/A%20concept%20image%20of%20space_%20Image%20by%20Canities%20via%20Shutterstock_.jpg)

For the first time since the Apollo 17 mission in December 1972, humans are once again pushing beyond Earth’s orbit. The Artemis II mission has reignited that ambition, sending four astronauts on a historic journey around the moon and setting the stage for a permanent human presence in the years ahead. Backed by NASA, this mission is not just a one-time event - it is building the base for a future lunar economy.

But beyond the headlines and rocket launches, a lesser-known player is quietly positioning itself at the center of this shift. Intuitive Machines (LUNR) may not be a household name, yet its role is critical. The company is helping track and support the Orion spacecraft during Artemis II, while also building lunar landers and communication systems designed for future missions.

As NASA ramps up its lunar plans, demand for such infrastructure is expected to rise. That puts Intuitive Machines in a strong spot to secure long-term contracts and recurring revenue streams. While the company is still operating at a loss, its growing backlog and expanding role in Artemis missions are building confidence.

LUNR stock has already shown solid momentum, and analysts believe the path to profitability is becoming clearer, making LUNR a name investors may want to watch closely.

About Intuitive Machines Stock

Intuitive Machines is a Houston-based aerospace company with a market cap of $4.4 billion that designs and operates lunar landers, satellites, and deep-space communication systems. Intuitive Machines develops spacecraft, links them through advanced networks, and then runs those systems as a service for commercial clients, governments, and national security programs.

Over time, it has built more than 300 spacecraft and delivered over 260 kilograms of payload to the moon, while also guiding missions across the solar system with its navigation expertise. Importantly, its integrated model stands out, offering end-to-end solutions under one roof. As demand for lunar missions and space-based services grows, Intuitive Machines is positioning itself to be a key player in shaping the next era of space exploration.

Shares of Intuitive Machines have been on a strong run, but not without a few pauses along the way. Over the past two years, shares have surged 267.7%, with a solid 181% gain in just the past one year, showing rapid investor interest.

The stock hit a 52-week high of $23.32 in late January, and while it has pulled back about 2.6% from that level, the broader trend still looks healthy. In fact, over the last six months, LUNR is up nearly 108%, and it has already gained 43.87% in 2026. Even in the past month alone, the stock has climbed 29.79%, reflecting steady buying momentum.

The recent rally in LUNR stock is being driven by a clear shift in its growth story. Investors are increasingly betting on the company’s role in NASA’s plan to carry out multiple lunar missions, which could translate into steady demand for its landing and space delivery services.

At the same time, the company’s order backlog has jumped to around $943 million, giving better visibility into future revenue. And in January, its acquisition of Lanteris Space Systems strengthened capabilities, supporting upbeat 2026 guidance. Altogether, this combination of strong contracts, expanding opportunities, and improving outlook is giving the market more confidence, which is reflected in the stock’s steady climb.

