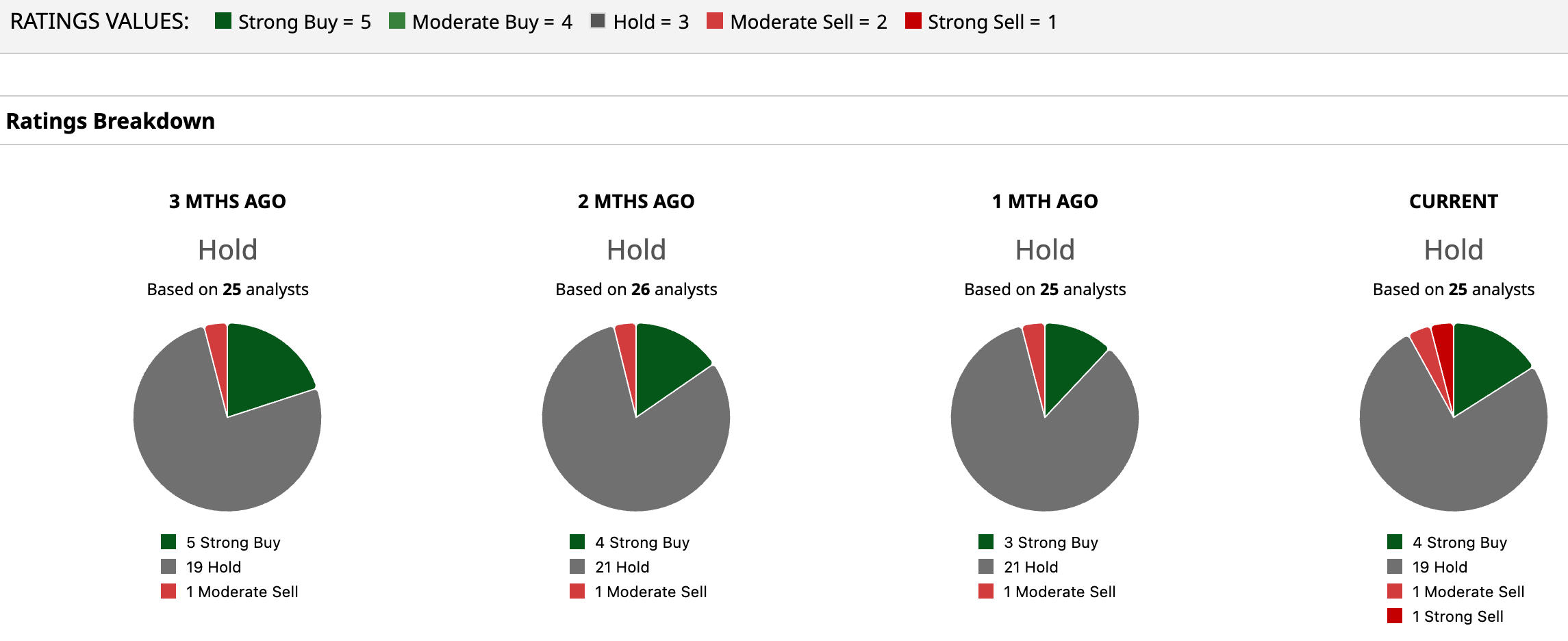

Analysts’ consensus opinion on the stock is neutral, with a “Hold” rating overall. Among the 25 analysts covering the stock, four are recommending a “Strong Buy,” 19 advise a “Hold,” one suggests a “Moderate Sell”, and the remaining one analyst is outright skeptical with a “Strong Sell” rating.

SWKS’ average analyst price target is $68.33, indicating an upside potential of 8.12% from the current levels. The Street-high target of $106 implies the stock could rise as much as 67.7%.

Chip Stock #2: Qorvo

Qorvo, founded in 1957 and based in Greensboro, North Carolina, is a global chipmaker powering the connected world. The company designs semiconductor solutions used across smartphones, automotive, defense, and industrial markets. It operates through three segments of High-Performance Analog (HPA), Connectivity and Sensors Group (CSG), and Advanced Cellular Group (ACG), serving everything from 5G networks to smart homes.

Qorvo combines deep engineering expertise with large-scale manufacturing to tackle complex tech challenges. With a presence across the U.S., China, Asia, and Europe, it supplies leading device makers and continues to expand into high-growth areas like ultra-wideband, Wi-Fi, and automotive connectivity. The market cap currently sits at $7.847 billion.

