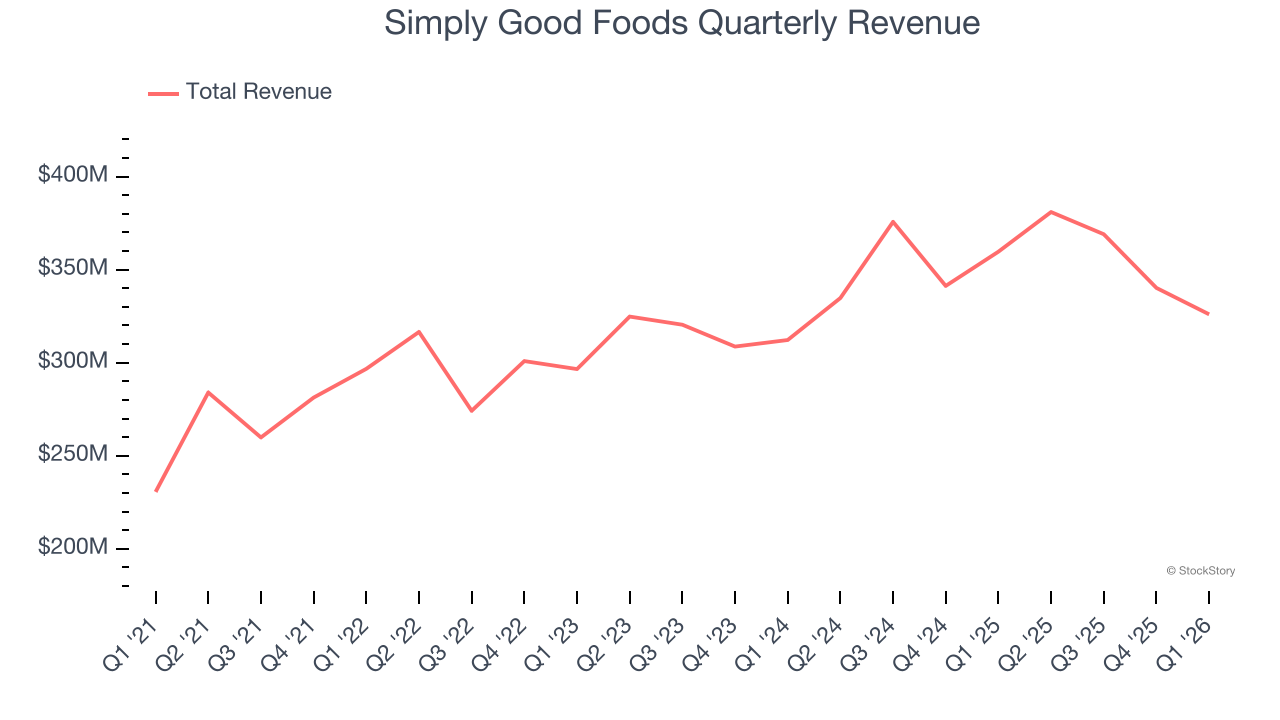

Packaged food company Simply Good Foods (NASDAQ:SMPL) fell short of the market’s revenue expectations in Q1 CY2026, with sales falling 9.4% year on year to $326 million. Next quarter’s revenue guidance of $333.5 million underwhelmed, coming in 11.6% below analysts’ estimates. Its non-GAAP profit of $0.45 per share was 13.6% above analysts’ consensus estimates.

Is now the time to buy Simply Good Foods? Find out by accessing our full research report, it’s free.

Simply Good Foods (SMPL) Q1 CY2026 Highlights:

- Revenue: $326 million vs analyst estimates of $343.8 million (9.4% year-on-year decline, 5.2% miss)

- Adjusted EPS: $0.45 vs analyst estimates of $0.40 (13.6% beat)

- Adjusted EBITDA: $55.51 million vs analyst estimates of $57.06 million (17% margin, 2.7% miss)

- Revenue Guidance for the full year is $1.33 billion at the midpoint, below analyst estimates of $1.44 billion

- EBITDA guidance for the full year is $221 million at the midpoint, below analyst estimates of $267.6 million

