Unity Software (U) recently locked in a major vote of confidence from one of the most powerful companies in tech. On April 8, 2026, Unity and Meta Platforms (META) announced an extended multi-year partnership focused on virtual reality (VR) development. The deal deepens a collaboration that has made Unity the backbone of the VR gaming ecosystem.

So, does this change the outlook on U stock? Here's what you need to know.

Why the Meta-Unity VR Deal Matters for Unity stock

The partnership signals that Meta, the undisputed leader in consumer VR hardware, is doubling down on Unity as its go-to development platform.

"Unity powers the majority of its top-selling VR games," Unity COO Alex Blum said in a company statement. It means that the games driving revenue on Meta Quest devices are largely being built on Unity's engine. Meta VP Ryan Cairns echoed the sentiment. "Unity is a critical partner for Meta across multiple initiatives, including our investment in the VR developer community," Cairns said.

VR as a category has struggled to go truly mainstream. But Meta has invested billions in pushing adoption. If that bet pays off and the Meta Quest lineup continues to grow, Unity stands to capture a significant share of that developer spending.

Unity provides the engine, runtime, tooling, and distribution infrastructure that let developers build once and deploy everywhere. In VR, that kind of platform neutrality is a real competitive edge.

Unity’s Business Momentum Is Gaining Traction

Before you factor in the Meta deal, Unity's underlying numbers were already turning heads.

On March 26, 2026, the company reported preliminary first-quarter 2026 results that blew past its own guidance.

- Unity now expects Q1 revenue of $505 million to $508 million, compared to prior guidance of $480 million to $490 million.

- Adjusted EBITDA is projected at $130 million to $135 million, up 58% year-over-year (YoY) and well above the guided range of $105 million to $110 million.

Unity Vector, the company's artificial intelligence-powered advertising platform, which is expected to grow 15% sequentially in Q1. That follows three straight quarters of mid-teens sequential growth. In January, Vector posted its best revenue month ever, up 72% compared to January of the previous year.

Unity CEO Matt Bromberg was direct about what's fueling the beat. "Unity Vector continues to deliver robust growth each quarter, driving results meaningfully above our guidance," Bromberg said.

Moreover, Unity announced it will shut down the IronSource Ads Network, effective April 30, 2026, and is exploring the sale of its Supersonic game publishing business, according to a company statement.

IronSource was a legacy, lower-margin ad network that was dragging on Unity's overall growth numbers. By sunsetting it, Unity is clearing the deck for Vector, a higher-margin, AI-native platform, to take center stage.

Once IronSource is gone, the company's strategic Grow revenue (which already excludes IronSource) is expected to increase 48% YoY in Q1. Total Grow revenue, including IronSource, is projected to grow just 24%, underscoring how much the legacy network was holding back the headline number.

So Is U Stock a Buy, Sell, or Hold?

The bull case here is real and getting stronger. Vector is scaling fast, the Create business is growing again, margins are expanding, and now Meta is publicly reaffirming Unity as its core VR partner.

Unity is not a speculative bet on VR alone. It's a platform company with a strong position in gaming, a fast-growing AI ad business, and a widening developer ecosystem. The cleanup of non-strategic businesses should make the financials easier to read and harder to ignore. That said, competition from AppLovin (APP) in the ad space remains intense, and VR adoption as a category is still not a sure thing.

For investors with a medium-to-long-term horizon, Unity looks more like a “Buy” than a “Hold.” The pieces are coming together faster than the market may be pricing in.

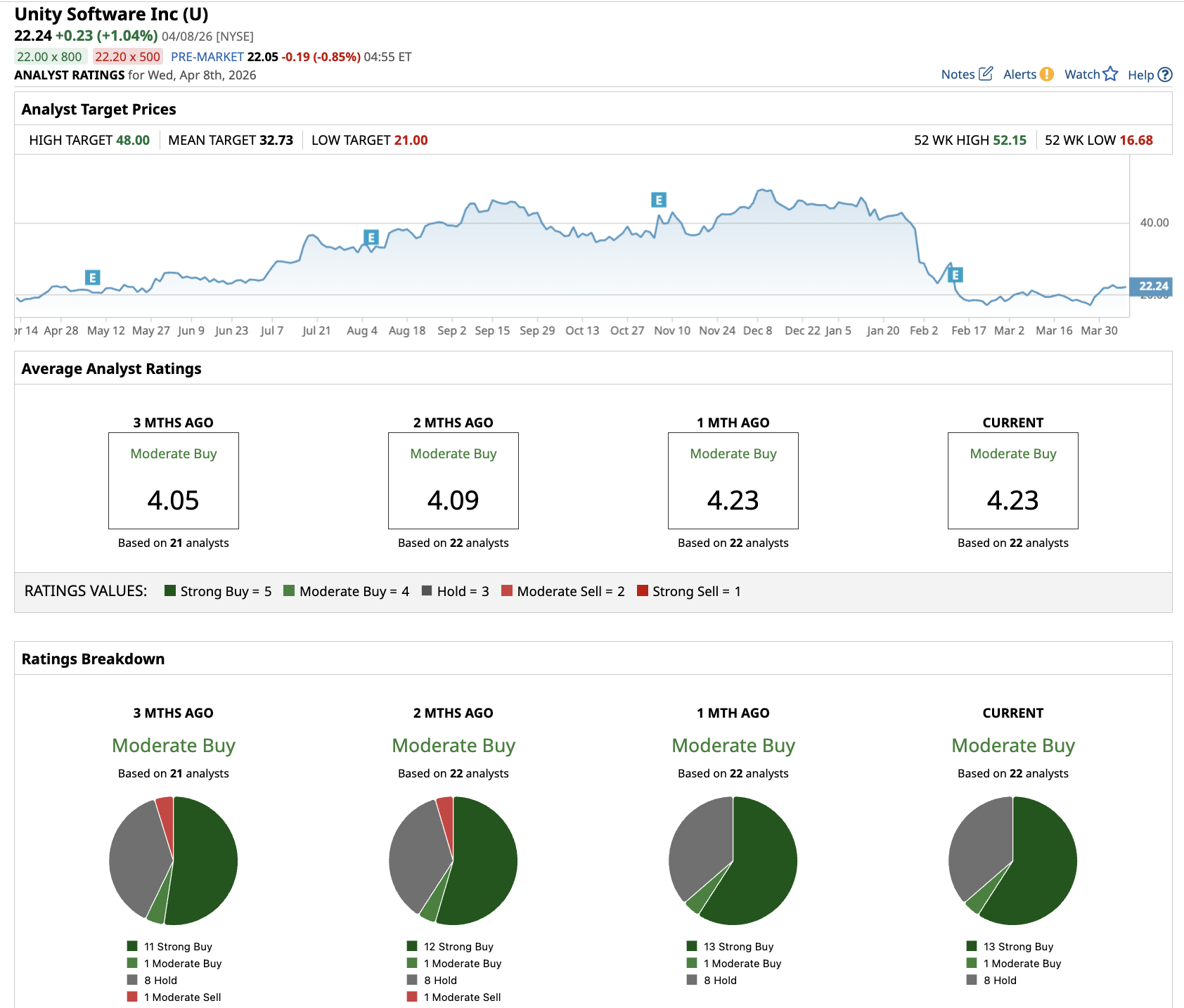

And analysts mostly agree with this outlook. Out of the 22 analysts covering U stock, 13 recommend “Strong Buy,” one recommends “Moderate Buy,” and eight recommend “Hold.” The average U stock price target is $32.73, above the current price of about $22.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)