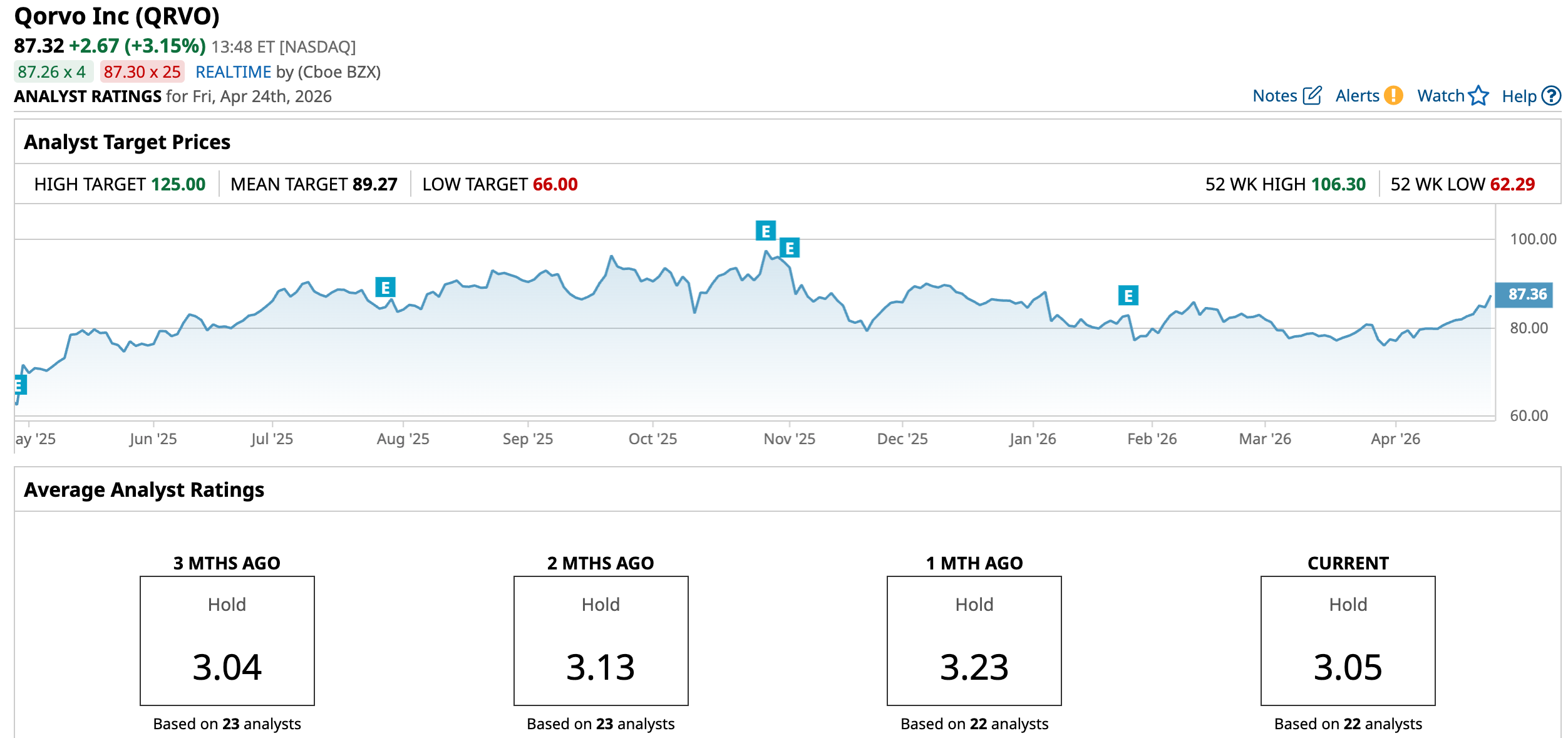

Shares of the communications chipmaker have been on a bit of a rollercoaster, but the tone is shifting. QRVO stock is still up 37.4% over the past 52 weeks, even after pulling back nearly 20.4% from its October peak of $106.30. More importantly, it has rebounded 44% from its 52-week low of $60.92, showing buyers are stepping back in.

Lately, momentum is building again, with gains of 9.57% over the past month and a steady push higher in recent sessions.

Technically, the 14-day RSI sits at 74.81, positioning the stock in overbought territory but still has some room to run.

Valuation-wise, Qorvo is trading at a noticeable discount. The stock is priced at 12.95 times forward adjusted earnings and 2.13 times forward sales, sitting below sector averages and its own historical levels. The market might not fully pricing in its growth potential, keeping it in a relative bargain zone. This could be something that could appeal to value-focused investors.

Qorvo unveiled its Q3 earnings report on Jan. 27, with both top and bottom lines exceeding Wall Street’s projections. Revenue climbed to $993 million, up 8.4% YOY, helped by a key design win in cellular-enabled iPads and strong demand from flagship smartphones.

But it was not just phones doing the heavy lifting. Early traction in automotive ultra-wideband, along with steady demand from defense, aerospace, and infrastructure markets, added more fuel to the mix. Adjusted earnings jumped 34.8% annually to $2.17 per share.

During the quarter, the gains came from smarter execution – more content per device, a richer mix of high-end products, and efficiency improvements from restructuring. Margins got a boost, and it showed.