- Operating Margin: -65.4%, down from 15.2% in the same quarter last year

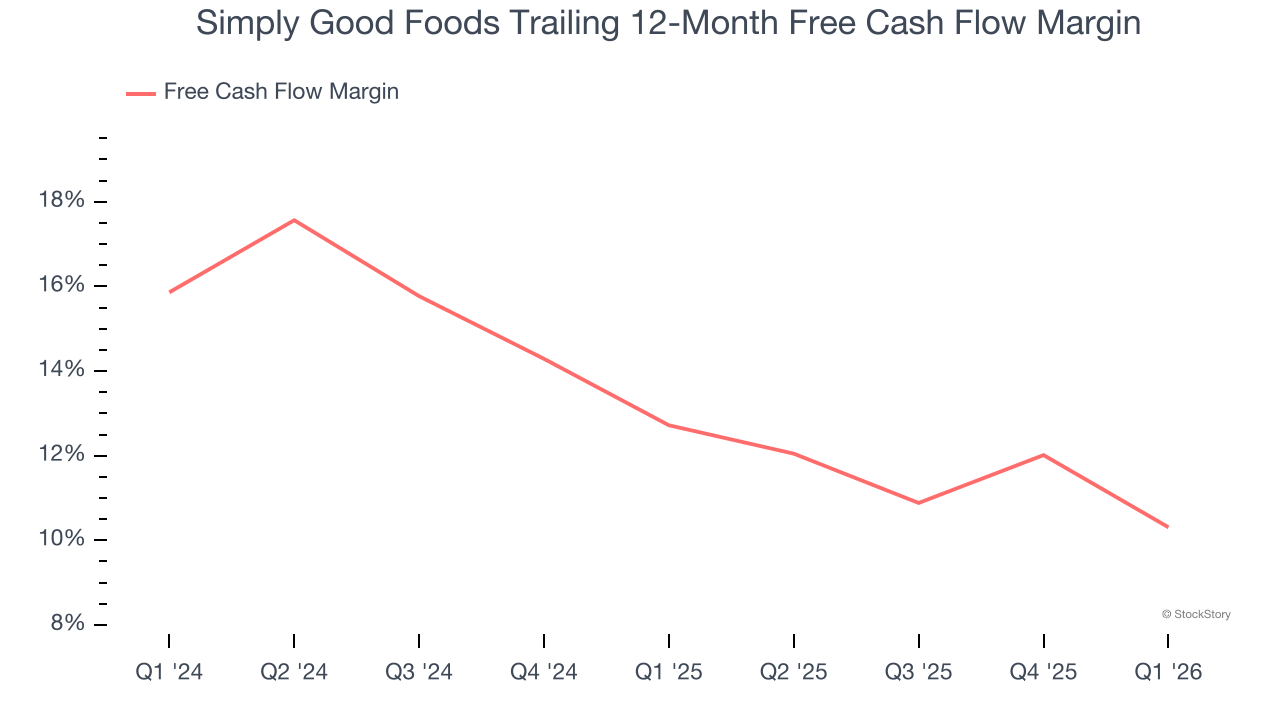

- Free Cash Flow Margin: 0.8%, down from 8.6% in the same quarter last year

- Market Capitalization: $1.33 billion

Company Overview

Best known for its Atkins brand that was inspired by the popular diet of the same name, Simply Good Foods (NASDAQ:SMPL) is a packaged food company whose offerings help customers achieve their healthy eating or weight loss goals.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.42 billion in revenue over the past 12 months, Simply Good Foods is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Simply Good Foods grew its sales at a mediocre 6% compounded annual growth rate over the last three years. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

This quarter, Simply Good Foods missed Wall Street’s estimates and reported a rather uninspiring 9.4% year-on-year revenue decline, generating $326 million of revenue. Company management is currently guiding for a 12.5% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products will face some demand challenges.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Simply Good Foods has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors. The company’s free cash flow margin averaged 11.5% over the last two years, quite impressive for a consumer staples business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Simply Good Foods’s margin dropped by 2.4 percentage points over the last year. Continued declines could signal it is in the middle of an investment cycle.

Simply Good Foods broke even from a free cash flow perspective in Q1. The company’s cash profitability regressed as it was 7.8 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

Key Takeaways from Simply Good Foods’s Q1 Results

It was good to see Simply Good Foods beat analysts’ EPS expectations this quarter. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter was bad. The stock traded down 12.1% to $12.67 immediately after reporting.

The latest quarter from Simply Good Foods’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

/Amazon%20pickup%20%26%20returns%20building%20by%20Bryan%20Angelo%20via%20Unsplash.jpg)