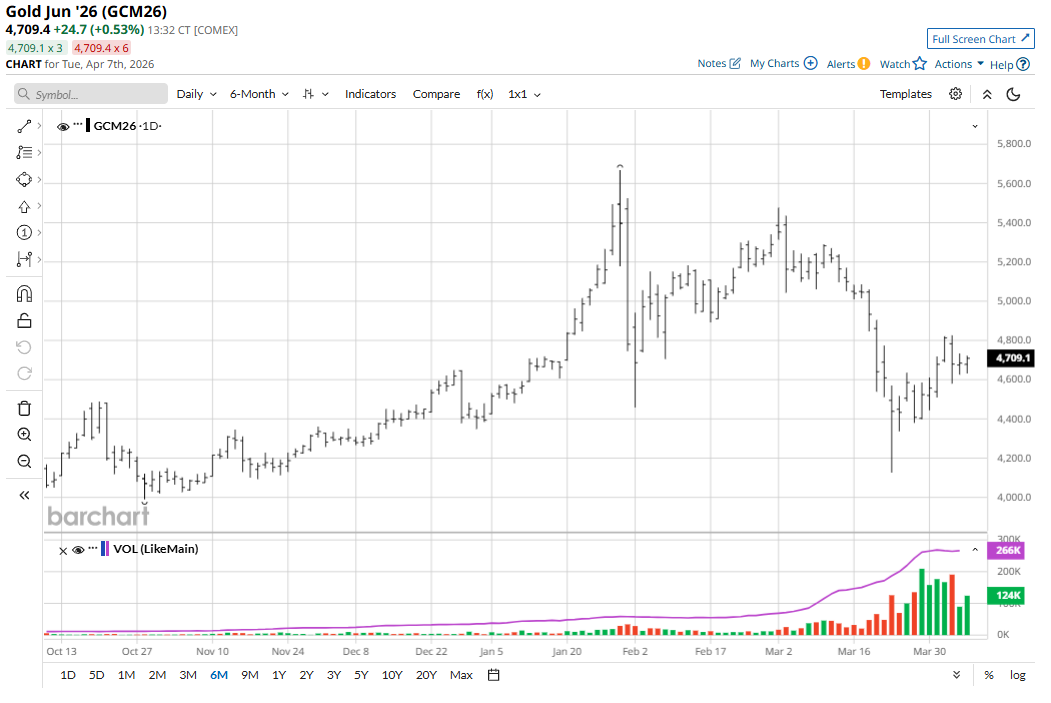

More than a few gold (GCM26) and silver (SIK26) market traders and investors, including the veterans, have been scratching their heads at recent daily price movements in the precious metals.

Recently, on trading days when risk appetite in the general marketplace is more robust and the stock indexes are rallying, so, too, are gold and silver prices. And on trading days when keener risk aversion in the marketplace has driven stock index prices solidly lower, safe-haven gold and silver prices have also sold off. This seeming dislocation of what heretofore had been one of the major supply and demand fundamentals (risk-on = bearish and risk-off = bullish) has frustrated gold and silver bulls.

Apparently, what gold and silver traders are presently deeming more important than the bullish aspect of safe-haven demand is the bearish aspect of slowing global economic growth due to the Middle East war. The conflict is choking off consumer and commercial demand for the metals in the coming months, or longer.

