Oil markets are tense again as trouble around the Strait of Hormuz raises fresh questions about oil flows and jet fuel costs. Earlier fuel spikes already pushed airline names lower and left prices looking more attractive across the group. That kind of pressure has pulled more focus back to airlines and made any move from inside the executive suite feel a lot more important.

Delta Air Lines (DAL) is now front and center after Chief of Operations John Laughter recently cut more than 21% of his personal stake. This move came after the stock climbed back above its 200-day moving average. The executive's sale has sparked a fresh debate about whether this latest rally in DAL stock still has room to run.

Is this the moment to follow Laughter's lead and walk away from DAL? Or does it still make sense to stay on board for the next leg higher? Let’s take a closer look.

Can Delta’s Numbers Justify the Insider Exit?

Headquartered in Atlanta, Georgia, Delta Ait Lines operates a global route network that serves corporate, leisure, and premium travelers across domestic and international markets.

Shares of Delta sit near $68 as of this writing. The stock is now down more than 1.5% year-to-date (YTD) but remains up by 69% over the past 12 months.

Delta is valued at about $46.1 billion by market capitalization and trades at 11.8 times trailing earnings and 7.45 times price‑to‑cash‑flow, which is a bit cheaper than the respective sector medians. That market value supports a forward annual dividend of $0.75 per share, working out to a modest 1.05% yield.

The company's most recent earnings report, released earlier this month for the March quarter of 2026, showed EPS of $0.64 versus a consensus estimate of $0.61, a nearly 5% positive surprise. This beat suggests that Delta is still running a little ahead of what the market expected.

The same period brought in sales of $15.85 billion, with sales declining roughly 1% compared to the previous quarter but growing 13% year-over-year (YOY) from $14.04 billion in Q1 2025. That tells investors that demand is holding, but not really picking up speed. The company still reported a net loss of $289 million, with net income falling 124% sequentially, so profits clearly took a step back.

That pressure shows up in the cash flow numbers, too. Operating cash flow for the March 2026 period came in at $2.43 billion, down 71% from the previous period. Net cash flow was $734 million as well, down 32% sequentially, which leaves Delta with less financial flexibility.

Strategic Shifts Behind the Insider Exit

Leadership is the easiest place to link John Laughter’s stock sale to what is happening at Delta. The executive is wrapping up a 30‑year career and stepping down from his roles as Executive Vice President, Chief of Operations, and President of Delta TechOps at the end of April. In his place, Peter Carter is becoming President and Dan Janki is taking over as Chief of Operations. Meanwhile, Erik Snell is moving into the role of Chief Financial Officer and Ranjan Goswami is becoming Chief Marketing and Product Officer.

At the same time, Delta is making long‑term calls on its fleet and costs. The airline has chosen GE Aerospace's (GE) GEnx engines for 30 new Boeing (BA) 787‑10 jets, with options for 30 more, plus spare engines and long‑term service support. This locks in the engine choice for a big widebody expansion and supports the company's long‑haul international plans, using an engine family already widely used on 787s and known for better fuel use and reliability.

On the revenue side, Delta is also trying to bring in more money per customer by raising checked bag fees. The management has tied that move directly to higher jet fuel costs linked to tensions overseas. The change shifts more of that fuel bill onto travelers and gives the airline a tool it can use again when costs climb.

Analysts See More Upside Ahead

Analysts see a bit of a push and pull in Delta’s near-term. The next earnings report is due on July 9, covering the quarter ending June 2026, and the average earnings estimate is $1.47 per share. That is down from $2.10 in the same quarter last year, so the Street is looking for a roughly 30% drop in profit even after DAL stock’s strong run.

