/Monolithic%20Power%20System%20Inc%20logo%20magnified-by%20Casimiro%20PT%20via%20Shutterstock.jpg)

Monolithic Power Systems (MPWR) is making its case as a high-conviction semiconductor play, with Oppenheimer Holdings (OPY), the Investment research and advisory firm, placing it in the same league as NVIDIA Corporation (NVDA), Broadcom (AVGO), and Marvell Technology (MRVL).

Following recent channel checks across Asia’s supply chain, Oppenheimer’s analyst Rick Schafer highlighted that the artificial intelligence (AI) race remains in overdrive. Cloud service providers are aggressively scaling infrastructure, with demand expected to outstrip supply well into 2027.

The imbalance is particularly visible in advanced wafers, packaging, and memory, where tight supply and extended lead times are pushing prices higher. The backdrop is working in Monolithic Power’s favor as its focus on power management solutions gives it a critical role in AI data centers, where efficiency and precision directly impact performance.

Still, the story requires patience as long design cycles and the complexity of data center integration mean that many of these opportunities will likely convert into meaningful revenue closer to 2028.

However, the lag does not weaken the thesis. If anything, it highlights that Monolithic Power’s current positioning could prove so valuable as the next phase of AI-driven demand begins to take shape.

About Monolithic Power Stock

Based in West Palm Beach, Florida, Monolithic Power Systems designs high-performance power semiconductors that regulate voltage and current across a wide range of advanced electronics. With a market cap of $53.7 billion, its product portfolio spans DC-DC converters, AC-DC solutions, MOSFET drivers, and power management ICs, all distributed through a global network of channel partners.

