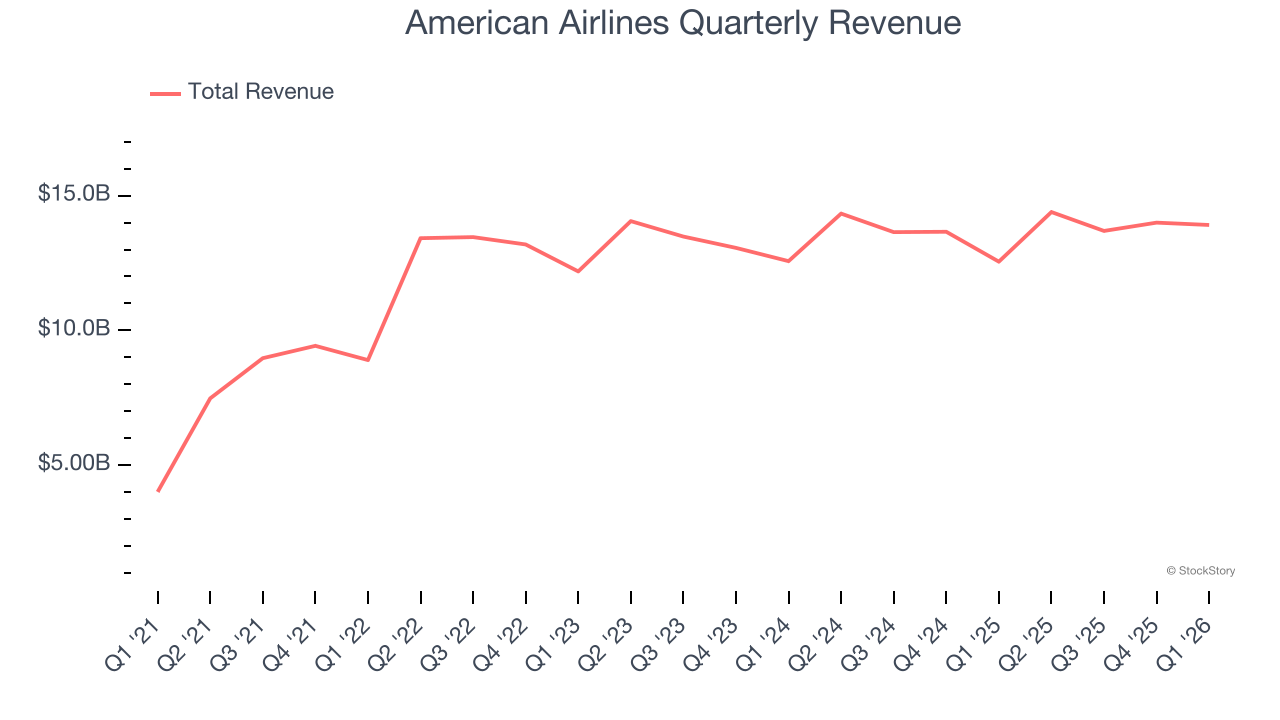

Global airline American Airlines (NASDAQ:AAL) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 10.8% year on year to $13.91 billion. On the other hand, next quarter’s revenue guidance of $15.11 billion was less impressive, coming in 8.1% below analysts’ estimates. Its non-GAAP loss of $0.40 per share was 13% above analysts’ consensus estimates.

Is now the time to buy American Airlines? Find out by accessing our full research report, it’s free.

American Airlines (AAL) Q1 CY2026 Highlights:

- Revenue: $13.91 billion vs analyst estimates of $13.82 billion (10.8% year-on-year growth, 0.6% beat)

- Adjusted EPS: -$0.40 vs analyst estimates of -$0.46 (13% beat)

- Adjusted EBITDA: $434 million vs analyst estimates of $768.2 million (3.1% margin, 43.5% miss)

- Revenue Guidance for Q2 CY2026 is $15.11 billion at the midpoint, below analyst estimates of $16.44 billion

- Management lowered its full-year Adjusted EPS guidance to $0.35 at the midpoint, a 84.1% decrease

