/Moderna%20Inc%20HQ-by%20hapabapa%20via%20iStock.jpg)

Hedge funds are betting hard against Moderna (MRNA). But the company's pipeline tells a very different story, and contrarian investors are paying close attention.

According to Bank of America's equity team, MRNA stock has the highest short interest of any S&P 500 ($SPX) stock, with 17.8% of its float sold short by hedge funds. That's a massive vote of no confidence from Wall Street's biggest players.

So what do they know that bulls don't? And more importantly, could they be wrong?

Why Moderna's Stock Is Heavily Shorted

The short thesis is not difficult to understand.

- Covid-19 vaccination rates have been declining.

- Moderna's U.S. revenue fell last year, dropping to $1.2 billion.

- And the company is still burning cash on a sprawling pipeline of drugs that haven't hit the market yet.

Moderna Chief Financial Officer Jamey Mock acknowledged as much at the TD Cowen 46th Annual Health Care Conference in March. The company is planning another decline in U.S. revenue in 2026, to roughly $1 billion, a 20% year-over-year (YoY) decline. That's a brutal number for a stock that once traded above $400.

But here's the thing that short sellers may be overlooking: Moderna isn't just a Covid vaccine company anymore.

Moderna’s Revenue Growth Plan Goes Well Beyond Covid

Despite the U.S. weakness, Moderna guided for up to 10% total revenue growth in 2026. The key driver isn't domestic vaccine sales but international contracts.

The company has locked in multi-year strategic partnerships with the United Kingdom, Canada, and Australia. In 2025, Moderna generated $700 million in international revenue. In 2026, management expects that number to climb to $1 billion.

"The step-up in revenue from our guidance last year ... the key step-up in our up to 10% growth is predominantly coming from ex-U.S. revenues," Moderna Head of Investor Relations Lavina Talukdar said at the Barclays 28th Annual Global Healthcare Conference in March. Moderna has signed multi-year contracts with governments, providing a level of revenue visibility that most biotech companies don't have.

Europe is also set to open up in 2027. A competitor's contract that effectively locked Moderna out of that $1.8 billion respiratory vaccine market expires later this year. And Moderna just received a positive Committee for Medicinal Products for Human Use (CHMP) opinion for its flu/Covid combination vaccine in Europe, meaning it could arrive ready to compete the moment that door opens.

Could the MRNA Stock Short Trade Flip?

The biggest potential game-changer is intismeran, Moderna's personalized cancer vaccine developed in partnership with Merck (MRK). The Phase III trial in adjuvant melanoma, one of the fastest-enrolling Phase III oncology trials ever, could read out in 2026.

Phase II data was remarkable. At the three-year mark, patients on intismeran plus Keytruda saw a hazard ratio of 0.51 on recurrence-free survival. That durability held for five years. If Phase III shows even a 0.75-0.80 hazard ratio, analysts say it would still be a clinically meaningful result with blockbuster commercial potential.

Moderna has eight late-stage cancer studies running across melanoma, renal cell carcinoma, bladder cancer, and lung cancer. Phase III trials in non-small cell lung cancer are still enrolling.

Beyond oncology, a Phase III readout for a norovirus vaccine is also expected in 2026. And Moderna's standalone flu vaccine now has a U.S. PDUFA date of Aug. 5, the first potential approval of what the company sees as a multi-billion-dollar product.

Talukdar described Moderna's 2025 as "a year of execution":

- $1.9 billion in revenue at the high end of guidance

- $1 billion in cost reductions exceeding targets

- And a cash balance of $8.1 billion.

The bottom line: short sellers are betting on further Covid decay. But they may not have fully priced in the company's international revenue floor, its approaching oncology catalyst, or a flu franchise that could generate real revenue starting in 2027.

