McDonald's Corp. (MCD) reported +3.8% higher Q1 comparable store sales on May 7, including +3.9% higher U.S. comp sales. However, the market is obsessed with the CEO's comments on how higher gas prices affect lower-income families, as an AP report commented.

Nevertheless, fears seem overdone with MCD stock below its prior 1-year low point (i.e., $285.55 on June 25, 2025). Its free cash flow is strong, and analysts are forecasting higher revenue. Could this be a good buying opportunity for value investors?

MCD closed at $275.75, down 2.80% on Friday, May 8, and is off 19.1% from a recent peak of $341.06 at the end of February (Feb. 27). Since last month-end, MCD is off $17.84, i.e., -6.07% from $293.59 on April 30.

Strong Sales and FCF

McDonald's Corp.'s Q1 total systemwide sales rose 6% in global constant currency, and total revenue was up 9.4% to $6.5 billion. Moreover, its operating income rose 11.5% for the quarter to $2.953 billion, resulting in a strong operating margin of 45.3%, slightly over 44.46% last year.

However, for the quarter, McDonald's generated slightly lower free cash flow: $1.73 billion, compared to $1.877 billion last year, according to Stock Analysis.

Not to worry, though, as over the trailing 12 months (TTM), McDonald's Corp. has still generated higher FCF: $7.039 billion vs. $6.704 billion last year. That worked out to a 25.65% FCF margin, slightly lower than the prior year (26.08% for the TTM period to Q1 2025), and 26.73% for the full-year 2025.

Overdone Fears?

The market is likely not reacting to this lower FCF and FCF margin performance. It seems more concerned about the CEO's comments about whether MCD's customers will drive to McDonald's stores with higher gas prices.

For example, the AP article pointed out that gas prices are now 44% higher than a year ago. The CFO, Ian Borden, said that gas prices will “disproportionally affect low-income consumers.” He said that they are already under pressure and that these “pressures there are gonna continue.”

However, the market may be too worried about affordability. After all, these issues are not new. McDonald's now has 10 items at $3.00 or lower as of April 21 on its McValue menu, according to AP, and its value menu offerings are expanding.

Moreover, analysts are still projecting higher sales for 2026 and 2027. That will lead to higher comp sales, despite higher gas prices, as well as free cash flow.

For example, Seeking Alpha reports that the average forecast of 32 analysts is $28.51 billion for 2026, compared to $26.866 billion in 2025 (i.e., a +6.1% gain). Moreover, for 2027, 33 analysts are forecasting $30.18 billion (i.e., up another +5.86% over 2026).

In other words, over the next 12 months (NTM) period, average revenue should be $29.345 billion, or 9.2% higher than in 2025.

Forecasting FCF and Price Targets

As a result, it's reasonable for analysts to project higher free cash flow (FCF). That could lead to a higher stock price over the NTM period.

For example, assuming McDonald's generates a 26% FCF margin (i.e., slightly over its LTM FCF margin - see above):

$29.345 billion NTM revenue x 0.26 FCF margin = $7.63 billion FCF

That's 8.4% higher than the $7.039 billion in FCF for the TTM period as of Q1. This could push MCD stock higher. Here's why.

Let's assume that MCD pays out 100% of its FCF to shareholders. That means that its FCF yield is about 3.60%, given its market cap today of $195.92 billion (according to Yahoo! Finance):

$7.039b TTM FCF / $195.92 billion mkt cap = 0.0359 = 3.6% FCF yield

So, applying this to our forecast of $7.53 billion:

$7.63b NTM FCF / 0.0359 = $212.53 billion market value

So, MCD's value for the next 12 months has a fair value that is 8.5% higher than its present $195.92 billion market value. So, MCD's price target is worth almost $300:

$275.75 x 1.085 = $299.19 price target (PT)

Other analysts agree. For example, Yahoo! Finance's survey of 36 analysts shows an average of $333.97 per share. And Barchart's mean analyst survey is even higher at $343.76. However, AnaChart's survey of 24 analysts shows an average PT of $320.28.

The bottom line is that MCD stock has an average fair value of $324.30 per share, or +17.6% higher than Friday's close.

One way to play this is to sell short out-of-the-money puts and buy in-the-money calls.