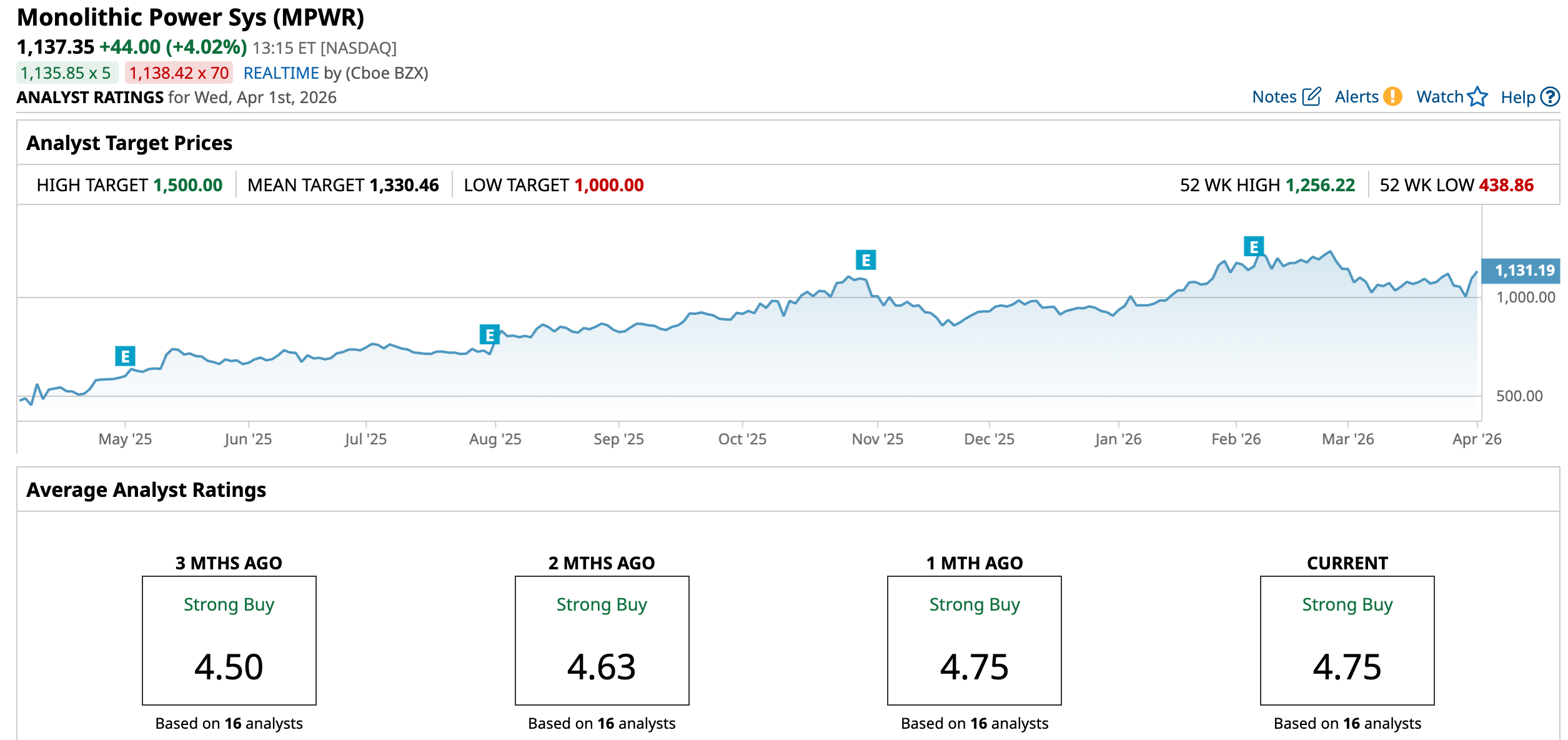

MPWR stock has climbed 94.4% over the past 52 weeks and gained another 23.4% in the last six months. Even on a year-to-date (YTD) basis, it is up 24.7%, showing that momentum has carried into 2026.

From a valuation standpoint, the stock is currently trading at 58.95 times forward adjusted earnings and 15.85 times sales. While the figures sit above industry averages, they remain below and above their own five-year average multiples, respectively, which suggests the premium is not as stretched as it may first appear.

On the income front, Monolithic Power has raised its dividend for eight consecutive years and now pays $8 per share annually, offering a yield of 0.80%. The next payout of $2 per share is scheduled to be paid on April 15 to shareholders on record as of March 31.

Monolithic Power Surpasses Q4 Earnings

On Feb. 5, Monolithic Power reported its Q4 fiscal 2025 results, owing to which the stock rose 1.7% on the day and added another 6.4% in the following session. Revenue climbed 20.8% year-over-year (YOY) to $751.2 million, comfortably ahead of the $742.4 million analyst estimate. Adjusted EPS rose 17.1% from the year-ago value to $4.79, also beating the Street’s forecast of $4.74,

Non-enterprise data end markets expanded by more than 40% YOY, highlighting the strength of a diversified business model. At the same time, the company secured over $4 billion in geographically balanced capacity and continued to add supply chain partners.

In addition, Monolithic Power delivered record module revenue and moved further toward integrated solutions by sampling its 800-volt power solution for data centers. In automotive, it introduced solutions for 48-volt and zonal architectures, including the first fully integrated 48-volt EPUs at the kilowatt-level zonal controller.

Non-GAAP operating income rose 21.9% YOY to $269 million, while non-GAAP net income climbed 18.6% to $235.4 million. Also, the balance sheet strengthened meaningfully, with cash and cash equivalents rising to $1.1 billion as of Dec. 31, 2025, up from $691.8 million a year earlier.

Looking ahead, management struck an optimistic tone. It pointed to improving visibility into customer demand and a growing backlog, particularly in data center power solutions tied to AI and server applications. For Q1 fiscal 2026, the company expects revenue between $770 million and $790 million, along with a non-GAAP gross margin in the range of 55.2% to 55.8%.

Analysts see the momentum carrying forward. They expect Q1 fiscal 2026 EPS to jump 30.5% YOY to $3.81. For the full fiscal year 2026, earnings are projected to rise 32.9% to $17, followed by another 21.5% increase to $20.65 in fiscal year 2027.

What Do Analysts Expect for Monolithic Power Stock?

