/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)

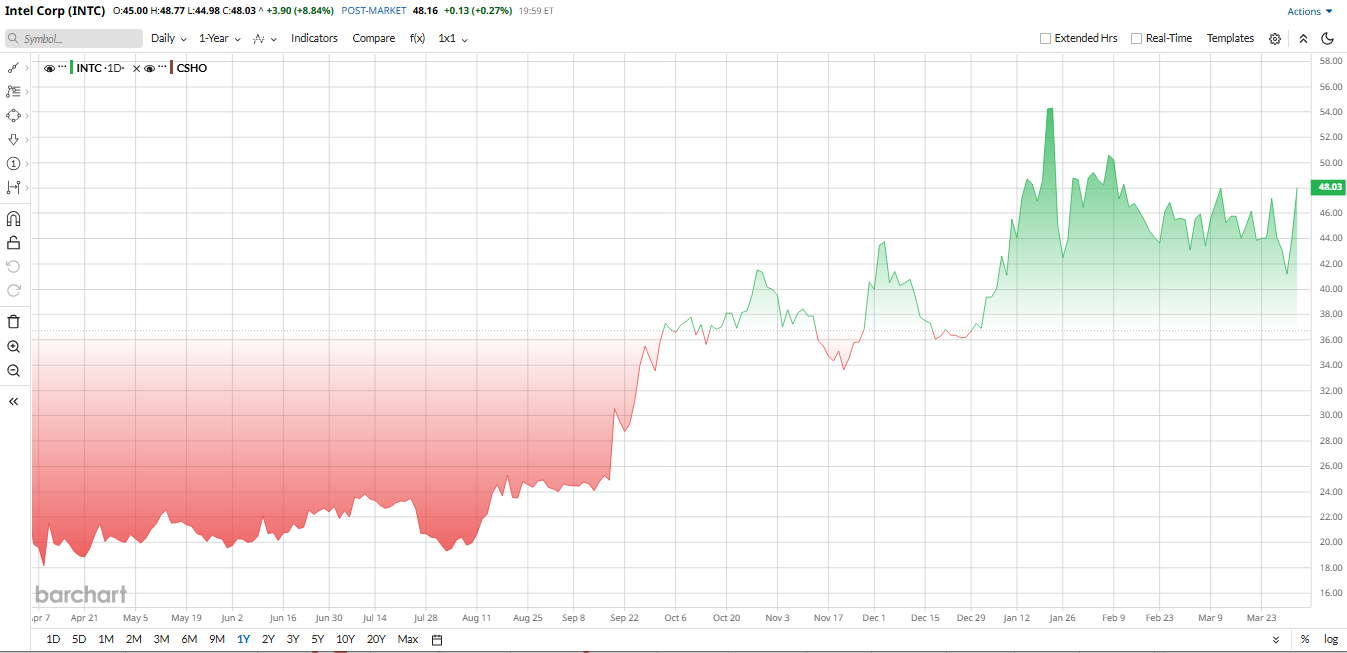

Semiconductor stocks have had a rocky start to 2026. AI chip darling Nvidia (NVDA) continues to soar, but old-school chipmakers like Intel (INTC) have been left behind. Investors are worried about PC demand, competition from AMD (AMD), and Intel’s costly factory buildout.

Intel is now trying to change that story with a major move tied to its manufacturing future. The company said it will buy back the 49% stake in its Fab 34 joint venture in Ireland from Apollo for $14.2 billion, a deal that gives Intel greater control over one of its most important production assets. Investors cheered on the news, sending INTC Shares more than 8% higher on Wednesday trading.

How Did Intel Stock Perform?

INTC stock has experienced a sharp rally lately. Over the past 12 months, the stock has more than doubled, and even amid broader market pressure, Intel has somehow managed to deliver 36% gains so far in 2026, thanks to its 8% jump yesterday on stake news.

From a technical perspective, the stock recently broke below its 200-day moving average, a development widely viewed as a bearish signal. At present, the shares are attempting to hold support near the $18 level.

However, on the valuation table, Intel looks like a bargain. It trades at just 1.2 times book value versus the semiconductor sector median of 4.5. Its forward P/E of 22 is below the industry average of 28. But it can get cheaper. Value traps exist for a reason. Investors want proof of a real recovery first.