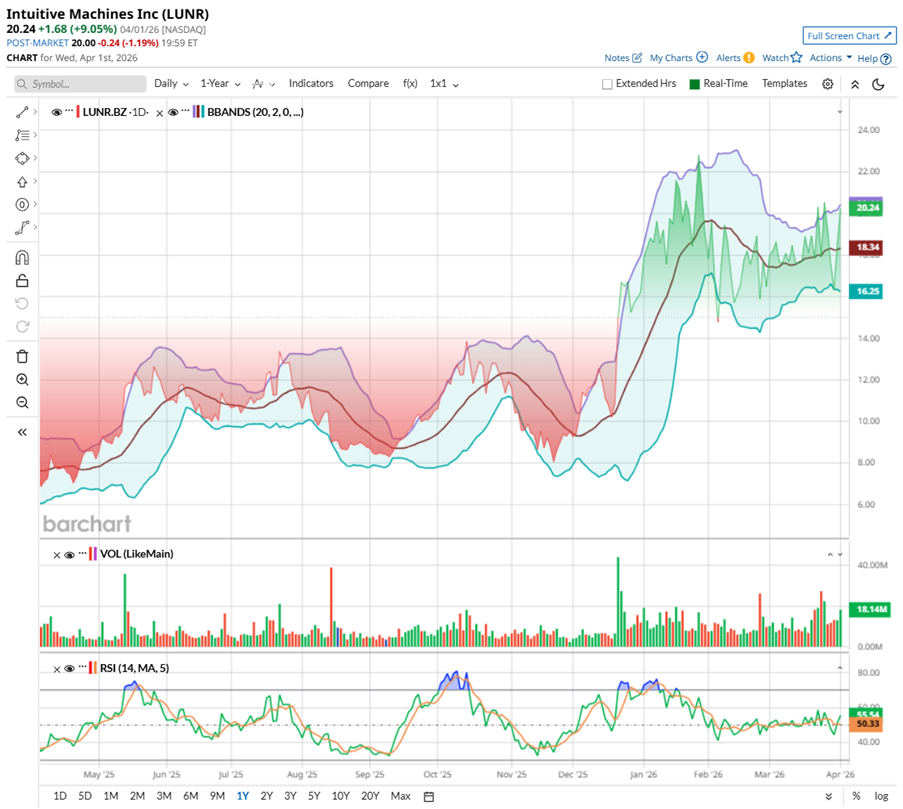

Technically, trading volumes with more green bars hint at stronger participation from buyers. The 14-day RSI of 61.8 shows bullish momentum but not overheated.

Looking at the Bollinger Bands in the chart, LUNR recently pushed toward the upper band during its sharp rally, signaling strong upside momentum. After that move, the price cooled off a bit and drifted toward the middle band, which often acts as a short-term support zone. Now, with the bands widening, it suggests higher volatility, while the price holding in the upper half of the range points to underlying strength.

Valuation-wise, LUNR looks expensive. The stock is priced at about 3.42 times forward sales, above the sector average. But that also reflects the market’s confidence in its role in the fast-growing space economy. Investors seem willing to invest in a company positioned at the forefront of lunar missions and next-gen space infrastructure.

A Closer Look at Intuitive Machines’ Q4 Report

Intuitive Machines wrapped up 2025 with a mix of ambition, expansion, and growing pains – exactly what one would expect from a company trying to scale in the space economy. On March 19, it rolled out its fiscal Q4 and fiscal 2025 results, highlighting a year in which it not only completed its second lunar mission but also deepened its involvement in national security programs. Add to that the acquisition of KinetX Aerospace and the announcement of Lanteris Space Systems acquisition, and this company is clearly trying to level up fast.

Q4 revenue came in at $44.8 million, largely driven by contracts like Commercial Lunar Payload Services (CLPS), Omnibus Multidiscipline Engineering Services III (OMES III), and Near Space Network Services. But that was below Wall Street's expectations.

Margins are slowly improving too, with gross margin at 19%, showing that the business mix is shifting in the right direction. But growth came at a cost – operating loss more than doubled to $33.1 million, mainly due to acquisition-related expenses, while net loss widened to -$59.7 million. Adjusted EBITDA stood at -$19 million, reflecting the pressure from ongoing investments and expansion efforts.

Cash flow tells a slightly better story. Free cash flow usage improved to $56 million for the year, and the company ended 2025 with cash and cash equivalents of $582.6 million, up sharply from the previous year. Long-term debt stood at $335.3 million, reflecting the cost of expansion.

Intuitive Machines took a big step forward on Jan. 13, closing its $800 million acquisition of Lanteris Space Systems, moving closer to becoming a fully integrated space contractor.

Now, on backlog, there was a dip of $115.3 million by the end of 2025, mainly because the company kept executing on existing contracts. Big chunks came from OMES III, CLPS missions, and NSN work, along with some mission-related adjustments. Nevertheless, fresh awards worth about $105 million helped soften the decline.

Then, this February, the combined backlog stood near $943 million, giving the company a solid base to support its 2026 growth plans.

Looking ahead, the focus shifts to execution. With Lanteris now in the fold, Intuitive Machines is positioning itself as a vertically integrated space contractor. For 2026, management expects revenue between $900 million and $1 billion, along with positive adjusted EBITDA, suggesting the company is aiming to turn scale into sustainability.

Analysts tracking Intuitive Machines anticipate things improving fast. Losses are expected to narrow sharply, down about 80% year-over-year (YOY) to -$0.08 in fiscal 2026. And looking ahead to 2027, the story could flip, with the company projected to turn profitable and deliver EPS of $0.16.

