Valued at a market cap of $68 billion, Warner Bros. Discovery, Inc. (WBD) is a global media conglomerate formed by merging WarnerMedia and Discovery, Inc.. The New York-based company operates a broad portfolio spanning film studios, television networks, and streaming platforms, making it a major player in both traditional media and the rapidly evolving direct-to-consumer streaming space.

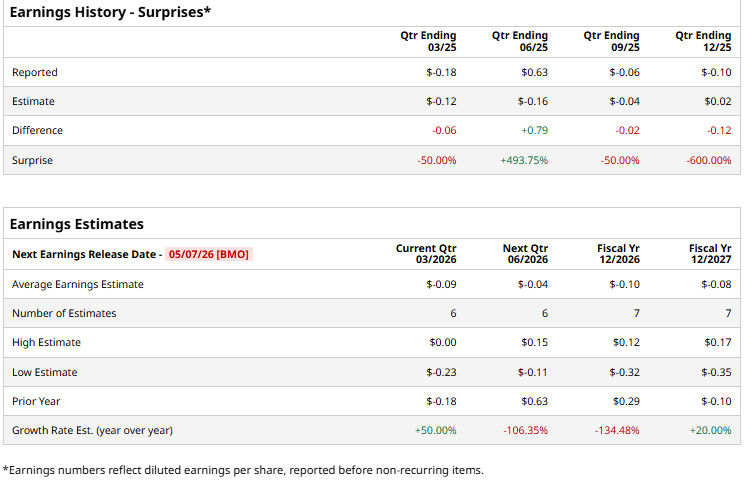

The company is scheduled to announce its fiscal Q1 earnings for 2026 before the market opens on Thursday, May 7. Ahead of this event, analysts expect this media and entertainment company to report a loss of $0.09 per share, down 50% from a loss of $0.18 per share in the year-ago quarter. The company has missed Wall Street’s bottom-line estimates in three of the last four quarters, while surpassing on another occasion.

For the current fiscal year, ending in December, analysts expect WBD to report a loss of $0.10 per share, down 134.5% from a profit of $0.29 per share in fiscal 2025.

WBD has skyrocketed 244% over the past 52 weeks, significantly outperforming both the S&P 500 Index's ($SPX) 33.6% return and the State Street Communication Services Select Sector SPDR ETF’s (XLC) 32.9% uptick over the same time period.

Warner Bros. Discovery has outperformed the broader market over the past year largely due to improving investor sentiment around its turnaround strategy. The company’s efforts to streamline operations, reduce debt, and move its streaming business toward profitability have strengthened confidence in its long-term outlook, even as near-term fundamentals remain mixed.

Additionally, corporate activity and strategic interest in the company have highlighted the underlying value of its extensive content library and global media assets, attracting investor attention.

Wall Street analysts are cautious about WBD’s stock, with a "Hold" rating overall. Among 23 analysts covering the stock, two recommend "Strong Buy," one advises "Moderate Buy,” 18 indicate "Hold,” and two give it a “Strong Sell.” While the company is trading above its mean price target of $24.78, its Street-high price target of $29.10 suggests a 6.6% potential upside from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)