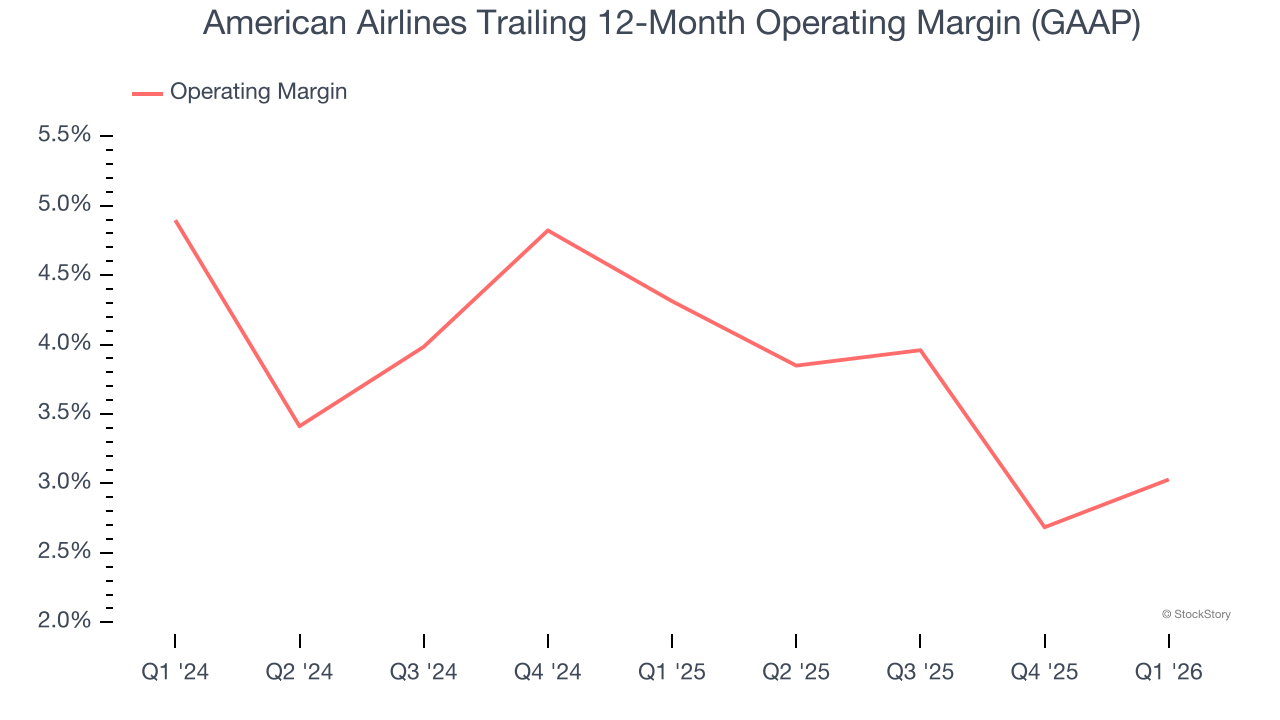

- Operating Margin: -0.3%, up from -2.2% in the same quarter last year

- Free Cash Flow Margin: 24.5%, up from 13% in the same quarter last year

- Revenue Passenger Miles: up 2.2 billion year on year

- Market Capitalization: $7.59 billion

“American delivered record revenue in the first quarter, and we’re on track for another record in the second quarter,” said American’s CEO Robert Isom.

Company Overview

One of the ‘Big Four’ airlines in the US, American Airlines (NASDAQ:AAL) is a major global air carrier that serves both business and leisure travelers through its domestic and international flights.

