/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Micron (MU) shares bounced back on Wednesday as GF Securities issued a bullish note on the memory market, and signs of easing geopolitical tensions in the Middle East helped improve sentiment.

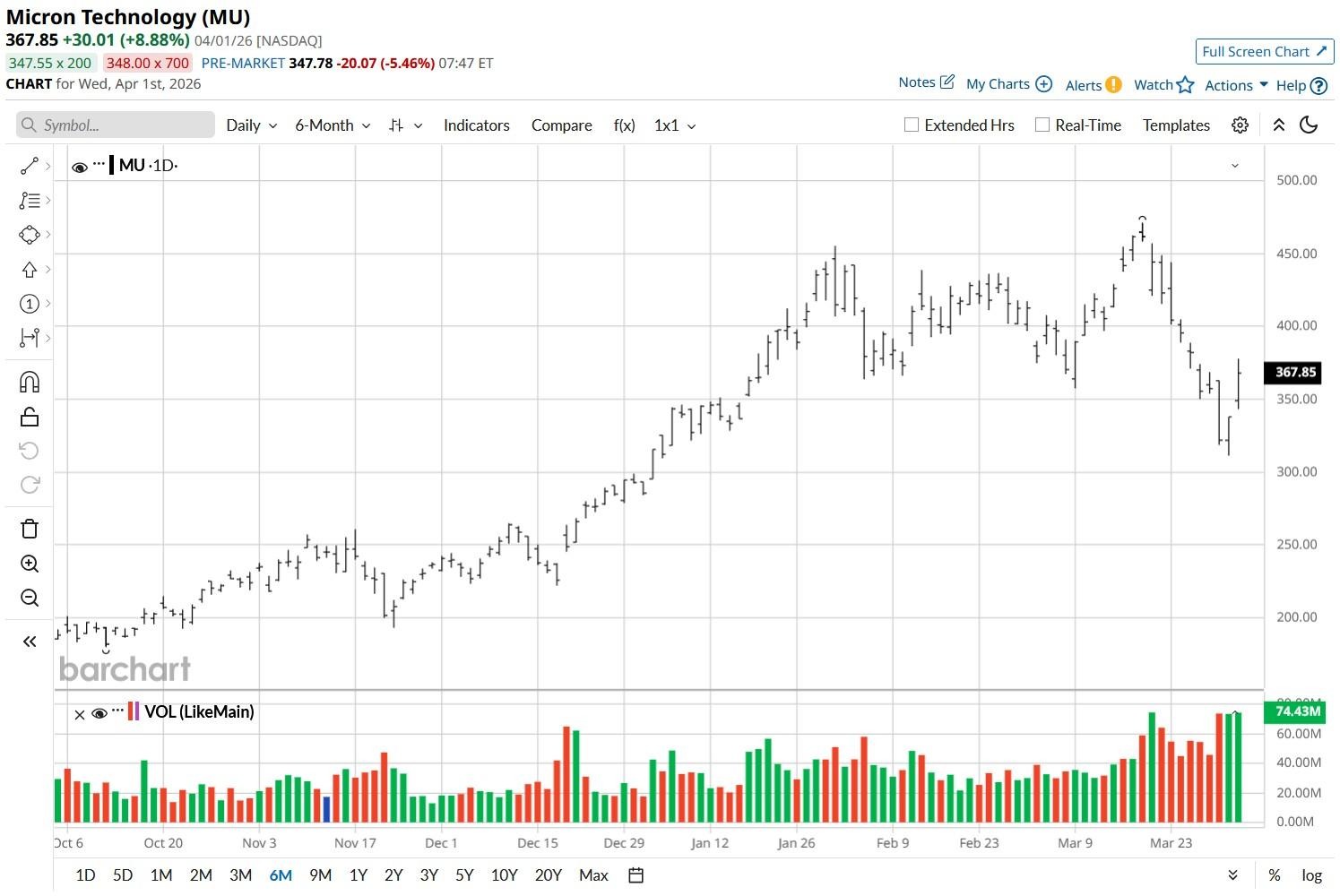

MU has successfully reclaimed its 100-day moving average (MA) and looks headed to test its 20-day MA next, indicating bulls are now taking back control across multiple timeframes.

Despite recent gains, however, Micron stock remains down more than 20% versus its year-to-date high.

Why GF Securities’ Note Is Bullish for Micron Stock

In his research note, GF Securities’ senior analyst Jeff Pu dubbed the recent pullback in memory spot prices a “healthy correction” rather than a structural downturn.

According to Pu, the decline was driven primarily by a high price premium and liquidation of speculative positions.

For example, “64GB DDR5 in Huaqiangbei were traded around $2500 — nearly double the contract price of $1250-1500 offered by Micron/Samsung in 2Q26,” making a correction inevitable.

However, Pu expects spot prices to stabilize quickly as long-term contracts are signed.

With 2027 DRAM pricing projected to be at least 25% higher than current levels, MU shares are poised for sustainable earnings visibility and margin expansion moving forward.