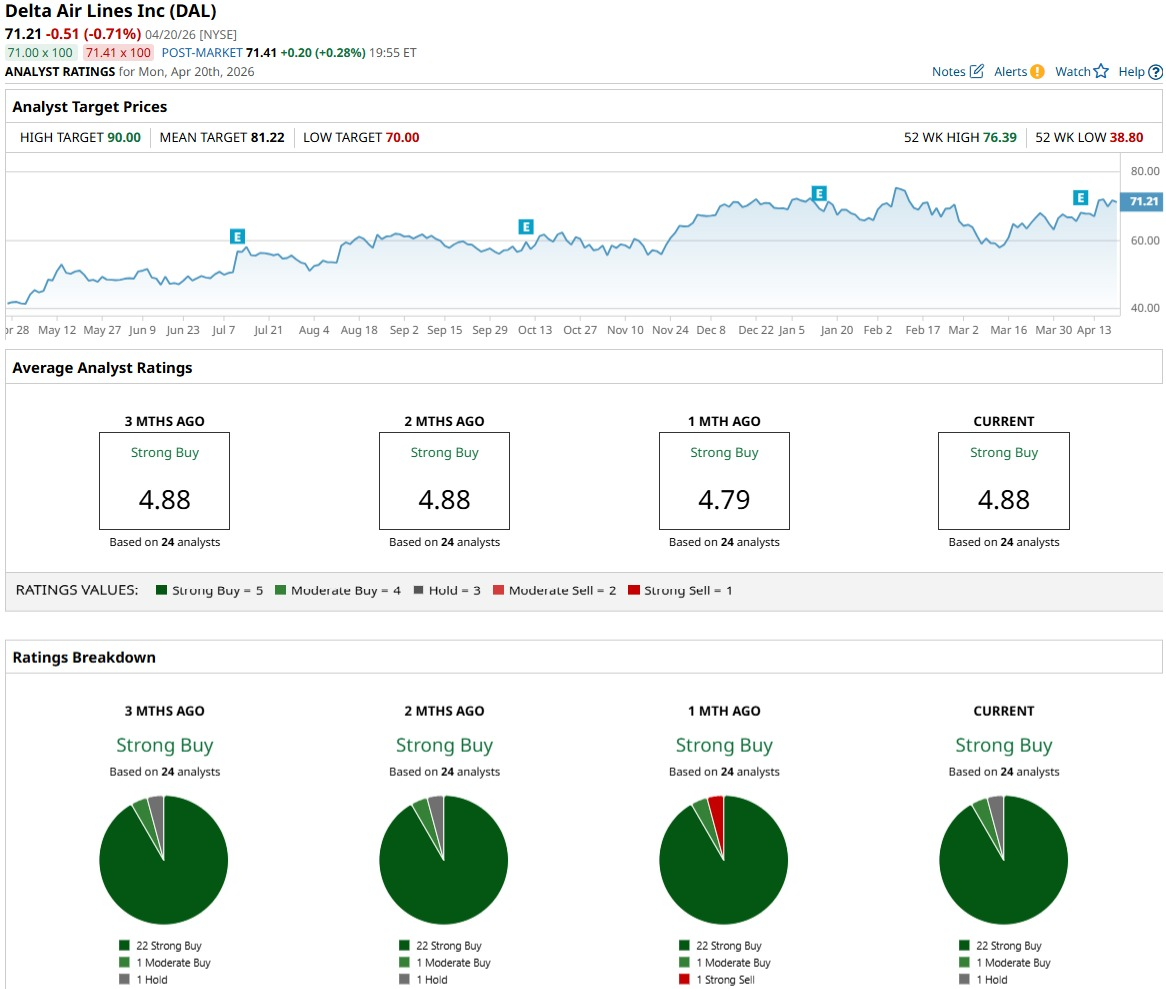

Big firms are still willing to back the name, however. Morgan Stanley recently put Delta at the top of its airline list and attached a $90 price target, signaling that analysts still see room for the story to play out on the upside.

The broader analyst community is lining up behind that stance as well, as the consensus rating on Delta is still a “Strong Buy” based on 24 analyst views. The average 12‑month price target sits at $81.43, which implies roughly 19% potential upside from current levels.

Conclusion

Delta does not really look like a stock that has to be dumped just because a long‑time insider chose to cash out part of his stake. The sale lines up with a leadership change, softer near‑term earnings, and a big run in the share price of DAL stock, but Delta is still investing and still growing. The broader view on Delta also remains positive. From here, trading will likely be ranging rather than a straight fall, with a slight lean toward drifting higher as long as Delta keeps executing reasonably well.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)