Revenue Growth

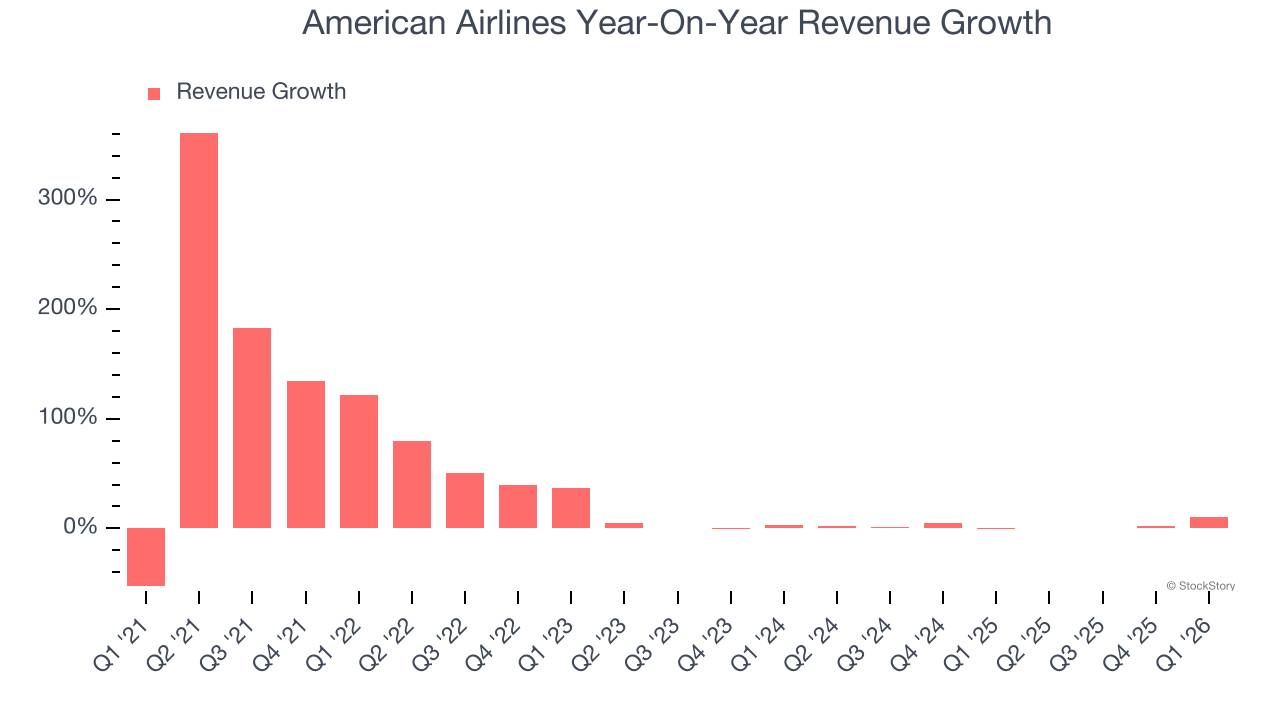

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, American Airlines grew its sales at a 34.3% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. American Airlines’s recent performance shows its demand has slowed as its annualized revenue growth of 2.6% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

American Airlines also discloses its number of revenue passenger miles, which reached 58.55 billion in the latest quarter. Over the last two years, American Airlines’s revenue passenger miles averaged 10.6% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, American Airlines reported year-on-year revenue growth of 10.8%, and its $13.91 billion of revenue exceeded Wall Street’s estimates by 0.6%. Company management is currently guiding for a 5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 11.1% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

American Airlines’s operating margin has shrunk over the last 12 months and averaged 3.7% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, American Airlines’s breakeven margin was -0.3%, up 1.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

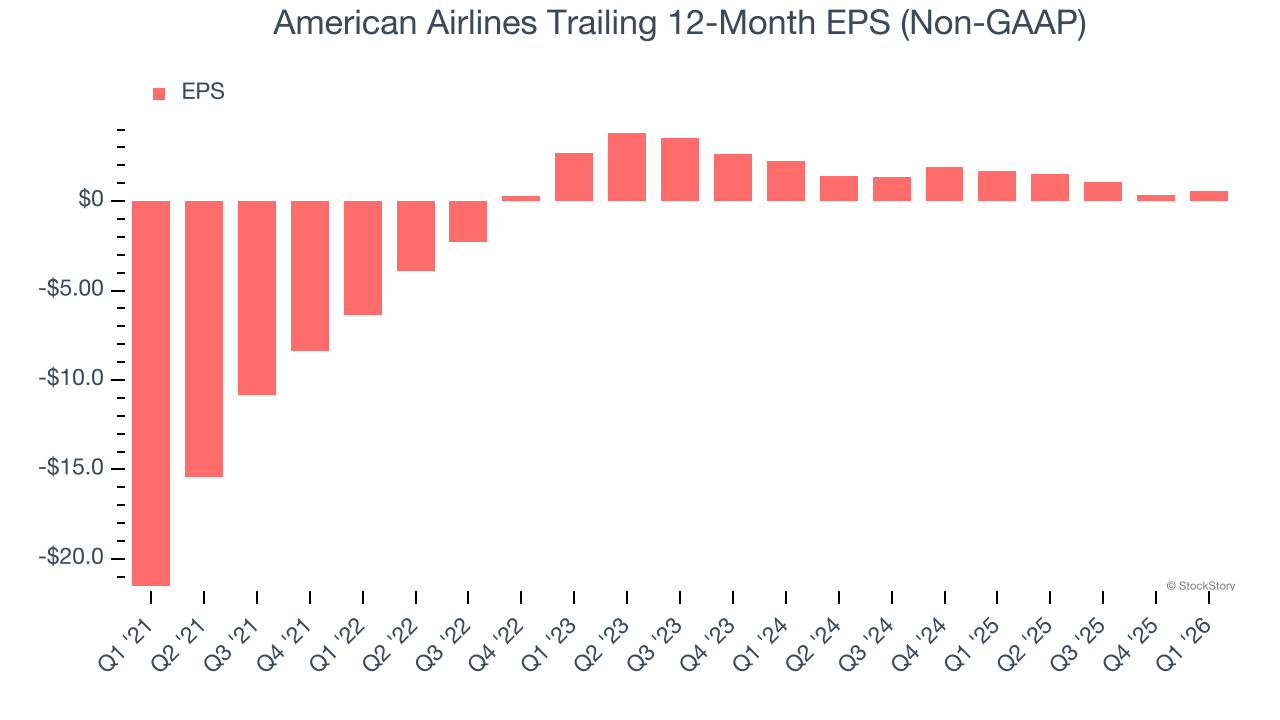

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

American Airlines’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q1, American Airlines reported adjusted EPS of negative $0.40, up from negative $0.59 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects American Airlines to perform poorly. Analysts forecast its full-year EPS of $0.54 will invert to negative negative $0.39.

Key Takeaways from American Airlines’s Q1 Results

We were impressed by American Airlines’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. On the other hand, its EBITDA missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock remained flat at $11.46 immediately following the results.

Is American Airlines an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)