/Unitedhealth%20Group%20Inc%20HQ%20photo-by%20jetcityimage%20via%20iStock.jpg)

The U.S. managed care sector has had a rough year. Medical costs jumped, reimbursement outlooks were cut, and the country’s largest private insurer, UnitedHealth Group (UNH), found itself at the center of a serious credibility problem. By late January 2026, UNH had dropped about 46% over the prior year, erased roughly $60 billion in market value in a single day, and pulled its full‑year guidance after a weak Q4 and restructuring charges.

The stock then spent months trying to find a bottom. By late March, UNH was still down 18% year-to-date, trading well below key moving averages, while analysts cut Q1 estimates as high medical costs kept weighing on sentiment.

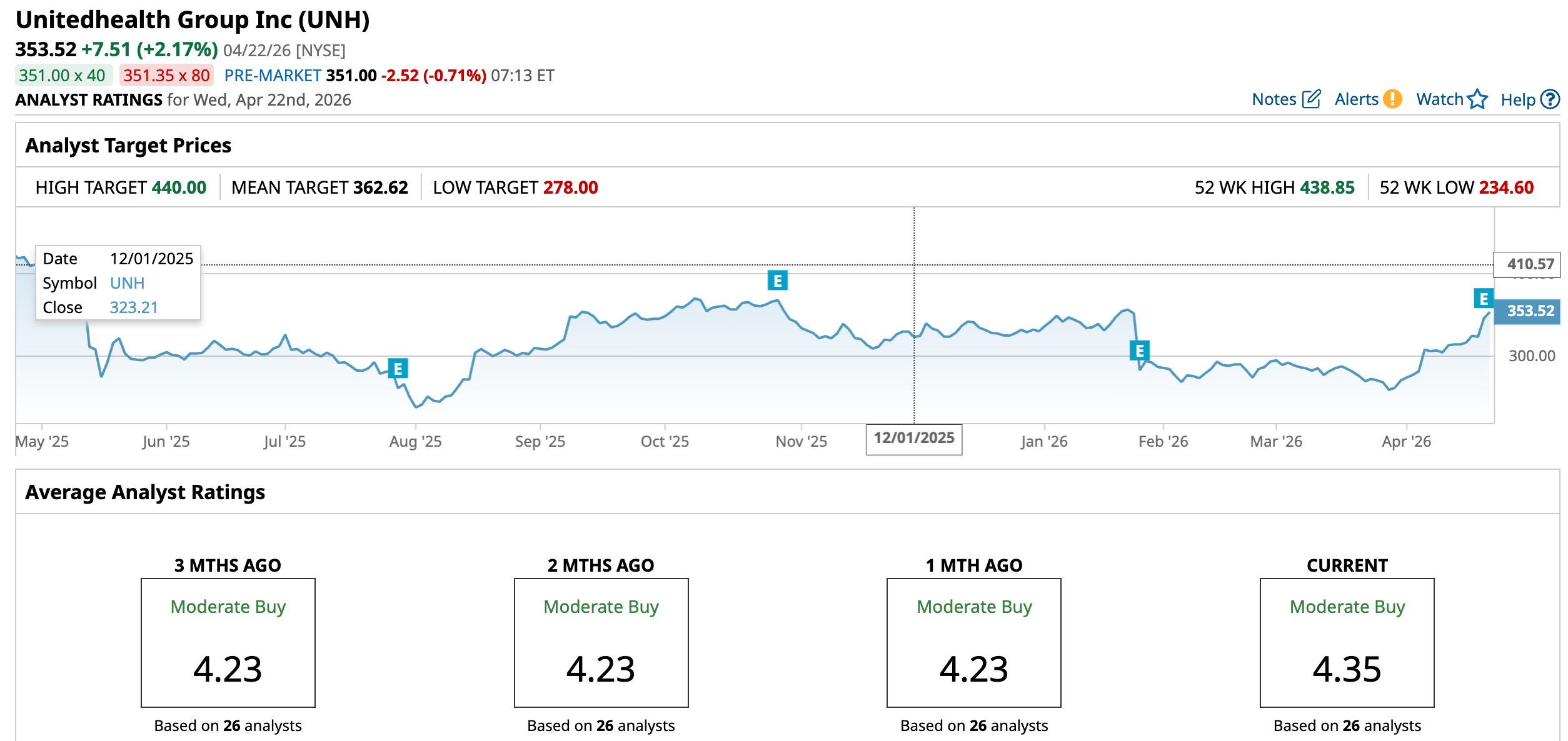

Then came April 21. UnitedHealth posted Q1 2026 adjusted EPS of $7.23, easily topping the $6.48 consensus, on $111.7 billion in revenue. It also raised its full‑year 2026 adjusted profit outlook to at least $18.25 per share, up from $17.75. The stock reacted right away, jumping from $323.48, pushing its RSI into the 80s and into technically overbought territory. It was UNH’s strongest earnings reaction in several quarters, off a low of $234.60, a gain of nearly 38% from the bottom into the print.

The numbers are hard to ignore. After a year of misses, pulled guidance, and a hit to trust so severe that management called it “broken,” is this the start of a real, lasting turnaround, and is this finally the move long‑time investors have been waiting for? Let’s find out.

UnitedHealth By the Numbers

UnitedHealth Group (UNH) today is basically a full‑service healthcare setup, pairing its UnitedHealthcare insurance business with the Optum platform, which handles services like care delivery, pharmacy, and data at scale.

Over the past 52 weeks, the stock has been down 17.24%, but year-to-date (YTD) it has managed to bounce 7.09%.

On valuation, UNH trades at a forward P/E of 18.32 times versus 17.71 times for the sector, so the market is paying a small premium for a company that looks like it’s slowly getting back on track. Income investors still have a solid case here.

UnitedHealth pays an annual dividend of $8.84, a 2.73% yield compared with the healthcare sector’s 1.58%, with the latest $2.210 dividend paid on March 9, 2026. The forward payout ratio is 53.17%, the dividend comes quarterly, and UNH has raised it for 16 straight years.

The latest quarter helps justify that confidence. First‑quarter 2026 revenue came in at $111.7 billion, up from $109.6 billion a year earlier. Adjusted net earnings were $7.23 per share, and earnings from operations reached $9.0 billion.

