/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

Financial major JPMorgan remains downbeat about Elon Musk-led EV (and increasingly AI) company Tesla (TSLA). Citing risks surrounding increased competition, a decline in deliveries, questions around execution, and diminishing brand value, the Wall Street institution has reiterated its “Underweight” rating on the stock ahead of its Q1 earnings.

In a note to clients, the firm said, “We continue to see large -60% downside to our $145 December 2026 price target and advise investors to approach TSLA shares with a high degree of caution, mindful of execution risk and the time value of money within the context of the materially stronger distant out-year earnings expectations implied by the rise in TSLA share price that has occurred alongside a material collapse in consensus for all performance metrics through at least the end of the decade.”

Notably, the share price performance reflects that weakness, as TSLA stock is down about 23% on a year-to-date (YTD) basis.

What then to make of the stock now? Let's find out.

Q4 Lowdown and Q1 Expectations

Tesla reported another quarter where it beat both revenue and earnings estimates, yet the broader results remained underwhelming.

In Q4 2025, total revenue declined 3% year-over-year (YoY) to $24.9 billion, with automotive revenue falling 11% to $17.7 billion. Earnings per share dropped 17% to $0.50, narrowly surpassing the $0.45 consensus estimate. This marked the fourth consecutive quarter of YoY EPS decline. Over the past nine quarters, Tesla has beaten earnings estimates only three times.

Gross margins narrowed to 5.7% from 6.2% in the prior-year quarter. Operating cash flow decreased 21% to $3.8 billion. The company closed the period with $44.1 billion in cash, ahead of short-term debt of $31.7 billion.

Both production and deliveries declined after a temporary lift from the expiration of federal EV tax credits. Production totaled 434,358 vehicles, down 5% YoY, while deliveries fell 16% to 418,227 units. This became even worse in Q1 2026 as the company reported production and deliveries of 408,386 and 358,023 vehicles (vs. consensus estimates of 365,000 vehicles). However, the figures were up 12.6% and 6.3% on an annual basis, respectively.

On a brighter note, active Full Self-Driving (FSD) subscriptions grew 38% YoY to 1.1 million in Q4. The energy segment continued to show solid momentum, with revenue rising 27% to $12.8 billion. Supercharger stations increased 17% to 8,182, and connectors grew 19% to 77,682.

Valuation remains elevated relative to most large-cap peers. The forward P/E stands at 171.41 versus a sector median of 15.03, while forward P/S of 12.85 and P/CF of 81.19 sit well above sector medians of 0.88 and 9.60.

For Q1, JPMorgan expects Tesla to report an EPS of $0.30 (from $0.43 earlier). The average consensus estimate is $0.24 per share, which would represent a YoY growth rate of 60%.

Q1: Beyond the Numbers

Expectations around Tesla do not just revolve around its vehicles now. Especially since the recent vehicle delivery miss and the complete shutdown of the legacy Model S and Model X production lines are largely priced into the stock, investors are hungry for clarity on the next phase of the company.

The energy storage division will undoubtedly take center stage following a surprisingly weak start to the year. Deployments of Megapack and Powerwall units plunged to just 8.8 gigawatt-hours, missing consensus estimates by a wide margin and falling sharply from the record 14.2 gigawatt-hours recorded late last year. For a business segment that analysts recently championed as the ultimate growth pillar meant to offset sluggish vehicle demand, this 38% sequential decline is a major red flag.

Shareholders will demand to know whether this massive shortfall is simply the result of seasonal timing and temporary supply chain snags or if it exposes deeper structural issues like intensifying price competition and policy uncertainty. The guidance provided here will completely dictate whether energy storage can still be modeled as a reliable, high-margin revenue stream.

Beyond the energy grid, the pivot toward autonomous ride-hailing is the next massive area of scrutiny. With Cybercab manufacturing reportedly kicking off at the Texas Gigafactory this spring, the investment community expects concrete operational updates on the production ramp. Building a dedicated autonomous vehicle without a steering wheel or pedals for under $30,000 sounds incredibly disruptive on paper, but scaling that architecture to millions of units requires staggering capital commitments. Notably, the stakeholders need an update on the status of regulatory approvals, especially since the localized employee testing in Austin must eventually translate into a nationwide rollout if the company wants to capture a meaningful slice of the multitrillion-dollar autonomous transport sector by the end of the decade.

Meanwhile, directly tied to the robotaxi network is the actual adoption rate and the technical progress of the Full Self-Driving software suite. Following the strategic transition to a subscription-only model earlier this year, analysts are eager to see if penetration rates have finally breached the targeted 50% threshold across the consumer fleet. This specific metric is vital because widespread software adoption is the only way to fundamentally alter the margin profile and transition the firm into a highly profitable software enterprise. Analysts will also be listening closely for updates regarding the deployment of unsupervised autonomy in North America and the impending regulatory green lights in European markets. Any unexpected delays in version updates or regulatory pushback could quickly deflate the premium valuation currently assigned to the stock.

