The global spirits business looks set to enter another round of deal‑making, as big groups seek greater scale amid softer demand, shifting tastes, and lingering inventory and economic pressures.

Just weeks after Brown‑Forman (BF.B) discussed a possible “merger of equals” with French giant Pernod Ricard (PRNDY), fresh reports on April 9, 2026, highlighted new interest in the company. The privately held U.S. rival Sazerac, owner of Buffalo Trace, Fireball, and Pappy Van Winkle, has also approached the Jack Daniel’s maker about a potential deal.

That headline sent Brown‑Forman’s shares sharply higher, with the stock jumping roughly 12% intraday on talk that a bidding battle could be brewing. The Kentucky‑based company behind Jack Daniel has long been seen as a high‑quality, family‑influenced blue chip in the sector.

With deal rumors now coming from more than one direction and the stock already trading at a premium valuation, the obvious question for dividend investors is simple. Does the prospect of an M&A bump make Brown‑Forman a buy at today’s price, or is it better to wait for clearer news and a possible cheaper entry point? Let’s dive in.

Brown‑Forman’s Numbers

Brown‑Forman is headquartered in Louisville, Kentucky, and owns a long list of well‑known brands, including Jack Daniel’s, Woodford Reserve, Old Forester, Herradura, and Finlandia.

Its Class B shares are at $29.65 as of April 13, up 13% this year and down 14% over the past 52 weeks.

BF.B stock trades at 17.62x earnings and 14.99x cash flow, compared with sector medians of 16.54x and 11.26x, so investors are paying a clear premium for the business.

The stock pays a forward annual dividend of $0.92 per share, yielding 3.05% at the current price of $29.49. That yield is not dramatic, but it is consistent and well covered by a company that has been paying and growing its dividend for 17 years.

Brown-Forman's latest quarter, ending in January 2026, showed EPS of $0.58 versus a $0.48 estimate, a 20.83% beat that points to stronger profit than the market expected. The company reported sales of $1.056 billion, up 1.93%, which is not rapid growth but still supports its dividend and income story.

The same report showed net income of $267 million, up 19.20% year-over-year (YoY), helped by cost control and a better mix. This kind of profit growth helps back both the dividend and any buybacks management chooses to make. Brown-Forman also posted operating cash flow of $709 million, up 142.81%. That net cash flow number was still negative at -$61 million, but the 51.20% improvement from the prior year suggests the cash picture is moving the right way.

Brown-Forman Weighs Strategic Moves

Potential buyers circling Brown‑Forman are not looking at a worn‑out legacy name. They are looking at a company already weighing its own options, including a recently discussed “merger of equals” idea with Pernod Ricard that could create a larger global spirits group with more scale, more brands, and wider reach.

This sits alongside separate reports that Sazerac has allegedly approached Brown‑Forman about a possible deal, which adds to the questions around where the company’s ownership and structure might go next.

Another important angle is how management is treating shareholders while all this is in motion. On Oct. 1, 2025, the board approved a $400 million share buyback for both Class A and Class B shares, running through Oct. 1, 2026, and funded by strong cash generation.

Street Expectations and What They Signal

Analysts still expect Brown‑Forman to keep growing, with the next earnings release set for June 4, 2026. The current quarter (April 2026) has an average EPS estimate of $0.34 versus $0.31 a year ago, which works out to about 9.68% growth. That is steady, single‑digit progress and points to a fairly predictable profit path rather than a big swing story.