Shorting OTM Puts and Buying ITM Calls

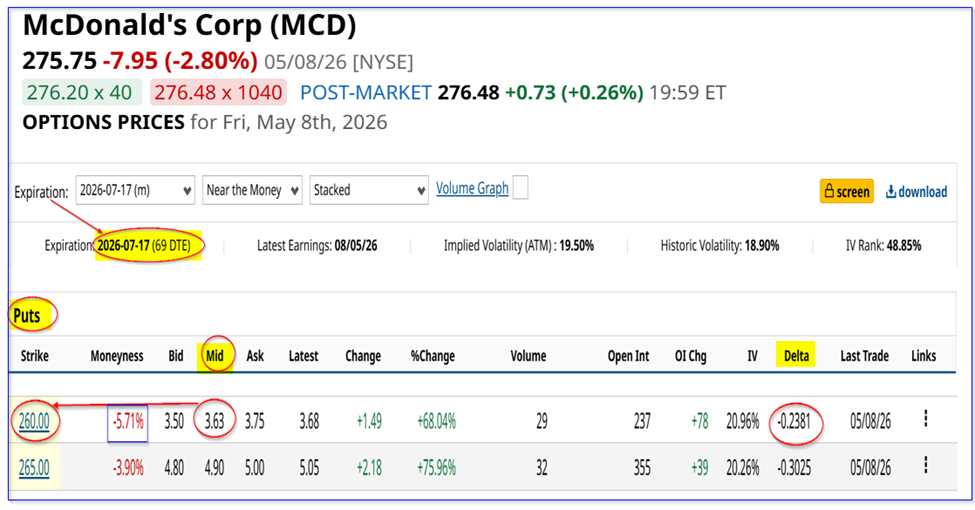

For example, the $260 strike price put option expiring July 17, which is 5.7% lower than Friday's close, has a midpoint premium of $3.63. That gives a short-seller an immediate yield of 1.40% (i.e., $3.63/$260).

Moreover, the delta ratio is just 0.238, implying less than a 24% chance that MCD will fall to $260 over the next 69 days. An investor must first secure $26,000 with the brokerage firm. Then, after entering an order to “Sell to Open” 1 put contract at $260, the account will receive $363.

Even if MCD falls to $260, the income received lowers the breakeven point to $256.37, or 7% below Friday's close.

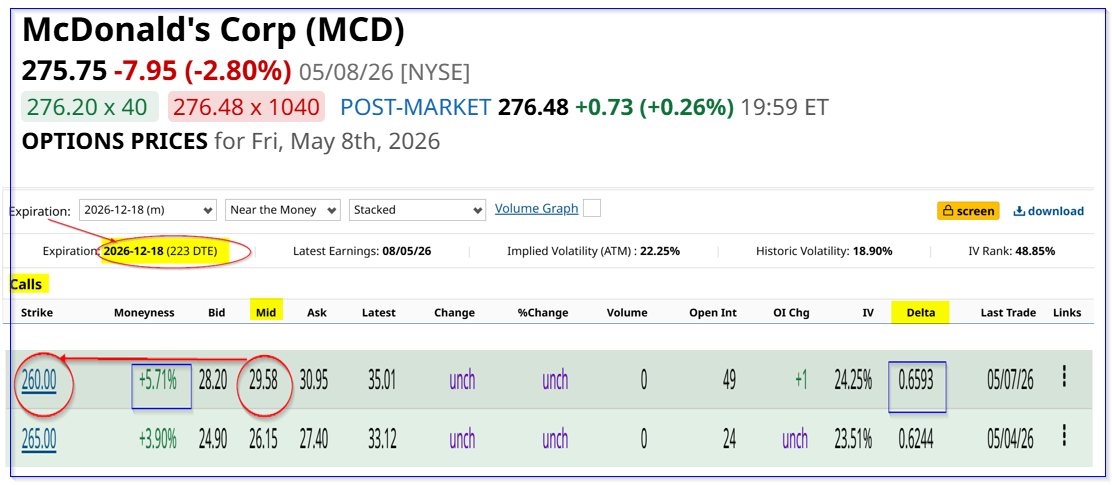

Another play is to use this short-put income each month to help pay for longer-dated in-the-money call options. For example, the December 18, 2026, expiry period shows that the $260 call option has a midpoint premium of $29.58.

So, the call option implies a breakeven of $289.58 (i.e., $260 + $29.58), or $13.83 higher than the trading price of $275.75 on May 8 (i.e., +5.0% higher).

In other words, the short-put income of $3.63 each month, if it could be repeated, this premium could be covered in 4 months (i.e., $13.83/$3.63 = 3.81). So, this is a profitable way to cover the extra premium over the intrinsic value of the call option.

The bottom line is MCD stock looks too cheap, and there are several ways to play this using out-of-the-money puts and in-the-money call options.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)