Finally, the massive capital expenditure pipeline will also be under intense review. The company recently committed roughly $20 billion toward AI compute clusters, advanced battery facilities, and the commercialization of the Optimus humanoid robot. With the old luxury vehicle lines now being repurposed to assemble the third-generation Optimus, management must justify these enormous cash outlays to a skeptical market. Investors are generally willing to fund a robotics and AI powerhouse, but they require a highly coherent timeline demonstrating when these futuristic bets will generate actual free cash flow.

Analyst Opinion on TSLA Stock

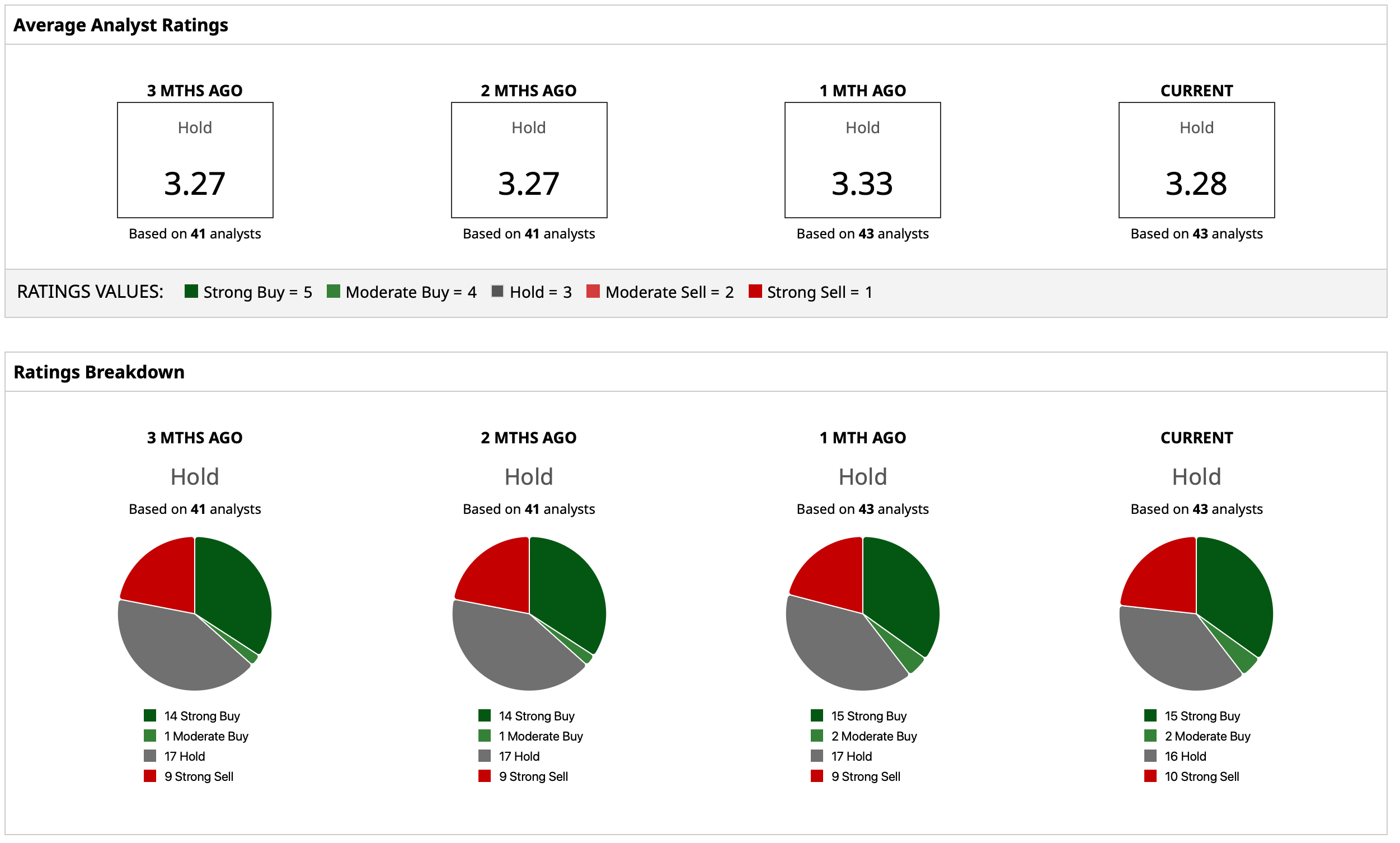

Overall, analysts have deemed TSLA stock to be a “Hold,” with a mean target price of $405.36. This denotes an upside potential of about 17% from current levels. Out of 43 analysts covering the stock, 15 have a “Strong Buy” rating, two have a “Moderate Buy” rating, 16 have a “Hold” rating, and 10 have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)