When Geopolitics Became the Only Chart That Mattered

Recent sentiment across CL and the broader energy complex has been dominated by a combination of geopolitical escalation and rapid shifts in supply expectations. The energy complex entered 2026 in a period of relative calm, with the EIA and J.P. Morgan both forecasting structural oversupply and a drift toward the $58 per barrel range by year end. That narrative was erased in a single weekend.

On February 28, the United States and Israel launched a coordinated air campaign against Iran, codenamed Operation Epic Fury, striking nuclear facilities, naval installations, and energy infrastructure. The Strait of Hormuz, which carries approximately 20 million barrels per day of global petroleum liquids, fell into near total disruption as tanker traffic halted and Iran's Revolutionary Guard began attacking commercial vessels throughout the Persian Gulf. This introduced an immediate and substantial risk premium into crude markets, as participants began pricing in the potential for severe disruption to Iranian exports and key regional transit routes.

However, that risk premium proved unstable. Within days of the initial rally, the U.S. Department of Energy signaled it was evaluating a coordinated Strategic Petroleum Reserve release alongside allied nations, which triggered a sharp liquidation in prices. At the same time, OPEC Plus members, led by Saudi Arabia, did not move to immediately adjust output targets, further reducing fears of an acute supply crunch. On March 18, Israel struck Iran's South Pars natural gas field, the world's largest, and Qatar's Ras Laffan export facility sustained heavy damage, threatening approximately 19 percent of global LNG trade. The IEA described the situation as "the greatest global energy security challenge in history." Most recently, on March 25, Reuters reported that U.S. special envoy Steve Witkoff transmitted a 15-point peace proposal to Iran via Pakistan, only for Iran to formally reject it shortly after. Today, March 26, Trump extended his pause on attacks targeting Iranian energy infrastructure to April 6, establishing that deadline as the market's next major focal point.

Crude oil is currently most sensitive to incremental geopolitical headlines, policy responses related to strategic reserves, and any shifts in OPEC Plus production guidance. The market is no longer reacting to broad narratives but to specific developments that directly impact supply or demand expectations.