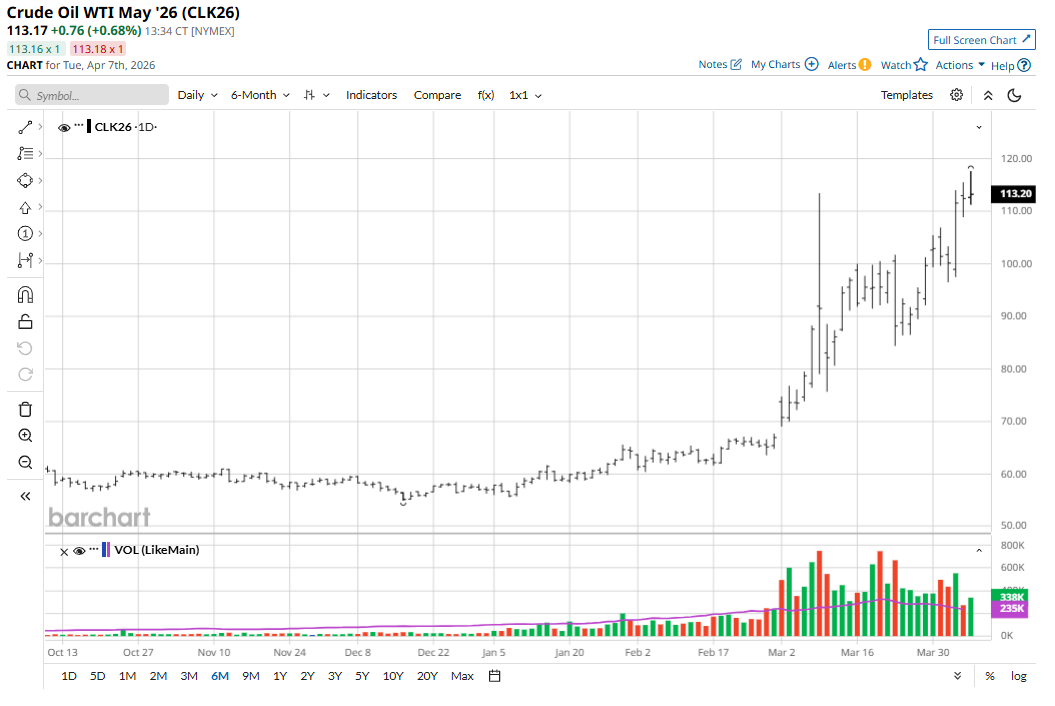

Spiking crude oil prices (CLK26) amid any slowing global economic growth could also prompt problematic inflation that could produce the dreaded stagflation phenomenon that is the archenemy of most markets, including raw commodities. Longtime gold and silver traders and investors remember the days when their metals were sought out as an inflation hedge. Many very likely correctly argue that down the road, such will be proven to still be the case.

The U.S. Dollar is Still a Major Factor for Gold and Silver

The U.S. dollar index ($DXY) (a basket of six major world currencies weighted against the greenback) is presently hovering near a 10-month high and remains in a near-term price uptrend. This is a daily bearish outside-market factor that has been crimping the upside of gold and silver. In times of keener geopolitical uncertainty, the dollar is also considered a safe-haven asset as traders around the globe, including sovereign nations, seek out the dollar to buy U.S. Treasuries that many believe are the safest asset in the world.

The Crude Oil Conundrum

The crude oil market is the leader of the raw commodity sector, and with its price hovering near a four-year high, such should be a firmly bullish fundamental for raw commodity markets, including gold and silver. Such was the case in the first couple weeks of the Middle East war.

However, as the war is now dragging on longer than many so-called experts initially reckoned, the reality is setting in that crude oil prices will remain elevated to the point of significantly cutting into global economic growth in the coming months. As one military expert said on TV today: “It’s much easier to close the Strait of Hormuz than it is to reopen it.”

Once again, it appears the raw commodity markets are paying more attention to the bearish aspect of higher crude oil prices acting to slow global economic growth.

My Bias on Gold and Silver Markets’ Price Direction

As I reported last week, gold and silver markets are in major, extended bull runs. Many veteran market watchers call that a tired trade. I think there is more price upside for gold and silver in the very near term and in the very long term. However, the coming days, weeks, or even few months are likely to see more choppy and sideways trading. Not a price uptrend and not a price downtrend, but a sideways trend. That’s not really surprising. Most of the time, most commodity markets’ prices are in choppy and sideways price trends.

For gold, in the coming months, I look for prices to trade between the record high scored in January, at $5,586.20 an ounce, basis nearby Comex futures, and the March low of $4,100.00. I look for silver prices to trade between $50.00 and 95.00. I know those are very big trading ranges, but hey, the general marketplace is presently experiencing what is arguably the biggest geopolitical event of the past 50 years. That means there are likely to be exaggerated price movements in many markets as the geopolitical event continues to play out.

Tell me what you think. I enjoy hearing from my valued Barchart readers from all around the globe. Email me at jim@jimwyckoff.com.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)