What Do Analysts Expect for Intuitive Machines Stock?

After landing a fresh NASA contract, Cantor Fitzgerald is maintaining its “Overweight” rating on LUNR. The brokerage firm sees the upcoming CT-4 mission as more than just another project – it could help fund the next, larger lunar lander.

Looking ahead, there’s a steady pipeline in sight, from the SiriusXM 11 delivery in early 2026 to potential wins like the CLPS CT-32 award and a key Lunar Terrain Vehicle decision by summer, keeping momentum alive.

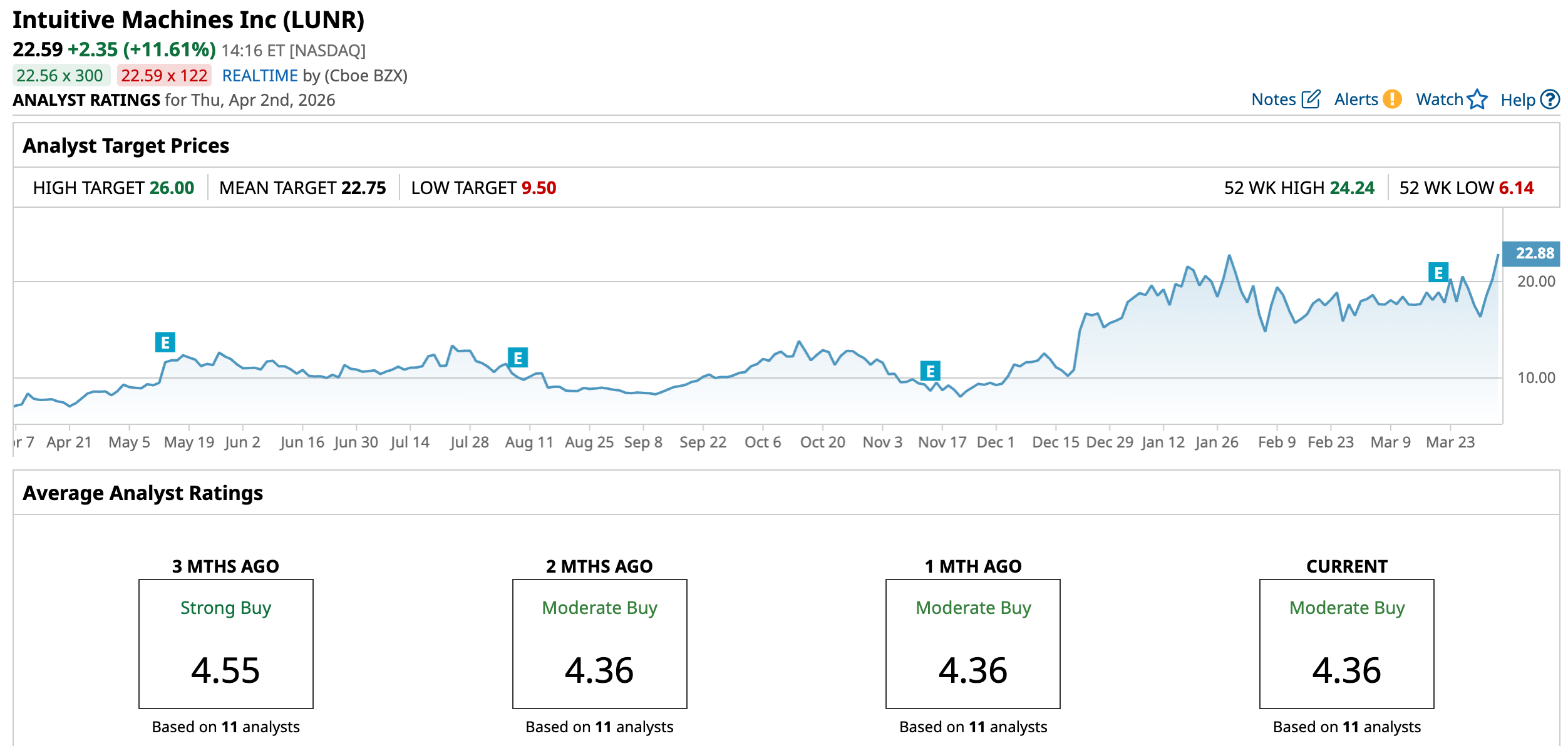

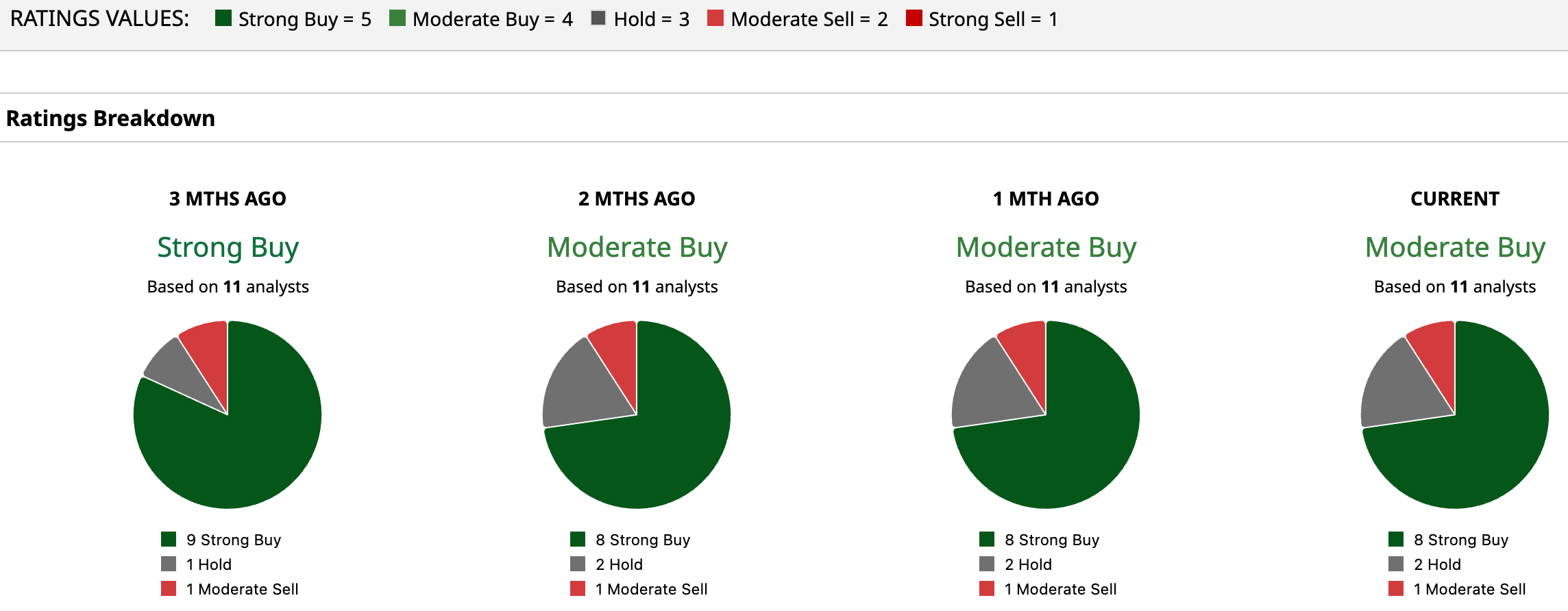

Analysts monitoring LUNR are optimistic, but with a dash of caution. The stock has a consensus rating of “Moderate Buy.” Out of 11 analysts, eight recommend a “Strong Buy,” two are on the sidelines, giving it a “Hold” rating, and one analyst advises a “Moderate Sell.”

Its current share price of $22.59 is hovering near the average price target of $22.75. Meanwhile, Cantor Fitzgerald’s Street-high target of $26 suggests LUNR stock could rise as much as 15.1% from the current price levels.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Hands%20of%20robot%20and%20human%20touching%20on%20big%20data%20network%20connection%20by%20PopTika%20via%20Shutterstock.jpg)

/CPU%20Chip.jpg)

/D_R_%20Horton%20Inc_%20billboard%20by-%20monticello%20via%20Shutterstock(1).jpg)