Wall Street continues to lean firmly in Monolithic Power’s favor. Wells Fargo’s Joe Quatrochi maintained an “Overweight” rating while lifting the price target from $1,200 to $1,350. Citigroup’s Kelsey Chia followed a similar path, reiterating a “Buy” rating and raising the price target from $1,250 to $1,350.

The bullish tone extended further when Truist Securities’ William Stein raised his target to $1,396 from $1,375 and maintained a “Buy” rating, while KeyBanc’s John Vinh kept his “Overweight” rating and pushed his target up to $1,500 from $1300.

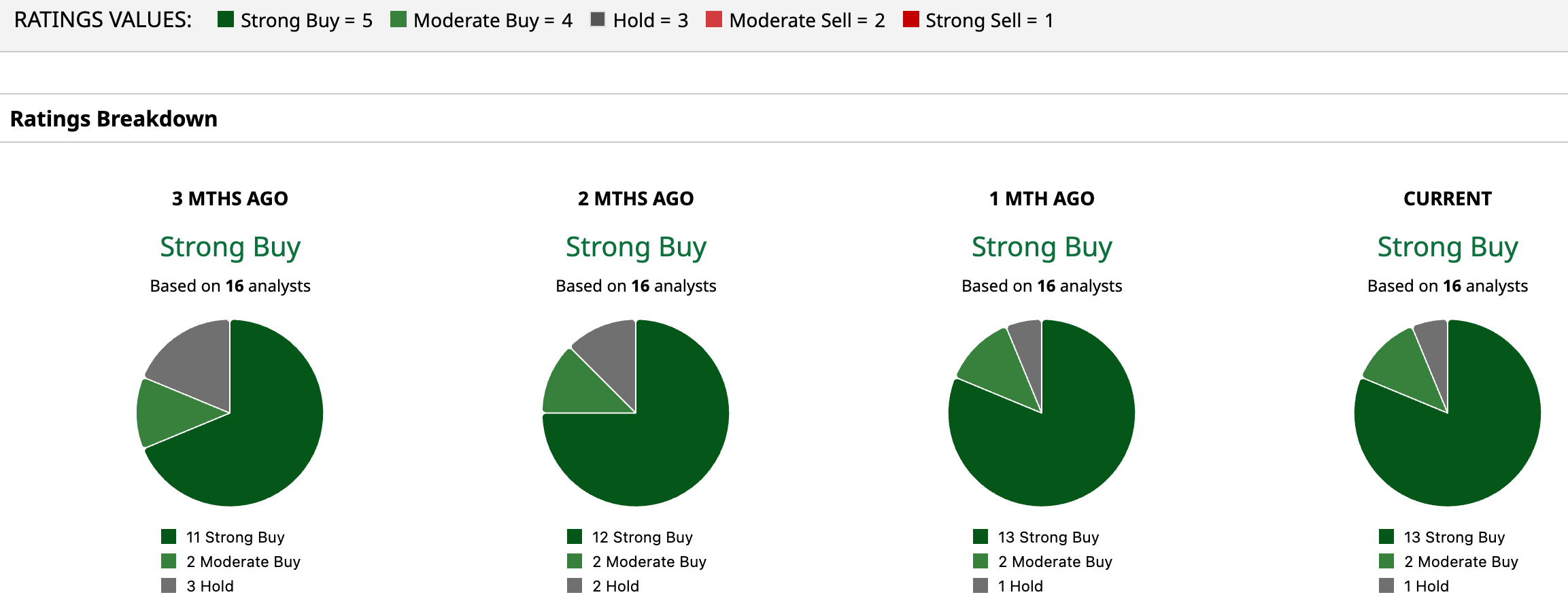

The broader analyst community echoes the optimism. Among 16 analysts covering MPWR stock, the overall rating sits at “Strong Buy,” with 13 calling it a “Strong Buy,” two assigning a “Moderate Buy,” and one opting to “Hold.”

The conviction carries through to price targets. The mean price target of $1,330.46 signals potential upside of 17%. Meanwhile, the Street-high target of $1,500 from KeyBanc’s John Vinh suggests a gain of 32% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)