/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Intel (INTC) stock has extended its strong momentum into 2026, following a significant rally in 2025. In the current year, shares have continued to advance, rising more than 70% year-to-date (YTD). The recent surge has accelerated in the past week, with INTC climbing about 25% over the last five trading days.

Part of this rally followed Intel’s announcement that it will participate in Elon Musk’s Terafab project. The development has boosted investor optimism around Intel’s potential role in large-scale technology infrastructure initiatives.

Investor sentiment was further supported by Intel’s expanded partnership with Alphabet’s (GOOG) (GOOGL) Google. The two companies recently announced a major multi-year agreement focused on artificial intelligence (AI) data center infrastructure.

Under the partnership, Google plans to deploy next-generation Intel Xeon processors while collaborating with Intel to develop custom Infrastructure Processing Units (IPUs) designed to handle rapidly growing AI and cloud workloads. The initiative reflects Intel’s broader strategy to strengthen its position in the accelerating market for AI and cloud infrastructure.

With Intel expected to announce its first-quarter earnings report on Thursday, April 23, expectations remain elevated following the stock’s recent gains. Notably, the result and outlook could significantly influence near-term price action. Options markets are currently pricing in a potential move of about 11.7% in either direction following the earnings release for contracts expiring April 24. This expected move is higher than the stock’s average post-earnings move of approximately 8.9% over the previous four quarters.

Recent earnings reactions have also been mixed for the company. Intel shares have declined following three of the past four earnings announcements, including a sharp 17% drop after its fourth-quarter results.

Intel Q1: Here’s What to Expect

Intel is set to report its first-quarter results against a backdrop of ongoing transformation, as the company is positioning itself to capitalize on higher-growth areas such as data-center processors, AI accelerators, and custom silicon.

At the same time, Intel is expanding its semiconductor manufacturing footprint in the U.S., positioning itself as a strategic supplier to governments and technology firms seeking secure, diversified chip supply chains.

In Q1, however, Intel’s financial results may reflect lingering supply constraints. These challenges are expected to weigh most heavily on Intel’s Client Computing Group (CCG) during the first quarter. Notably, supply conditions should begin improving in the second quarter and continue normalizing throughout the rest of the year. If that improvement materializes, Intel could see stronger revenue momentum emerging in the second half of 2026.

For the first quarter, Intel projects revenue between $11.7 billion and $12.7 billion. The midpoint of $12.2 billion implies a year-over-year (YoY) decline compared with the $12.7 billion reported in the same period last year. Within its business segments, the company expects a sharper drop in the PC-focused CCG, partly because internal supply is being directed toward higher-priority server markets.

At the same time, Intel Foundry revenue is projected to rise sequentially by double digits, driven by an increasing mix of extreme ultraviolet (EUV) wafers and improved pricing. Meanwhile, Intel’s Data Center and AI (DCAI) segment is expected to deliver strong growth as supply improves.

Intel is seeing momentum in networking hardware related to the global build-out of AI infrastructure. Intel’s custom ASIC business grew more than 50% in 2025 and surpassed a $1 billion annualized revenue run rate.

While Q1 revenue is projected to decline, Intel expects its bottom line to break even. Notably, Intel has exceeded analysts’ earnings estimates in three of the past four quarters.

Should You Buy INTC Stock?

Intel’s long-term growth outlook remains positive. However, INTC stock has already rallied substantially, rising approximately 216% over the past year. This strong performance suggests that a significant portion of optimism may already be reflected in Intel’s current valuation.

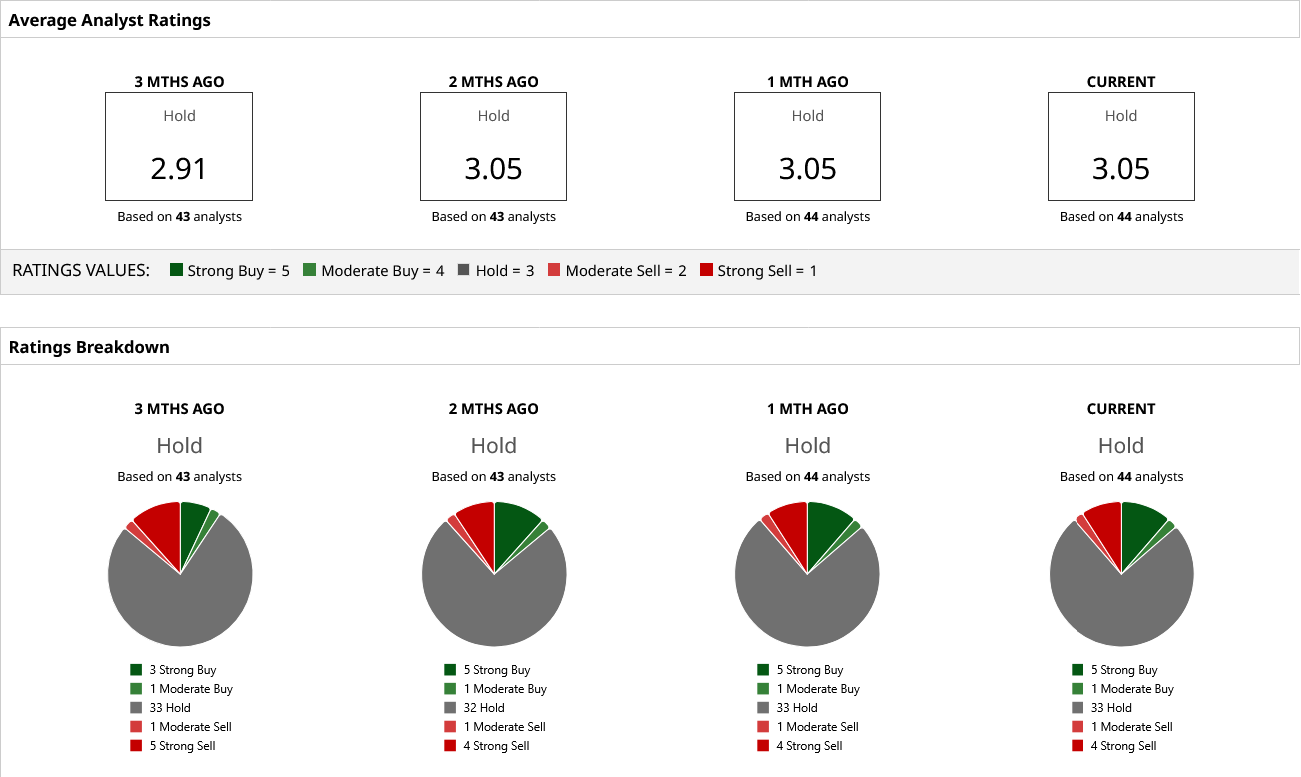

Wall Street analysts currently assign Intel shares a “Hold” consensus rating. Importantly, the stock is trading well above the average analyst price target of $46.79 ahead of the company’s upcoming earnings announcement. This indicates that, despite the company’s favorable long-term prospects, the recent surge in the share price may limit short-term upside.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)