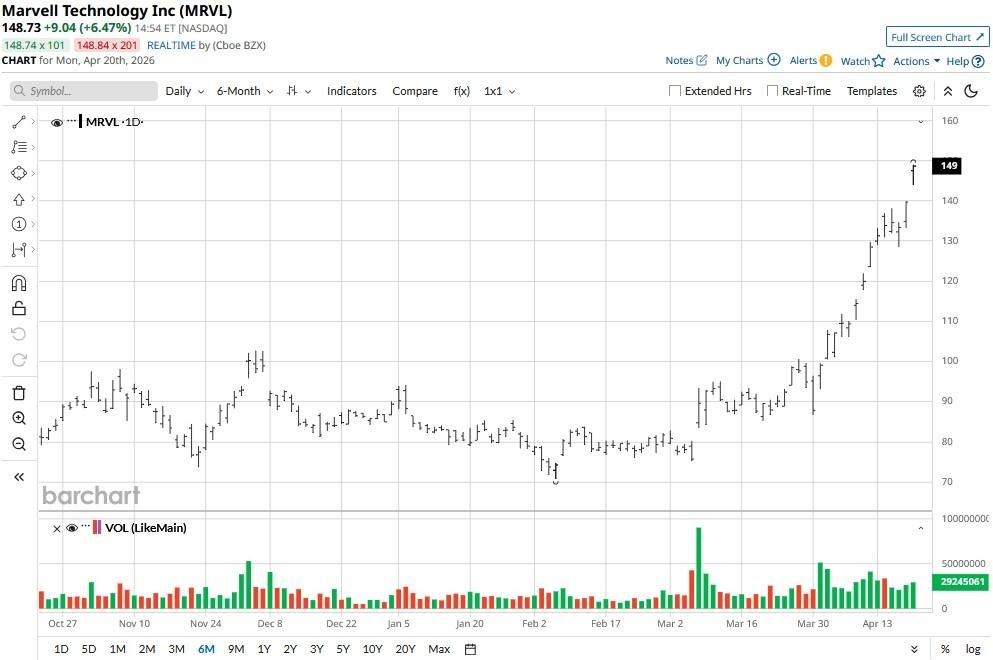

Marvell Technology (MRVL) shares are trading at a record high on Monday following reports that Alphabet's (GOOG) (GOOGL) Google is in talks with it to co-develop two of its new artificial intelligence (AI) centric processors.

Following today’s rally, MRVL’s relative strength index (RSI) has pierced the mid-80s, a technical setup that often signals a pullback ahead.

Still, the case for owning Marvell stock, which has already doubled this year, remains strong as ever for long-term investors.

Why Marvell Stock Rallied on Monday

A potential team-up with Google could prove a game-changer for MRVL stock, validating the firm as a premier alternative to Broadcom for custom ASICs.

According to media reports, the multinational is considering partnering with Marvell on a memory processing unit (MPU) and a new inference-optimized TPU to boost the efficiency of its AI models.

If MRVL does indeed succeed in winning a spot in Google’s silicon supply chain, its footprint in the fast-growing inference market will grow significantly in 2026.

In short, such an agreement will add billions to Marvell’s annual revenue – potentially bringing it similar proposals from other hyperscalers as well, as they look to reduce efficiency taxes and hardware costs.

What Makes MRVL Shares Attractive for 2026

If Google selects Marvell for its custom AI silicon, it will add to the company’s growing roster of high-profile custom chip contracts, which already includes industry titans Amazon (AMZN) and Microsoft (MSFT).

Meanwhile, the space leader, Nvidia’s (NVDA) recent $2 billion investment in MRVL serves as the ultimate seal of approval.

The firm’s dominance in high-speed optical interconnects (800G and 1.6T) makes it an essential picks-and-shovels play for artificial intelligence infrastructure.

At about 44x forward earnings, Marvell sure is trading at a premium, but its projected sales growth toward $15 billion within the next three years suggests the valuation is actually supported by huge scaling potential.

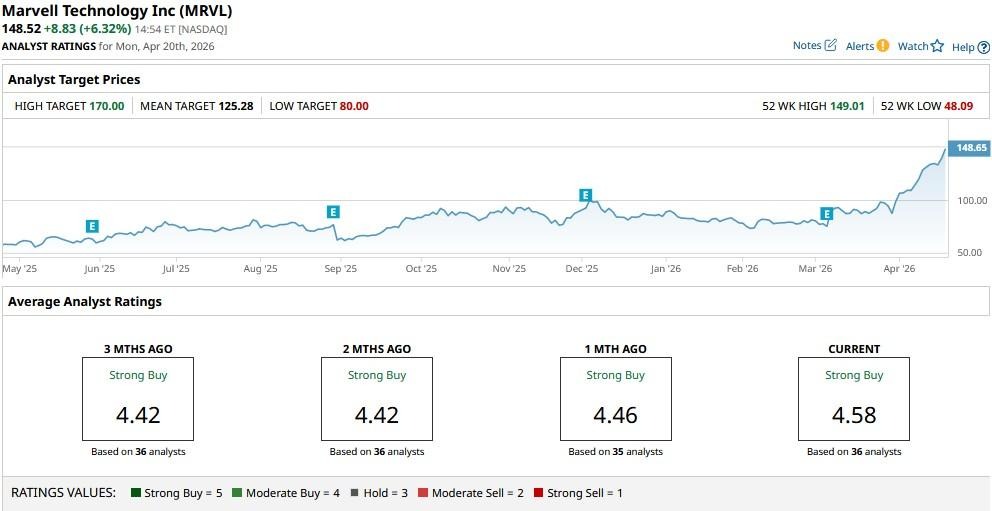

Wall Street Remains Bullish on Marvell Technology

Wall Street continues to recommend owning Marvell Technology in 2026, especially since it pays a small dividend yield of 0.16% as well.

The consensus rating on MRVL shares sits at “Strong Buy” currently, with price objectives as high as $170, indicating potential upside of another 14% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)