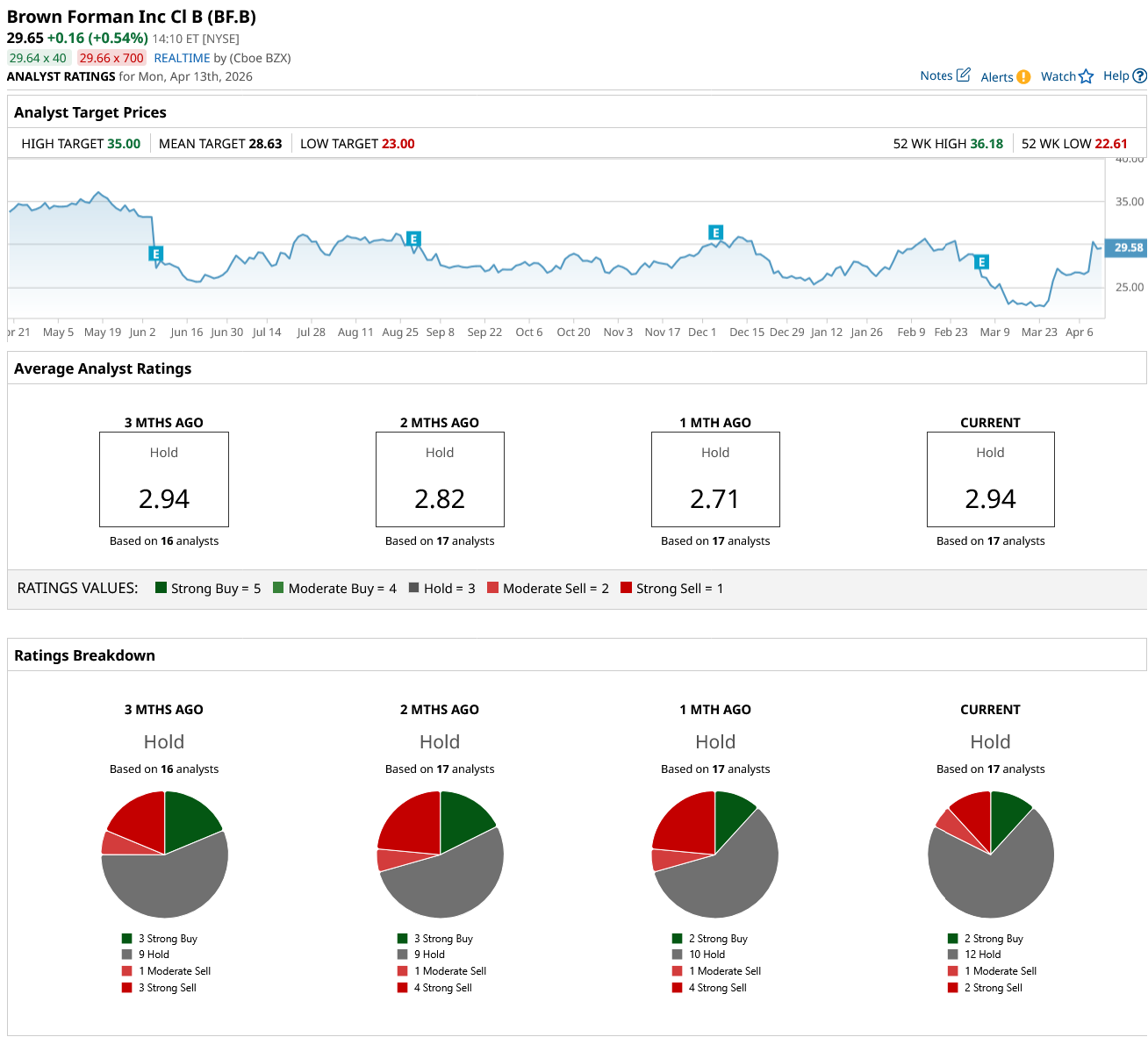

That said, the analyst community is hardly euphoric. BNP Paribas Exane cut its rating from “Neutral” to “Underperform” on Jan. 20 and dropped its target from $31 to $24, flagging concerns that the growth outlook may not fully support the previous valuation.

Across the broader Street view, the shares sit at a consensus “Hold” based on 17 analyst opinions, not a clear green or red light. Their average target of $28.63 implies roughly a 3% downside instead of upside. That gap between a flat Wall Street stance and the possibility of a Sazerac deal leaves investors in a genuinely tricky spot as they decide whether to buy, hold, or wait.

Conclusion

All the talk about deals and buyouts does not suddenly turn Brown‑Forman into a must‑buy at today’s price. The stock already bakes in a solid dividend, steady growth, and a quality premium, and most analysts are still on the fence. Presently, it looks more like a slow‑and‑steady hold for income‑focused investors than a punchy new buy. Over the next year, the risk‑reward picture points to fairly modest, range‑bound returns unless a real takeover offer lands and reshapes the story.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Businessman%20work%20with%20ai%20for%20economy%20analysis%20financial%20result%20by%20digital%20augmented%20reality%20graph%20by%20Natee%20K%20Jindakum%20via%20Shutterstock.jpg)