UnitedHealthcare now serves 49.1 million consumers and lifted its operating margin by 40 basis points to 6.6%, which matters in a thin‑margin line of business. Optum serves more than 122 million consumers, brought in $63.7 billion in revenue and $3.3 billion in earnings, for a 5.2% margin, showing that the services side is pulling its weight in the turnaround story.

What’s Powering UnitedHealth’s Momentum

UnitedHealthcare is leaning hard into new tech with Avery, a digital assistant built to make it easier for members to find their way around their plans and benefits. Avery lives inside the UnitedHealthcare app and myuhc.com and helps with everyday tasks like coverage questions, booking appointments, checking cost estimates and plan balances, tracking rewards and wellness programs, managing ID cards and OTC benefits, finding providers, checking claim status, and reading explanations of benefits. It already serves about 6.5 million employer-sponsored members and 160,000 Medicare Advantage members, with plans to reach 20.5 million commercial, Medicare and Medicaid members by year-end, and it runs under strict rules around safety, fairness, privacy and human oversight.

UnitedHealthcare is also trying to make life easier for providers, especially in rural areas. It is dropping most medical prior authorizations for rural providers and speeding up payments by up to 50% for roughly 1,500 rural hospitals and all Critical Access Hospitals, while building hub-and-spoke partnerships to bring key services closer to patients in underserved communities.

Analyst Revisions and Forward Signals

For the current quarter (Q1 2026), Wall Street is looking for earnings of $4.63 per share, down from $4.08 a year ago, which works out to about 13.5% lower year-over-year (YOY). For next quarter (Q2 2026), expectations improve, with the Street modeling $3.82 in EPS versus $2.92 last year.

For the full year 2026, the average earnings estimate sits at $18.32, up from $16.35 in 2025, an 12% growth rate. That climbs again in 2027, where analysts see $20.12 in EPS versus $18.32, implying roughly 9.8% growth.

On the ratings side, Raymond James recently upgraded UnitedHealth from “Market Perform” to “Outperform” with a $330 price target, with analyst John Ransom arguing that smart use of technology can cut general and administrative costs and make margins at Optum Health easier to predict. J.P. Morgan’s Lisa Gill is still positive too. She kept an “Overweight” rating but trimmed her target from $425 to $389, signaling that she still likes the long-term story even if near-term utilization and regulatory headlines are noisy.

