Howdy market watchers!

Another week just flew by with even more volatility! While it was widely expected eventually, but completely unknown on timing, the Iranian regime announced on Friday morning that the Strait of Hormuz was ‘completely’ open to shipping although President Trump said the blockade of Iran’s ports remains active. The Trump Administration did, of course, reiterate the openness of the channel and thanked Tehran. This followed the earlier truce announced between Israel and the Hezbollah in Lebanon.

BREAKING NEWS: Having said all of that, on Saturday morning, Iran announced that the Strait of Hormuz would close again with the US blockade remaining in place. A vessel attempting to pass through came under gunfire by Iran's military punctuating that news. If tensions re-escalate further over the weekend, we could see a huge surge back higher in crude oil and selloff in stock index futures. Link to breaking news: Iran reimposes control over Strait of Hormuz as ships report gunfire | Reuters

The momentum seems to be building for peace although it is becoming more apparent to me, as outlined in last week’s article, that the Trump Administration is close to desperate for an off-ramp as the Republican and MAGA ranks are beginning to fracture to varying degrees with the Iranian conflict, on one hand, and the critical, Mid-Term elections ahead, on the other. The urgency of achieving some stability in rising gas prices and lower, uncertain equity markets has reached the boiling over point as tight, financial conditions are pressuring households and businesses of all sizes.

The newly nominated Fed Chair, Kevin Warsh, has started his confirmation process with plenty of headlines as the next FOMC meeting approaches on May 4-5th with elevated fuel prices that could indeed be “transitory” and not require monetary policy action. Excluding volatile food and energy prices, with energy also being a large part of food costs, inflation is trending in line with expectations and near 2.6 percent, but still above the target of 2.0 percent of the Federal Reserve.

The US dollar index has recently weakened, gapping lower on April 8th. This has been and will become a tailwind for commodities if sustained. A weaker US dollar trends with lower interest rates and vice versa. Let's hope this weaker US dollar can persist and foreshadow measured cuts in interest rates, especially for the bottom leg of this “K” shaped economy that is widening.

However, there is so much noise in the data at present that interpretation is a slippery slope. Having said that, if tensions ease on a sustained basis and the equity markets continue to rally, inflationary concerns could continue to be a real issue even if energy prices selloff further. It will be an interesting next couple of months as election mode sets in and rhetoric shifts swiftly to winning votes.

The grain markets managed to rebound this week after recent weakness while soybeans staged an outside, reversal lower day to start the week after last week’s break higher. KC wheat, in particular, has been the leader with Thursday's highs usurping the prior March highs of late and trading the highest level in one year!

