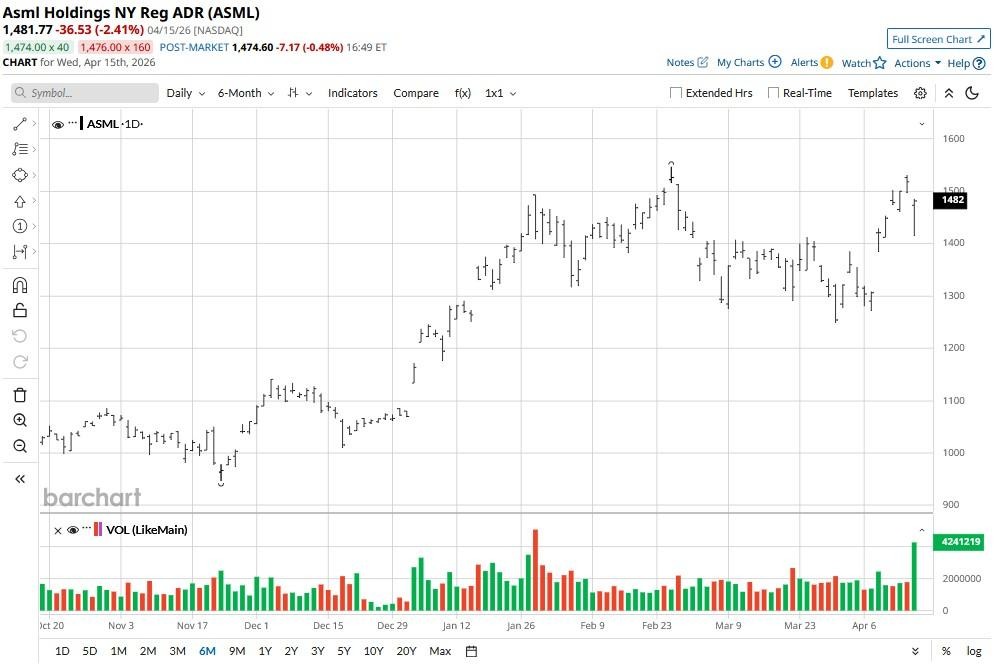

ASML (ASML) closed down on April 15 as management’s muted Q2 guidance tempered the firm’s strong first-quarter release, featuring better-than-expected earnings and revenue.

Its gross margin came in at a whopping 53% (at the high end of the guided range), signaling demand from chipmakers building out artificial intelligence (AI) infrastructure.

Despite the post-earnings dip, ASML stock remains up more than 25% versus its year-to-date low.

China Remains an Overhang on ASML Stock

ASML reported $10.4 billion in net sales for Q1 on Wednesday, slightly beating the consensus estimate.

However, a significant overhang on ASML shares is the shrinking China business.

Net system sales to Beijing declined to just 19% of the Q1 total, down significantly from 36% in the prior quarter, reflecting tightening export controls and normalization pressures.

Proposed U.S. legislation known as the MATCH Act could further restrict ASML’s ability to ship equipment to Chinese customers.

In the earnings release, chief executive Christopher Fourquet acknowledged this risk but said the firm’s 2026 guidance bandwidth — between 36 billion and 40 billion euros in revenue — already accommodates potential outcomes of ongoing export control discussions.

The Bull Case for ASML Shares

On the flip side, a dramatic surge in South Korea, which accounted for 45% of net system sales in Q1, helped offset the aforementioned China headwind.

SK Hynix placed a record EUV order that stretches through next year, and memory chip-makers report being sold out for 2026.

The memory segment now represents more than half of ASML’s tool sales, a structural shift driven by insatiable artificial intelligence-related demand for high-bandwidth memory.

Moreover, ASML’s competitive position remains unassailable. It’s the sole manufacturer of EUV lithography machines, which can cost $300 million each.

Management indicated plans to ship 60 low-NA EUV systems in 2026, a 25% increase over 2025, with capacity for 80 units in 2027.

This order pipeline from both logic and memory clients is expected to keep the company operating at full capacity through the end of next year, with EUV sales projected to surpass 50% of the total product mix beyond 2026.

This monopolistic position in an essential technology is bullish for ASML stock as it creates a durable competitive moat that few industrial companies anywhere can match.

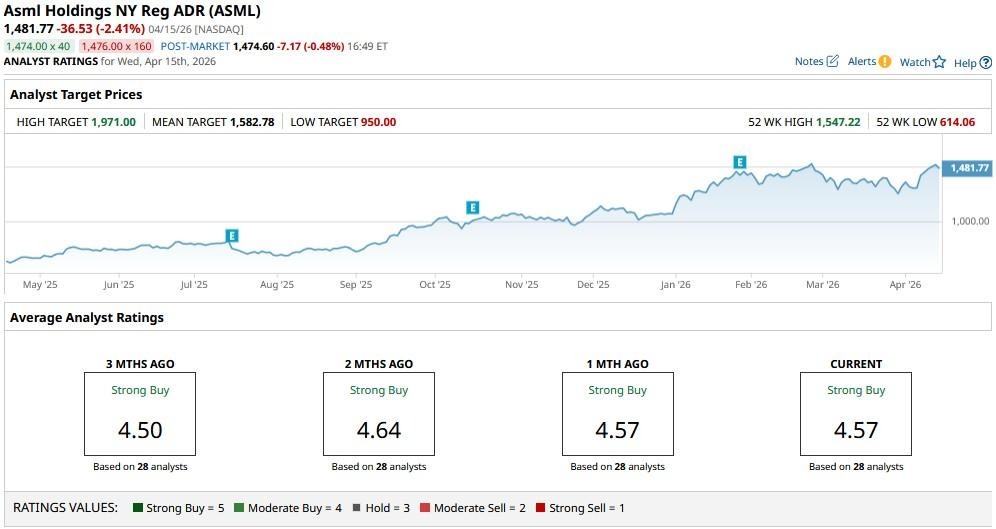

What’s the Consensus Rating on ASML?

Long-term investors should consider buying the post-earnings dip in ASML also because the Wall Street firms remain constructive on this Dutch behemoth.

The consensus rating on ASML shares sits at “Strong Buy,” with price targets as high as $1,971, indicating potential upside of about 33% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)