/Oracle%20Corp_%20logo%20on%20phone-by%20WonderPix%20via%20Shutterstock.jpg)

Oracle (ORCL) and Amazon (AMZN) have come together to accelerate progress on one of their projects, namely building a private and high-speed connection between AWS Interconnect-multicloud and Oracle Cloud Infrastructure (OCI). The move is part of Oracle’s ambitions to deeply embed itself into the ecosystem of hyperscalers, making it a win-win scenario for all parties involved.

Oracle benefits from this as it doesn’t try to compete with the likes of AWS, Alphabet’s (GOOGL) Google Cloud, and Microsoft’s (MSFT) Azure. Instead, it is positioning itself as a layer in the same ecosystem, so that it doesn’t have to force customers away from the strong hyperscalers. This also increases the company’s addressable market.

Hyperscalers like AWS also benefit by not having to fight for customer retention or risk losing customers to Oracle. But the biggest beneficiaries are the enterprise customers, who can run their AI and data workloads seamlessly, avoiding the complexity that would be present if Oracle and cloud providers like Amazon started to compete. These customers also save on costs, as AI training and inference can span across multiple clouds.

About Oracle Stock

Oracle is best known for its enterprise software products, database systems, and cloud infrastructure services. The company’s Oracle Cloud Infrastructure is an integral part of Project Stargate, the U.S. government’s vision to dominate the global AI arena. Oracle is headquartered in Austin, Texas, and has a market capitalization of $503 billion.

ORCL stock is down 9% YTD, which is quite a performance considering how the software sector has taken a beating in the first quarter. For context, the iShares Expanded Tech-Software Sector ETF (IGV) is still down 18% year-to-date (YTD), despite posting a 10% recovery in the last five trading sessions.

With total debt of $162 billion, Oracle faces negative sentiment due to the prevailing macro uncertainty. The company is on track to increase its long-term debt significantly over the course of just two years. During the same period, free cash flow per share has gone from $4.30 to -$8.70 per share. The negative sentiment is justified to an extent, but do the growth prospects make this poor cash flow worth it?

The projected earnings growth rate according to Wall Street analysts is 7% for fiscal 2027, 35% for 2028, and 48% for 2029. There is a pattern here, which is that the growth is a bit too far down the road for investors to be comfortable. This adds execution risk, which is not compensated for by the forward price-to-earnings (P/E) ratio of 29.3 times, which is close to the sector median as well as the stock’s five-year average. ORCL stock isn’t cheap, although the 1.12% dividend yield provides some comfort.

Oracle Continues to Raise the Bar

Oracle announced its fiscal third-quarter 2026 earnings on March 10. EPS of $1.79 exceeded Wall Street expectations of $1.70, while revenue came in at $17.19 billion, comfortably ahead of the consensus estimate of $16.91 billion. The most interesting part of the earnings announcement was the remaining performance obligations (RPO) figure, which has now ballooned to $553 billion, allowing analysts to confidently add sustainable future revenue to their financial models.

One notable comment from management explains why some investors continue to ignore the debt figure. According to the company, most of the RPO is connected to those customers who either pay upfront or buy the GPUs themselves and hand them over to Oracle. This approach mitigates the risk arising from the capital-intensive nature of AI investments. The company expects to overdeliver on the fiscal 2026 revenue promise and is constantly raising fiscal 2027 revenue forecasts, expecting the company’s operations to grow more valuable over time.

What Are Analysts Saying About Oracle Stock?

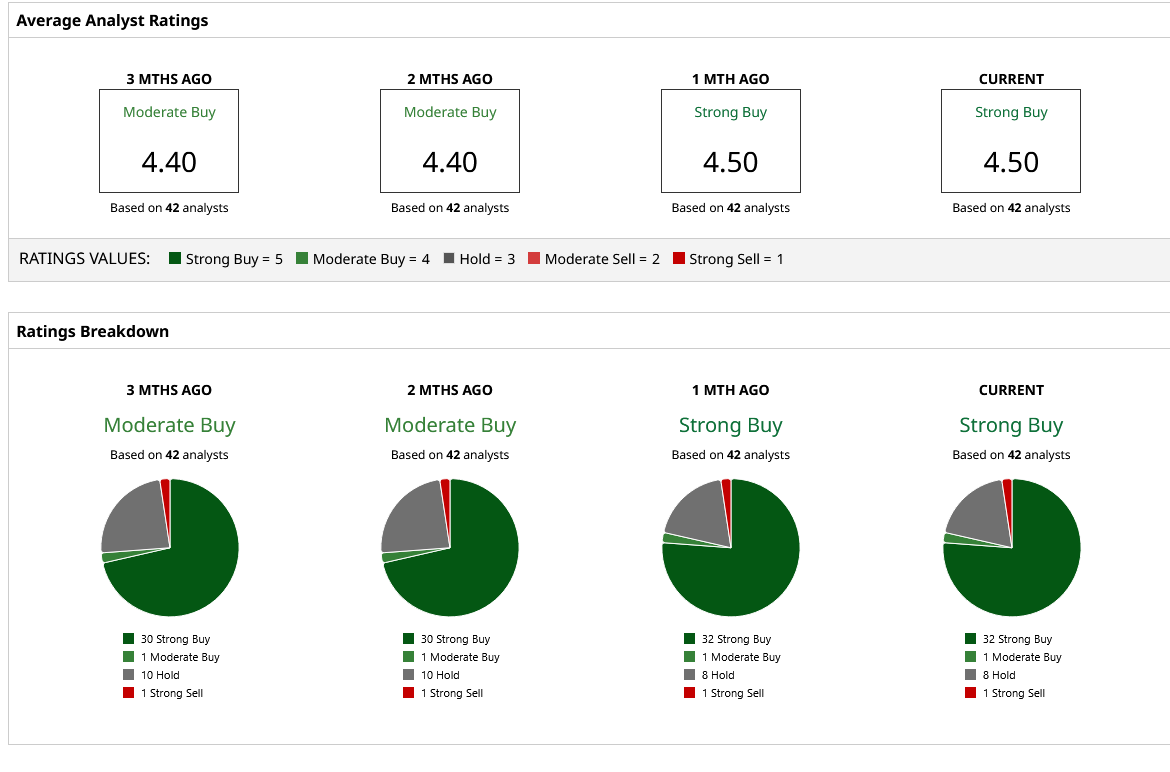

Analysts have been cautious on Oracle’s prospects during the last one month, with no upward price target revisions during the period. Still, a vast majority of the 42 analysts covering ORCL stock assign a “Strong Buy” rating. The mean target price of $253.21 suggests further upside of 43% from here, which shows how far the stock has fallen over the last six months. At one point in 2025, ORCL stock traded at roughly double the price that it now trades at today.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)