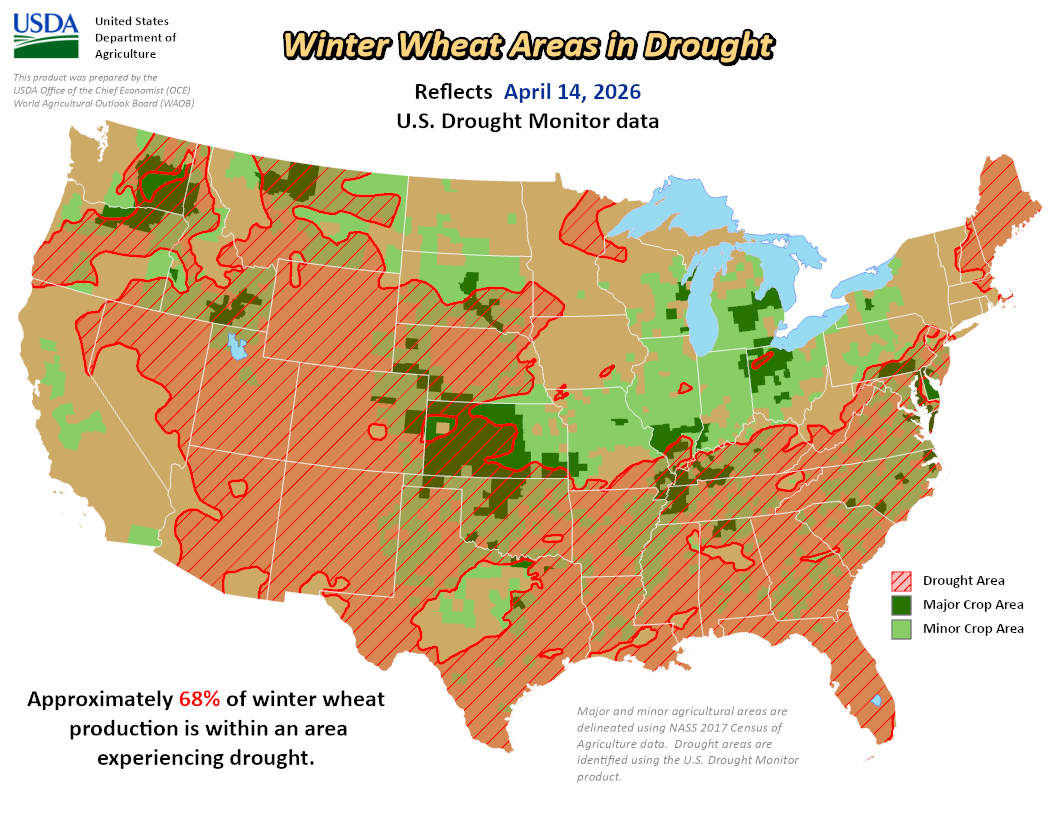

The wheat market has continued to be in the lead for ag commodities with the charts gapping higher on last Sunday night’s opening with the gap remining unfilled on Friday’s close. Rain chances with severe storms passed through northwestern Oklahoma and parts of Kansas on Friday afternoon into evening, but it will do little to reverse the damage that has been done from months of drought and hot temperatures across the Southern Plains.

Crop insurance claims continue to roll in on winter wheat fields that will not be harvested. My dad always said that wheat has 9-lives, but this year does indeed seem to be different in the prospects of recovery even should the weather dramatically shift to cooler and wetter. US winter wheat conditions released this past Monday came in at 34 percent Good-to-Excellent versus 35 percent expected and 47 percent last year. Oklahoma’s G/E ratings were 10 percent versus 44 percent last year, Texas at 15 percent versus 23 percent last year, Nebraska 14 percent versus 30 percent and Kansas at 32 percent versus 43 percent.

Corn planting is getting started at 5 percent complete, slightly behind expectations of 6 percent, but ahead of last year’s 4 percent. Soybean planting is also well ahead of schedule at 6 percent complete versus just 2 percent expected and average for this time of year.

Active weather patterns have delayed some plantings in the Midwest, but it is still early and unlikely to be reflected in prices unless there is continued delays.

The plunge in crude oil prices hints to lower fertilizer prices, but that is far from certain and unlikely for this season given delays in shipments as well as consolidation in fertilizer distribution. Summer crop “top dressing” and “new crop” in South America will feel the bulk of the price pinch first, but the real question will be the cost of inputs for the 2027 crop in the US that begins in the fall/winter of 2026.

Unfortunately, I believe this situation is far from over and the current pause is just that, a pause. Leverage will continue to build and politics will continue to be at play until the next pinch unfolds.

