Over the past few years, artificial intelligence has turned data center stocks into some of the market’s biggest winners. The race to build more computing power has only gotten bigger, and Nvidia (NVDA) has been at the center of it all, thanks to its dominant position in AI chips. The company recently projected that its Blackwell and Rubin GPU platforms could generate as much as $1 trillion in data center revenue, which shows the enormous demand coming from hyperscale cloud providers and enterprise customers.

Now, one major Wall Street firm thinks Nvidia’s growth story may still be flying under the radar. In a new note, Wells Fargo said Nvidia’s $1 trillion data center revenue forecast could actually turn out to be conservative, with the firm seeing even more upside ahead for 2026 and 2027.

For investors watching the AI boom, here is why Wells Fargo is so bullish on Nvidia’s data center revenue.

Nvidia Is Now Cheaper Than the S&P 500

Nvidia’s stock cooled off after a blistering 2025. The shares were up 40% in 2025 but have slid roughly 10% year-to-date (YTD) in 2026. The pullback strings tie with the broader tech selloff due to the ongoing war and profit-taking after last year’s gains. Still, Nvidia is outperforming many peers, and the pullback has only made the valuation more attractive for growth investors.

This has happened after 17 years, and Nvidia is now trading at a discount from the S&P 500 ($SPX). After the sharp selloff last week, Nvidia's forward earnings currently stand at 19.8x, below that of the S&P 500, which trades at 20.4x. So I think Nvidia fans can't get a better offer than what the chipmaker is giving right now.

Wells Fargo’s Turn Bullish

On March 27, Wells Fargo released a note with a big claim: Nvidia’s goal of $1 trillion in data center GPU revenue through 2027 may be “conservative by a lot.” The research team says they see 15% to 20% upside to the consensus 2026-27 estimates.

In other words, instead of $1 trillion, it could be $1.15 trillion to $1.2 trillion. This surprising endorsement of Nvidia’s runway got headlines. The message to investors is clear: even Nvidia’s own targets might be low. And if Nvidia really can capture $1.2 to 1.5 trillion, it underscores why the stock is a core AI play.

Record Growth in the Latest Quarter

Nvidia’s fiscal fourth-quarter results for the period ending January 25, 2026, exceeded expectations by a wide margin. The company reported revenue of $68.1 billion, a 73% increase compared to the same quarter a year earlier. The primary driver was Nvidia’s data center GPU business, which generated $62.3 billion in quarterly revenue, up 75% year-over-year (YoY).

Profitability surged alongside revenue. Fourth-quarter net income totaled $42.96 billion, a 94% increase from the prior year. Earnings per share (EPS) on a GAAP basis came in at $1.76, up 98%. Gross margins remained near 75%, underscoring Nvidia’s continued pricing power despite competitive pressures.

Nvidia ended the quarter with a sizable cash balance and significant capacity for shareholder returns; the company noted that $58.5 billion remained under its share repurchase authorization.

CEO Jensen Huang was bullish. He told investors, “Computing demand is growing exponentially, the AI inflection point has arrived.” Nvidia guided Q1 FY2027 sales to around $78 billion, an all-time high, showing continued momentum. And management gave no chill on capex. Huang said Nvidia will keep building factories for Blackwell GPUs to meet insatiable demand.

All in all, Q4 was a blowout, which underlines how fast Nvidia is scaling its data center business, highlighting that AI is not slowing down for Nvidia.

AI Deals and Expansion

Beyond earnings, Nvidia is also making big moves. At its March GPU Technology Conference (GTC), Nvidia announced a partnership to sell 1 million AI chips to AWS by 2027, deepening its cloud ties. It’s also ramping production of new Grace Blackwell CPUs and Vera Rubin GPUs. Jensen Huang reported a backlog of $500B in orders for 2026 and another $500B for 2027, a staggering pipeline that directly feeds the Wells Fargo thesis.

Additionally, the company even boosted its quarterly dividend and executed a stock split in 2023, signaling confidence that it will continue to generate massive cash going forward.

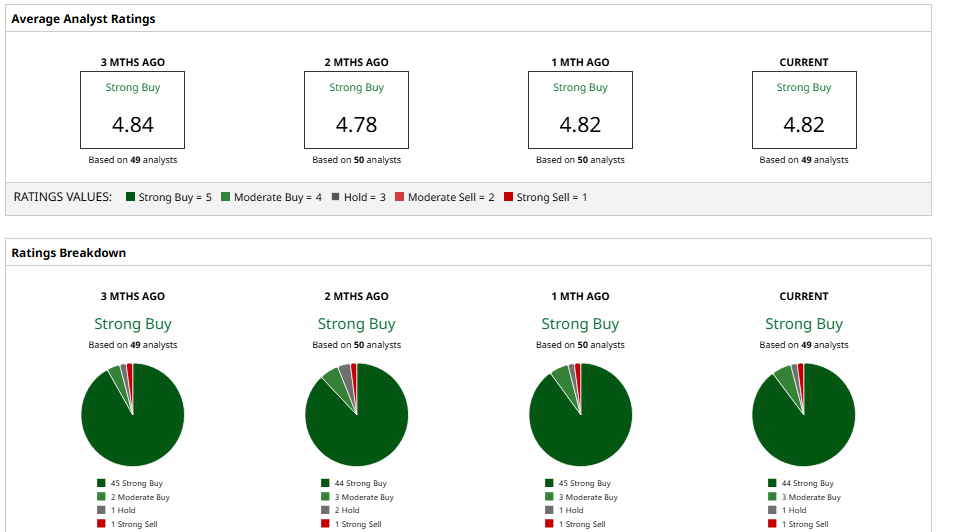

What Analysts Are Saying About Nvidia?

Wall Street remains overwhelmingly bullish on Nvidia. Most firms have "Buy" ratings and rich price targets. Goldman Sachs, for example, maintained a $250 target after GTC, arguing Nvidia’s AI edge still justifies that level.

Bank of America and Bernstein are even more optimistic, each at $300 targets, noting the company’s runaway growth. Morgan Stanley pegs its target at $260, acknowledging risks but valuing Nvidia’s AI moat.

Wedbush’s Dan Ives is famously bullish; he says Nvidia is “two to three years ahead of anyone, including Google,” and reiterated his “Outperform” rating. Rosenblatt Securities went as high as $325, banking on inference chips.

According to Barchart, the consensus price target is around $269.50, which gives the stock room to run 61% from current levels. Plus, the consensus rating is a solid “Strong Buy.” So I think Nvidia has an “unrivaled ecosystem,” and demand visibility is stronger than ever. And I see the $1 trillion forecast as a floor, not a ceiling, implying substantial upside if Nvidia delivers as expected. With growth forecasts still being revised higher, the Street’s median target might look conservative. As more analysts model in that extra 15-20% of data center revenue, we could see targets creep north of $300 again.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)