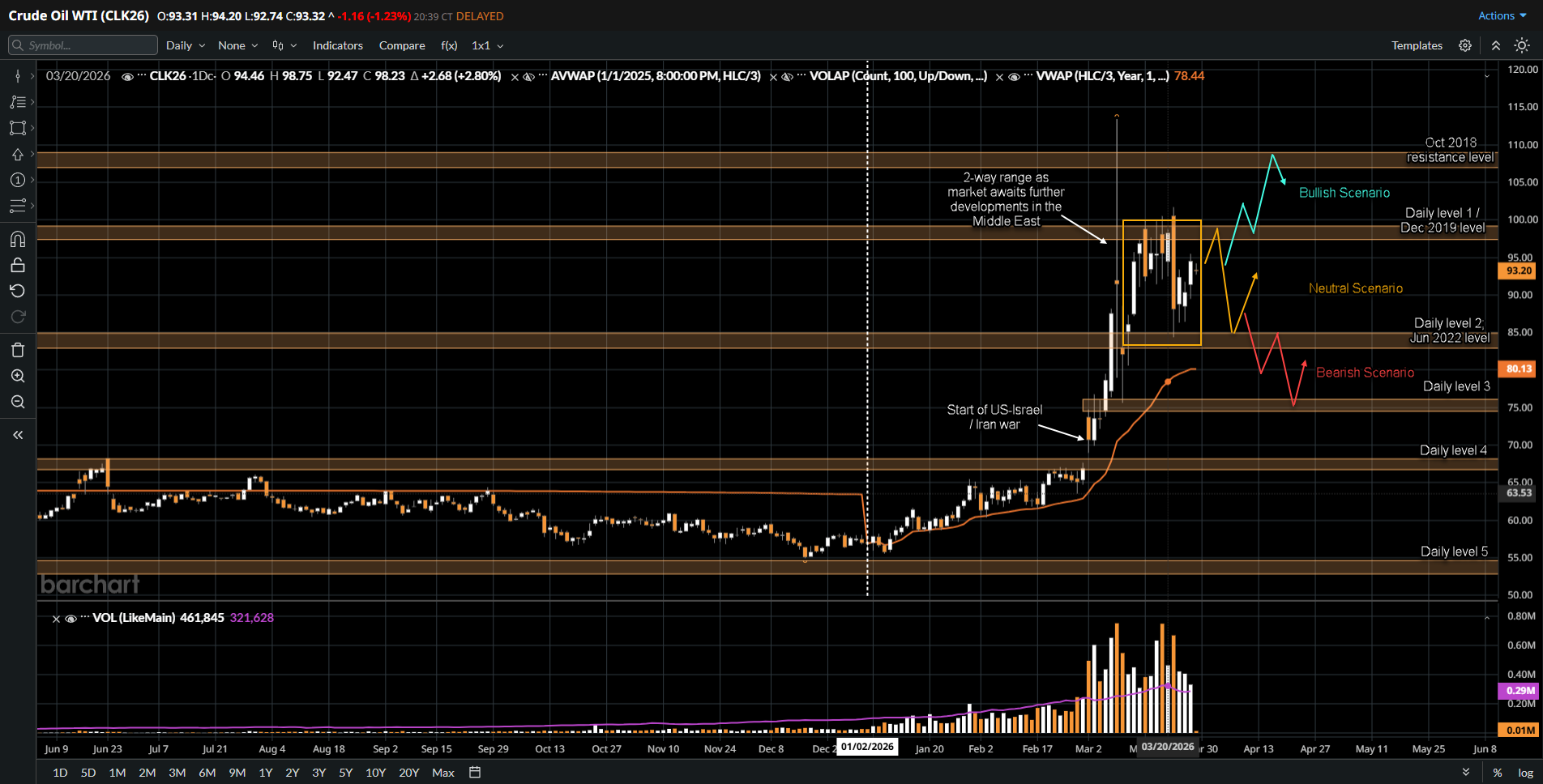

What the Market Has Done

- The conflict began on February 28 and by March 2, CL surged sharply as initial shock pricing set in across the energy complex.

- CL futures reached a high in the vicinity of 113, near the October 2018 resistance level, on March 9.

- Market retraced sharply back down to the 75 area (Daily Level 4) within a span of two days, as the IEA's coordinated emergency reserve release and demand destruction concerns weighed on prices.

- Buyers responded and bid price back up to the 100 area (Daily Level 1 / December 2019 level), as markets recognized the reserve release was insufficient to bridge the supply gap.

- In the past week, sellers responded and prices rotated back down to the 85 area (Daily Level 2 / June 2022 level), where buyers have responded, resulting in a two-way auction developing within the 100 and 85 range.

What to Expect in the Coming Weeks

The key levels to watch are 100 (Daily Level 1 / December 2019 level) and 85 (Daily Level 2 / June 2022 level).

Neutral Scenario

- If the market lacks velocity and volume as it approaches the 100 area (Daily Level 1), expect rotation back down to the 85 area (Daily Level 2), with continued two-way activity as the market establishes value and waits for further development.

- This remains the base case while diplomacy is unresolved and neither side has committed to a formal ceasefire timeline, with the April 6 deadline now serving as the next key inflection point.

Bullish Scenario

- The first clue that the bullish scenario is in play is if bids hold at the 92 area (mid of the range) and price compresses toward the 100 area, signaling that buyers are willing to absorb the diplomatic discount and bid through the range midpoint.

- If the market breaks and accepts above the 100 area, expect a move back up toward the 110 area.

- The fundamental catalyst for this scenario would probably be a failure of the peace process, renewed escalation (such as further strikes on Gulf energy infrastructure), or confirmation that the IEA reserve release is insufficient to move the needle on the physical market, as ING strategists have already stated that "the only way to see oil prices trade lower on a sustained basis is by getting oil flowing through the Strait of Hormuz."

Bearish Scenario

- The first clue that the bearish scenario is in play is if offers hold at the 92 area and price starts to compress toward the 85 area, suggesting the market is building confidence that the diplomatic path will ease supply risk before it escalates further.

- If the market breaks and accepts below 85, expect a move down to the 2026 VWAP, where buyers are expected to respond.

- If buyers fail to hold there, the next destination is the 75 area (Daily Level 3). The EIA's current base case forecast supports this path over the longer term, projecting CL below $80 in the third quarter of 2026 and around $70 by year end if Strait flows gradually resume, though the agency acknowledges the outlook is highly dependent on both the duration of the conflict and the resulting supply outages.

Conclusion

CL futures are at a genuine inflection point where technical structure and macro fundamentals are speaking the same language. The 100 and 85 areas define the current value range, the 92 area is the tell for directional commitment, and the 75 area remains the downside destination if buyers fail to defend the range low. Fundamentally, Iran's rejection of the 15-point peace proposal and Trump's extension of the energy infrastructure strike pause to April 6 have left the market in a state of armed uncertainty, sensitive to every headline and repricing aggressively in both directions. The Strait of Hormuz remains the single most important variable, and as ING strategists have noted, sustained downside in crude is not possible until oil flows through it again. Whether you are positioned for a diplomatic breakthrough or a breakdown in talks, the edges of this range are where the opportunity lives.

We provide the infrastructure you need to quantify your discipline and ensure every decision is backed by the confidence of seeing exactly what drives your performance. Start trading with the clarity you deserve. Open an Account today.

Disclaimer:

This article is provided for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis presented reflects the author’s market observations and opinions at the time of writing and is not a recommendation to buy or sell any futures contract, security, or financial instrument. Futures trading involves significant risk and is not suitable for all market participants. Losses may exceed initial margin deposits, and market conditions can change rapidly.

Any scenarios, levels, or market expectations discussed are hypothetical in nature and are intended solely to illustrate potential market behavior. They do not represent actual trading results and should not be interpreted as guarantees of future performance. Past performance, market behavior, or historical price action are not indicative of future outcomes.

Readers are solely responsible for their own trading decisions and risk management. Always conduct independent research, consider your financial situation and risk tolerance, and consult with a qualified financial professional, if necessary, before engaging in futures or derivatives trading.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)