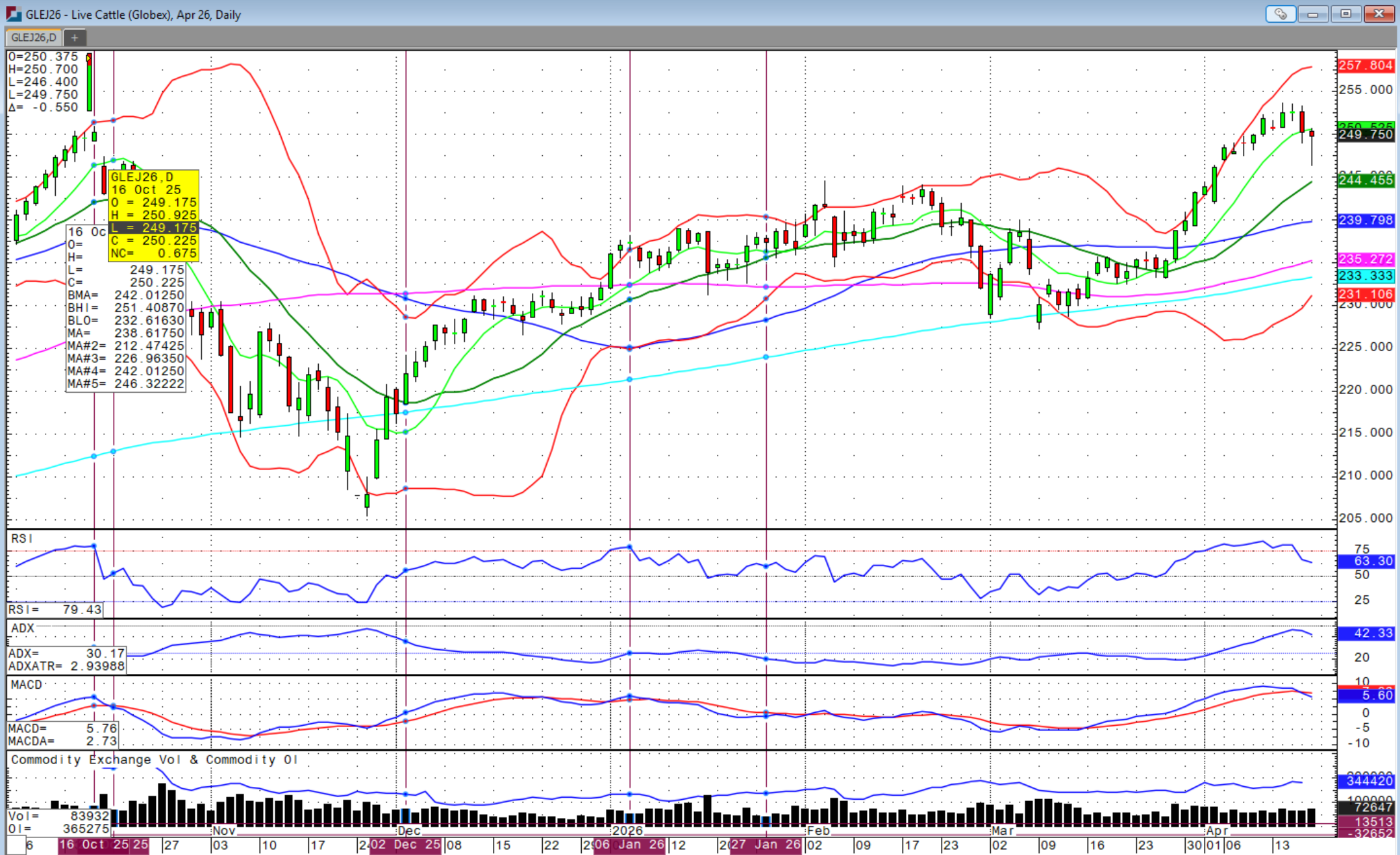

The cattle market has been the bright spot despite continued selling pressure in equities with fed cattle cash trade inching higher. On Tuesday, all feeder futures contracts filled the upper chart gap that was created all the way back on October 16th and made new, all-time highs. Markets surged, but closed well off the highs on that session although still closed positive.

Futures chopped sideways the following session, but then came under pressure on Thursday with heavy selling on Friday that saw contracts limit-down for May and latter futures, but rebounded well off the lows into the close. April feeders, in fact, closed the session above Thursday’s lows after trading all the way down to the 20-day moving average just above $366.50.

Cash fed cattle traded all week starting Monday with highs at $248 all the way down to Texas. The cash market remains strong with demand prospects improving and numbers continuing to tighten. If a sustained decline in gas prices can be accompanied by a sustained rebound in the stock market and improved sentiment overall, I believe beef demand overall can also rebound.

Friday’s USDA Cattle-on-Feed report had a slightly bullish bias with April 1st on-feed coming right in line with expectations at 99.5 percent of last year, but March placements coming in at 92.7 percent versus 92.9 percent expected. March marketings were slightly higher than expected ta 94.5 percent versus 93.8 percent expected.

When futures markets trade new highs, we often see some selling pressure. However, if gas prices soften, the stock market strengthens and overall sentiment improves going into summer, I could see this cattle market retesting recent highs again in the coming weeks/months.

Remember, we are in the extremes of uncharted territory in the cattle markets. No matter how normal and justified this price level currently feels, it is unlikely to be the “new normal”. Markets may and often go higher than expected and could yet still go higher. There will however be a point where these prices will be unjustified. We haven’t said it in awhile, but these cattle prices are likely equivalent to $12+ wheat. It may continue to last and then last longer than thought until suddenly it doesn’t and then it will seem like miles away.

Call Sidwell Strategies to develop longer term price protection strategies in the market to make this rally “last” for your operation.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/The%20sign%20for%20Marvell%20Technology%20out%20front%20of%20a%20corporate%20office%20by%20Valeriya%20Zankovych%20via%20Shutterstock.jpg)

/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)