The breakdown shows where the strength really came from. Qorvo generated $190.9 million in revenues from its HPA segment, while the CSG segment added $111.3 million. The bulk of the revenue, though, came from the ACG at $690.8 million, fueled by solid demand in premium smartphones.

Looking at the balance sheet, the company showcases strength. As of Dec. 27, 2025, cash and cash equivalents came in at $1.3 billion, while long-term debt amounted to $1.55 billion. Qorvo generated $265.4 million in net cash from operating activities and $236.9 million in FCF.

The company is gearing up to release its fiscal 2026 fourth quarter financial results on Tuesday, May 5, after the market closes. Management guided for Q4 revenue of approximately $800 million, plus or minus $25 million, with non-GAAP EPS expected to be around $1.20, plus or minus 15 cents.

Meanwhile, Wall Street sees revenue landing near $801.8 million, with profit at $0.97 per share, down 17.8% YOY. But looking at the full year, things appear different. Fiscal 2026 EPS is expected to be $5.29, up 13.8% YOY, and then rise by another 9.6% annually to $5.80.

Along with upgrading QRVO from an “Equalweight” rating to an “Overweight,” analyst O’Malley raised QRVO’s price target to $100 recently.

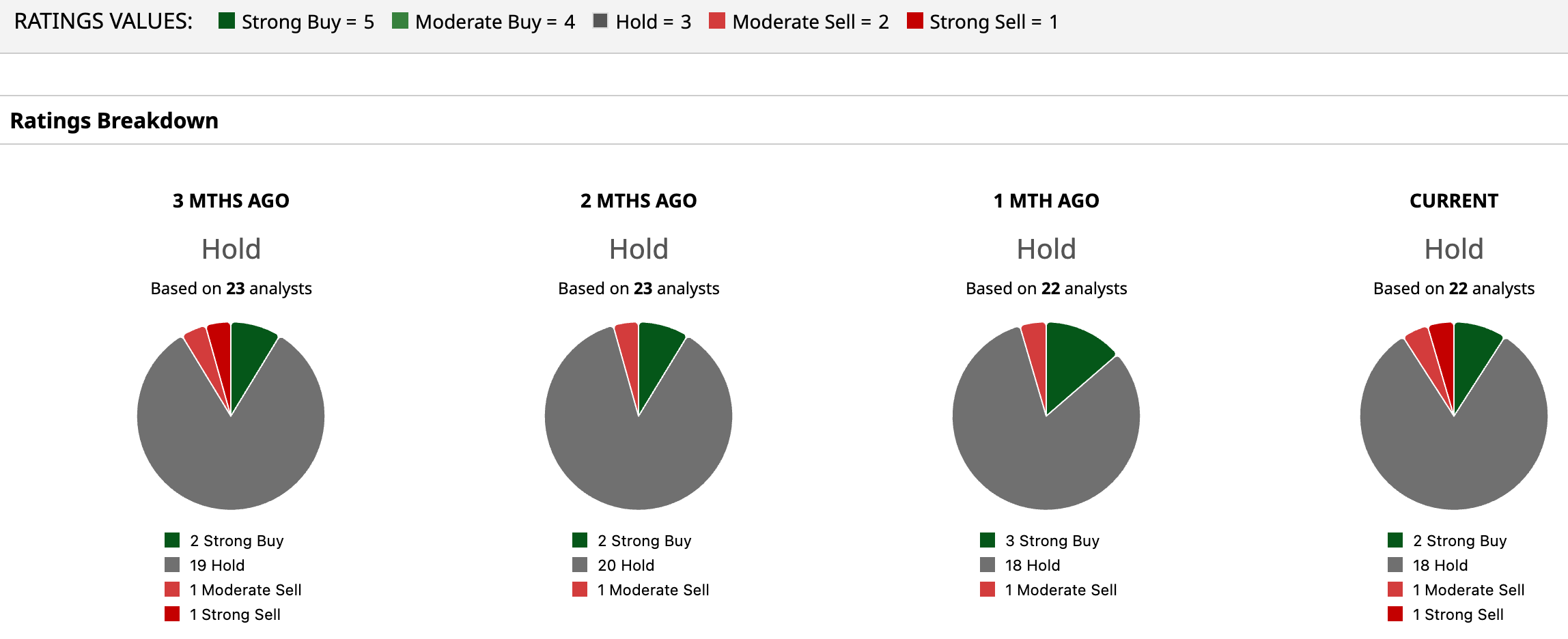

Analysts are playing it safe, with QRVO stock having an overall “Hold” rating. Of the 22 analysts tracking the stock, just two back it with a “Strong Buy,” 18 have a “Hold,” one has a “Moderate Sell,” and the remaining one suggests a “Strong Sell" rating.

QRVO’s average target of $89.27 suggests an upside potential of 2.23% from the current price levels. The Street’s highest $125 price target hints the stock could rally as much as 43.2%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)