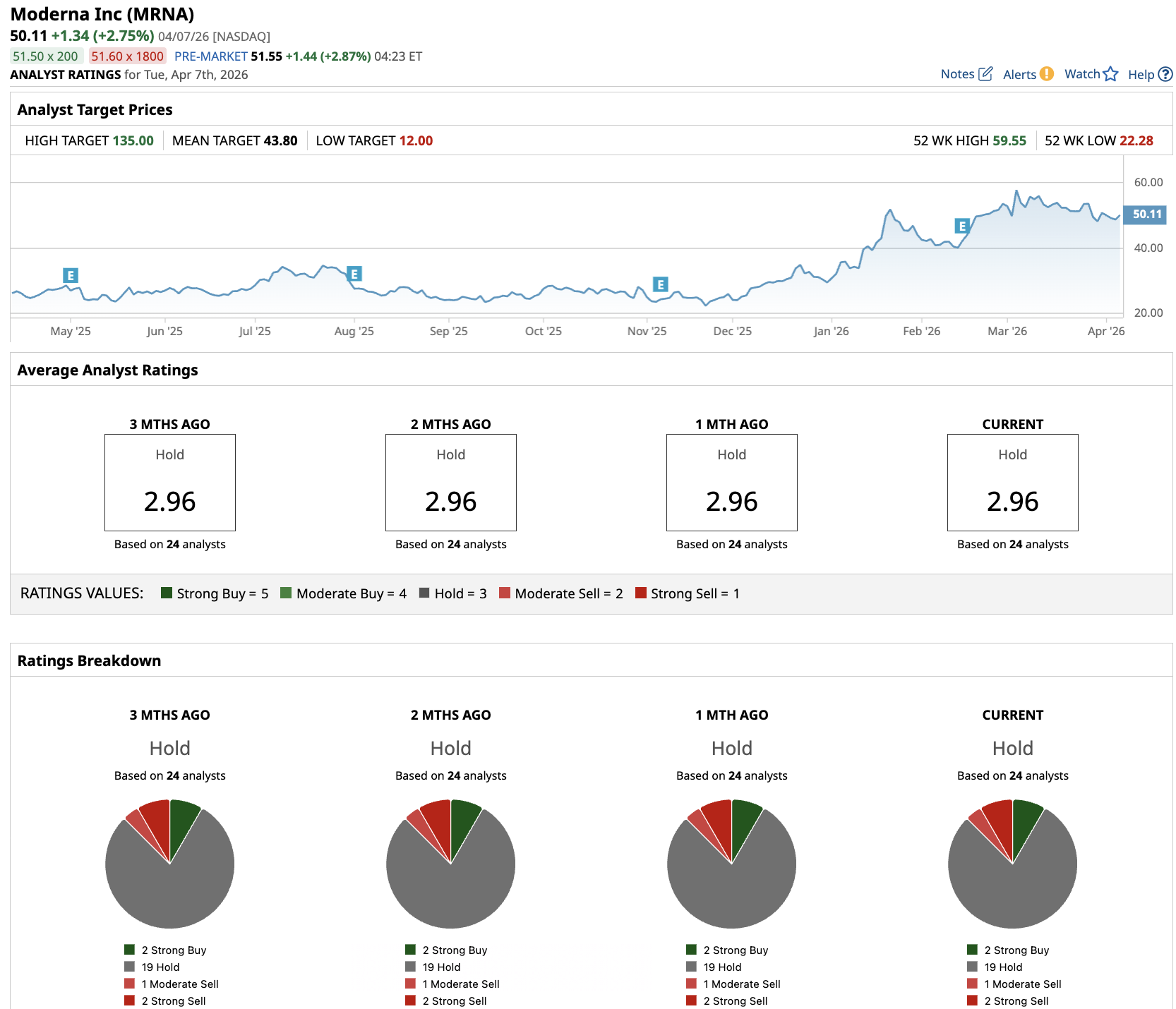

Out of the 24 analysts covering MRNA stock, two recommend “Strong Buy,” 19 recommend “Hold,” one recommends “Moderate Sell,” and two recommend “Strong Sell.” The average MRNA stock price target is $43.80, below the current price of about $50.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)