/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

Palantir Technologies (PLTR) stock has fallen sharply in recent months, dropping more than 32% from the 52-week high of $207.52. The decline comes despite the company consistently reporting an acceleration in top-line growth, driven by strong demand for its Artificial Intelligence Platform (AIP).

One of the major concerns among investors is valuation. Before the pullback, Palantir traded at very high multiples relative to its peers. Due to its extremely high valuation multiples, PLTR stock was vulnerable to corrections.

Meanwhile, competitive pressure in the fast-moving artificial intelligence (AI) sector has also weighed on market sentiment. Rapid enterprise adoption of Anthropic's models has raised questions about the durability of Palantir’s competitive advantage as companies evaluate different AI providers. The emergence of strong alternatives can shift expectations for future growth, often affecting technology stocks with premium valuations.

Investor sentiment was further influenced by comments from Michael Burry, who has expressed skepticism about the company’s outlook. This added to PLTR stock's volatility.

Despite these pressures, Palantir’s core business trends remain positive. The company continues to see strong demand for AIP. At the same time, Palantir has been expanding its profit margins, which supports its investment case.

While Palantir still trades at a premium relative to many software companies, the correction has eased some valuation concerns.

Palantir’s Growth Outlook Remains Strong

Despite the notable drop in Palantir stock, strong demand could continue to drive the company’s financials at a solid pace. Notably, 2026 could be another year of rapid growth for the company. The firm forecasts revenue between $7.182 billion and $7.198 billion for the year. The midpoint of this guidance, $7.19 billion, implies about 61% year-over-year (YOY) growth, representing acceleration from the 56% growth recorded in 2025.

The catalyst supporting Palantir’s growth is AIP, as adoption of platform has been strong. In the fourth quarter, Palantir’s U.S. business expanded 93% compared with the same period a year earlier and grew 22% from the previous quarter, driven by higher adoption of AIP.

Within this segment, the commercial business could again be a standout performer. U.S. commercial revenue increased 137% YOY in Q4 and rose 28% sequentially, following rapid growth in previous quarters. The segment posted 121% YOY growth in Q3 and 93% growth in Q2, indicating that enterprise demand for AI-driven data platforms is strengthening.

Palantir’s contract pipeline remains solid. It reported a record quarterly total contract value of $4.3 billion in Q4. At the same time, revenue from the company’s largest clients continues to rise. Over the past 12 months, the average revenue generated from Palantir’s top 20 customers increased 45% YOY to $94 million per client.

Commercial demand in the U.S. is expected to remain a key growth engine. Palantir estimates that U.S. commercial revenue will surpass $3.144 billion in 2026, implying growth of at least 115%. By comparison, the segment generated $1.465 billion in 2025.

Government contracts also continue to support PLTR stock’s growth. Palantir has long worked with defense and intelligence agencies, and demand from the public sector remains strong. In Q4, revenue from the U.S. government business rose 66% YOY and 17% from the previous quarter. As geopolitical tensions rise and governments invest more heavily in advanced analytics, spending on AI-enabled intelligence and logistics platforms is expected to remain elevated.

Palantir’s profitability is improving alongside revenue growth. In Q4, Palantir generated $798 million in adjusted operating income, representing a 57% operating margin. That margin figure increased from 45% in the same period a year earlier, reflecting higher sales and operating efficiency.

Looking ahead, management expects further gains. Adjusted operating income is projected to range from $4.126 billion to $4.142 billion in 2026, up significantly from $2.254 billion in 2025.

In short, accelerating revenue growth, expanding margins, and strong demand for AIP suggest that Palantir’s business still has solid growth ahead despite competitive headwinds.

Is PLTR Stock a Buy Now?

The solid demand for AIP, strong momentum in the U.S. commercial business, strength in the government segment, and significant margin expansion indicate solid growth ahead for Palantir. As a result, PLTR stock could see a recovery.

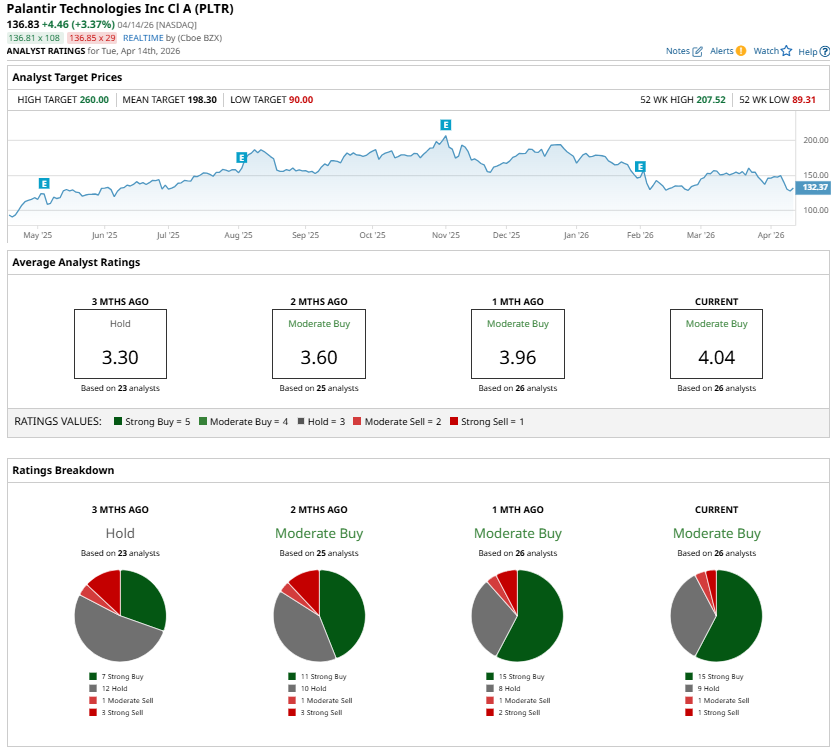

However, PLTR stock still trades at a premium valuation, suggesting it could remain volatile. Overall, analysts currently give PLTR stock a “Moderate Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)