HBM Shift to Drive MU Shares Higher

Beyond pricing cycles, the bull case for Micron shares is rooted in the massive shift toward High-Bandwidth Memory (HBM).

As Nvidia (NVDA) transitions to its Rubin Ultra line — featuring 1 TB of HBM — artificial intelligence (AI) server demand will account for 90% of the total DRAM demand by 2028, Pu noted.

This structural imbalance, where demand growth significantly outpaces a 15% annual supply boost, is broadly expected to keep the market tight.

All in all, given the aggressive shipment plans from hyperscalers like Alphabet's (GOOG) (GOOGL) Google, the sustainability of MU’s record profits appears increasingly durable.

How Wall Street Recommends Playing Micron

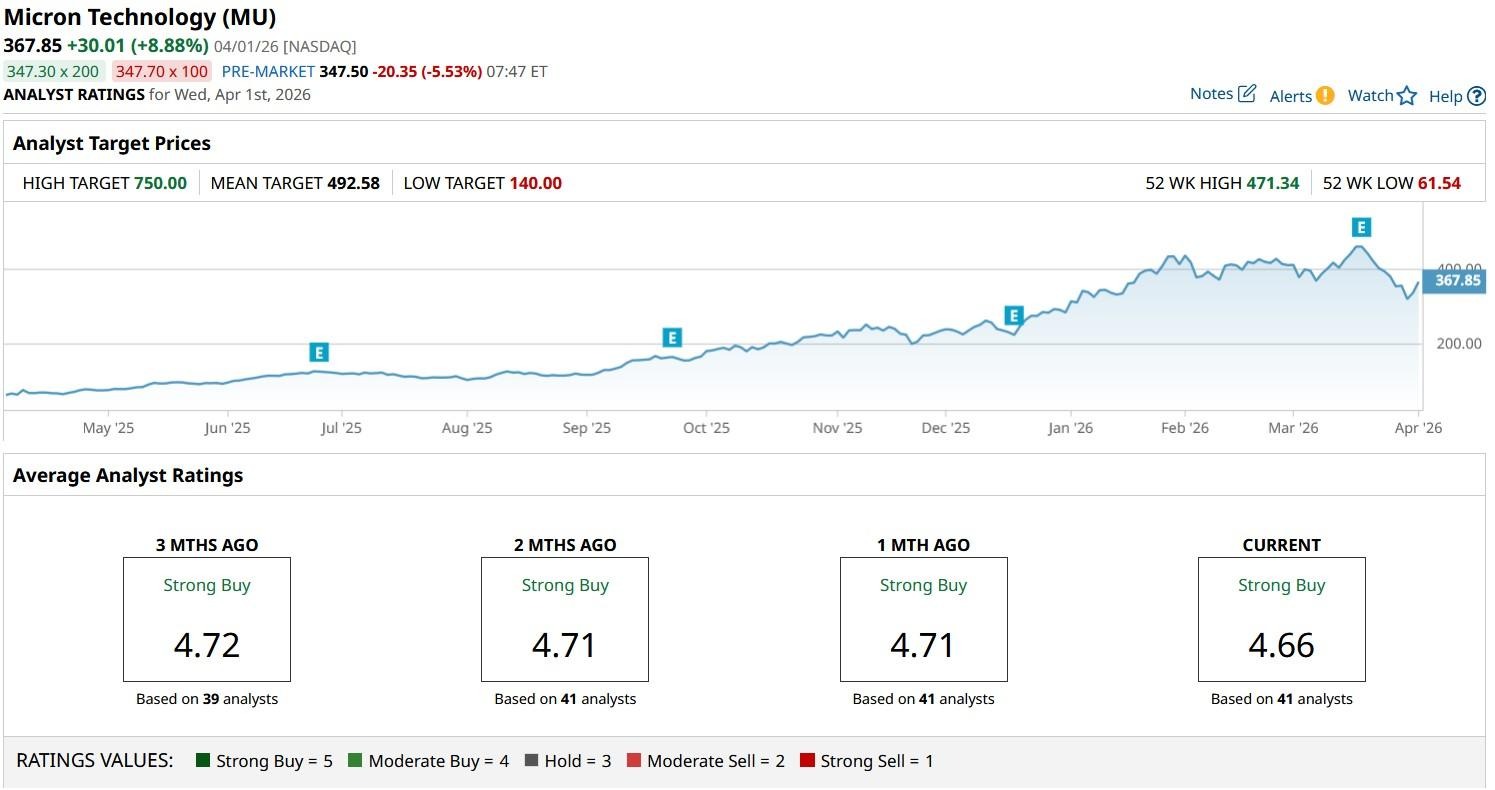

Wall Street continues to pound the table on Micron Technology, especially since it’s trading at an exceptionally cheap forward price-to-earnings (P/E) multiple of less than 6x currently.

The consensus rating on MU stock sits at “Strong Buy,” with the mean price target of roughly $492 indicating potential upside of about 35% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)