Intel: Reclaiming Fab 34

The deal is more than a simple asset purchase. In 2024, Apollo paid $11.2 billion for the minority stake, providing Intel with cash when the chipmaker was under pressure and expanding its manufacturing footprint. Intel now says the company has a stronger balance sheet, better financial discipline, and a more evolved strategy under CEO Lip-Bu Tan, who has pushed restructuring, job cuts, and asset sales since taking over.

Fab 34 is not just any plant. The Ireland site makes chips using Intel 4 and Intel 3 technologies, including Core Ultra and Xeon processors, and was Intel’s first high-volume manufacturing site to use extreme ultraviolet lithography for Intel 4. Intel is also shifting focus toward its more advanced 18A technology, which management wants to use as a key part of the comeback story.

Intel Q3 Shows a Slow Turnaround

Intel’s latest reported quarter showed early signs of stabilization, but the recovery remains gradual. The company posted revenue of $13.7 billion, down about 4% year-over-year (YoY), reflecting ongoing pressure in parts of its core business.

On the bottom line, Intel delivered adjusted earnings per share of $0.15, which came in ahead of expectations. While profitability improved versus prior quarters, margins are still being weighed down by heavy investments in manufacturing and AI infrastructure.

The company’s outlook, however, highlighted that challenges remain. Intel guided first-quarter 2026 revenue to a range of $11.7 billion to $12.7 billion, with adjusted earnings expected to be roughly break-even. That softer guidance suggests demand visibility is still uneven in the near term.

Even so, management continues to focus on long-term execution. Intel is investing aggressively in its foundry strategy and advanced nodes like Intel 3 and 18A, aiming to rebuild its competitive position.

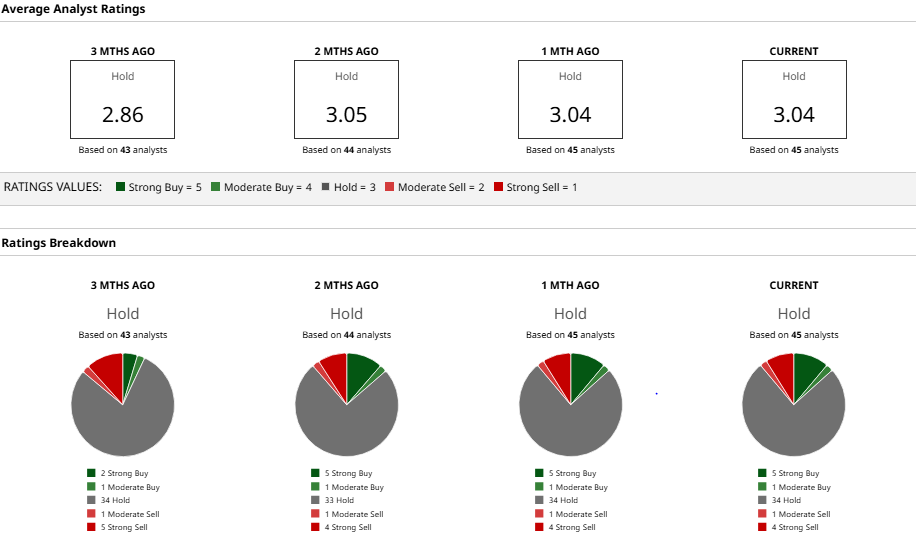

What Analysts Are Saying About INTC Stock?

Wall Street is split on Intel. Morgan Stanley lifted its price target to $39 from $35, maintaining an “Equal-Weight” rating. Analyst Joseph Moore pointed to PC segment growth but flagged “the data center malaise persists.”

Likewise, KeyBanc shifted to an “Overweight” rating with a $60 target, citing strong server CPU demand. Northland reiterated “Outperform” with a $54 target, following Intel’s Ireland fab repurchase.

On the bearish side, Goldman Sachs kept a “Sell” rating, raising its target to $30 from $28. Analyst Toshiya Hari acknowledged Intel’s technology roadmap execution but called the internal foundry model a “challenge.”

Importantly, Bank of America maintained an “Underperform” rating, cutting its target to $32 from $35. Analyst Vivek Arya noted that while the PC market is normalizing, a “faster pace of new products could keep costs elevated.”

Overall, according to Barchart, the consensus rating among 45 analysts is a “Hold.” The average 12-month price target is $45.26, which INTC stock already surpassed recently and is now moving towards its street high target of $66, which is about 34% above the current levels.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)