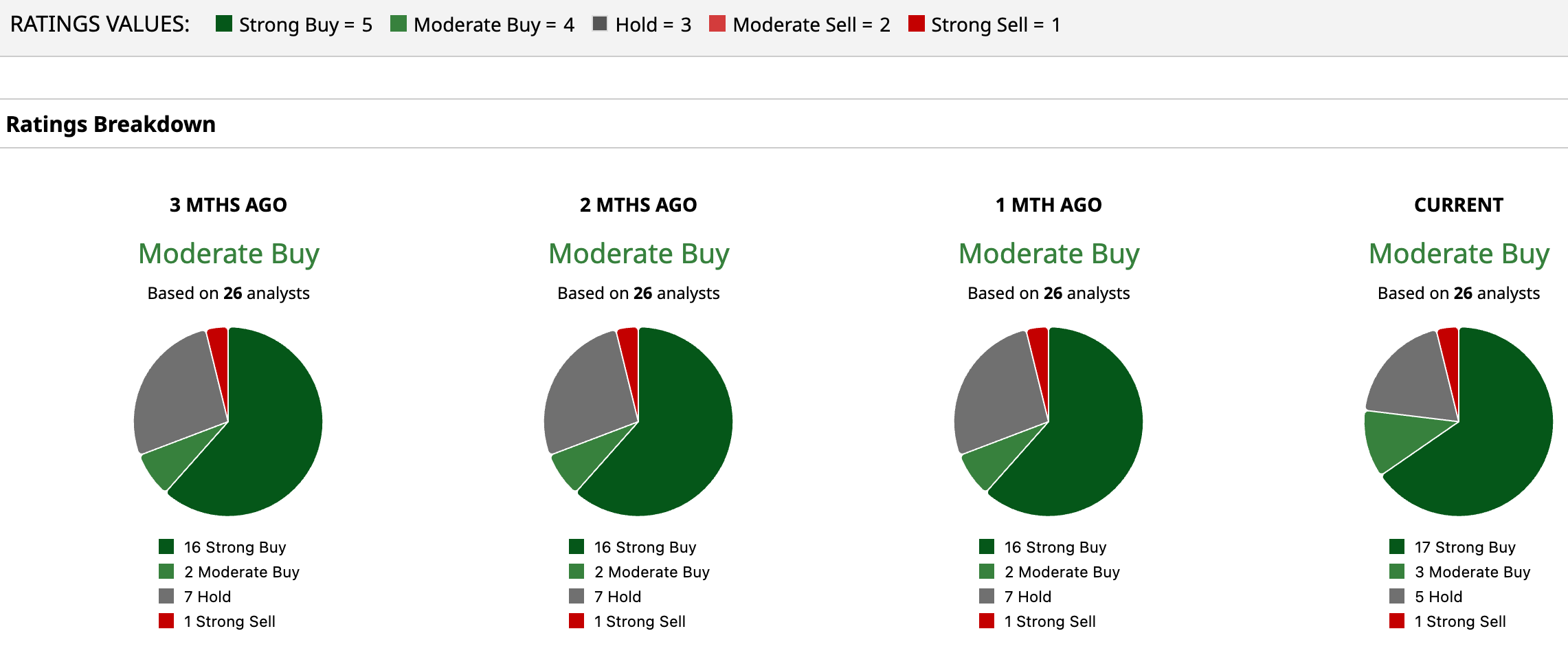

Overall, the stock holds a “Moderate Buy” status. Of 26 analysts, 17 rate it a “Strong Buy,” three give a “Moderate Buy," five are on the sidelines with a “Hold,” and the remaining analyst goes with a “Strong Sell.” Their average price target of $362.62 points to 2.6% upside from recent price levels, but the Street-high price of $440 calls for 24.5% upside potential this year.

Conclusion

At this point, it looks like UnitedHealth’s long‑awaited turnaround is finally taking shape, even if it is not a clean, straight line. The stock has come off a brutal drawdown, but a decisive beat on Q1 earnings, a higher full‑year profit guide, and early traction in AI‑driven efficiency and member engagement all point to a business that is repairing both margins and credibility. Layer on top a resilient dividend profile and a still‑supportive analyst backdrop, and the odds favor the shares grinding higher over the next 12 to 18 months rather than rolling over again, with volatility more likely to come from macro and policy shocks than from company‑specific cracks.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)