Since the initial onslaught of the COVID-19 crisis, one of the arguably unintuitive bull markets stemmed from the housing sector. During the early days of the pandemic, most people sheltered in place, wondering what the future might hold as economic activity nearly ground to a halt. However, the influx of accommodative fiscal and monetary policies meant that borrowing costs hit subterranean levels.

In turn, many astute individuals recognized the once-in-a-blue-moon opportunity, bidding up home prices to ridiculous valuations. However, with the Federal Reserve expanding the money stock at an unprecedented rate, holding cash presented problems. Therefore, those with the financial ability to do so saw a golden opportunity in real estate.

Of course, all good things must come to an end. While the future trajectory of home prices remains a hotly debated topic, it’s clear that at the very least, the broader housing market needs a breather. With the dramatic loss of purchasing power, many prospective homebuyers found themselves priced out. As demand slowly left the once-hot arena, sellers increasingly began lowering prices.

Still, with experts on both sides of the aisle offering conflict viewpoints, how do homebuyers know which voices to trust? Ultimately, every person must conduct their own due diligence and make the decision that they are most confident in.

However, before pulling the trigger, it’s helpful to consider one key metric: days inventory.

Days Inventory as the Primary Arbiter

For publicly traded companies, it’s quite normal for management teams to spin any news – even the less-encouraging datapoints – in the most optimistic light possible. Indeed, stakeholders wouldn’t have it any other way. Otherwise, being too blunt about organizational challenges could lead to significant volatility.

At the same time, to gain a truly objective perspective, investors should analyze the hard numbers on their own. For the housing market, both investors and homebuyers should consider public homebuilders’ days inventory line item, which indicates the average number of days a company takes to turn its inventory.

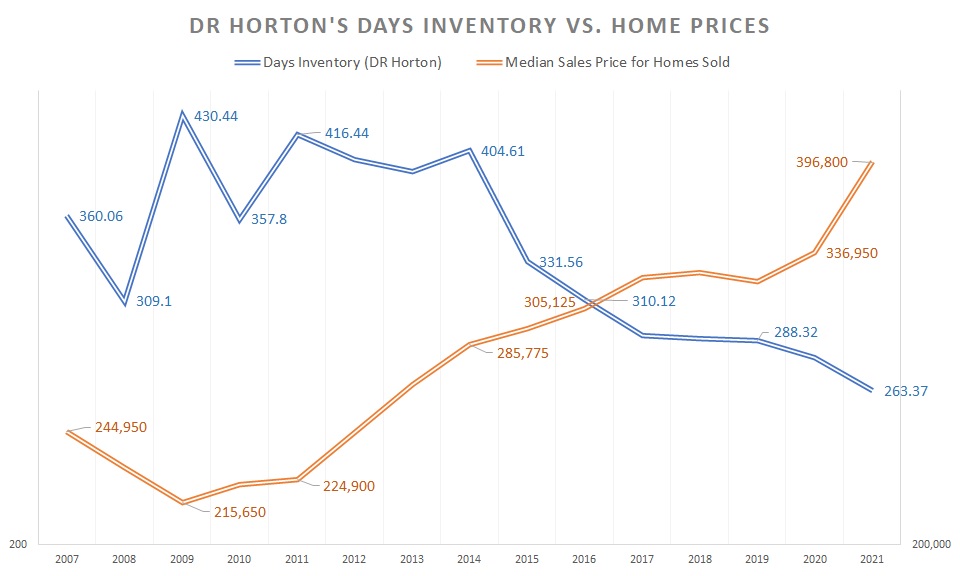

For companies like D.R. Horton (DHI), it’s not so much the nominal figure itself but its trajectory and more importantly, any pivots or transitions. As well, it’s helpful to juxtapose the days inventory metric to broader indices, such as home prices. Conducting this exercise for D.R. Horton against the median sales price of homes sold in the U.S. reveals the following trend:

Generally speaking, as days inventory declines, home prices rise and vice versa. In fact, the correlation coefficient in the chart above is -78.4%, reflecting an inverse relationship. Again, as one metric rises, the other declines.

Fundamentally, this dynamic makes perfect sense. As supply in D.R. Horton’s books increases, greater pressure materializes for management to convert said inventory into sales. On the flip side, reduced supply means that buyers must compete against each other to secure a new home.

The Fed Complicates Matters

Interestingly, while D.R. Horton’s days inventory slipped to 263.37 for its fiscal year ended Sept. 30, 2021 (thus corresponding to a blistering high $396,800 median home sales price), on a trailing-12-month basis, days inventory jumped to 307.21. That’s nearly a 17% increase from fiscal 2021’s tally.

Several years ago, between 2008 and 2009, D.R. Horton’s days inventory jumped from 309.1 to 430.44, a 39% jump shot. During the same period, home sale prices declined 6%. Therefore, some might assume that because such a wide increase in supply only resulted in a relatively minor reduction in the home sales price, any future correction from this point forward will be mild.

It’s not out of the question. However, the key difference between the Great Recession and the present juncture is the willingness for governmental intervention. Back then, the Obama administration launched multiple initiatives to rescue the housing market. On the monetary end, the Fed implemented dovish policies to spark business momentum.

Today, the opposite dynamic is true. Following a blistering inflationary cycle, Americans have grown concerned about interventions. Plus, Fed chair Jerome Powell issued a warning that some pain could be ahead as the central bank is now committed to addressing inflation. And that means higher borrowing costs to slow the economy, which almost invariably implies lower housing prices.

Not Holistically Great News

For prospective homebuyers that found themselves priced out of the wild housing market, the upcoming months (perhaps years) may spell an acquisitive opportunity. But like any other circumstance in the new normal, things aren’t quite so cut and dry.

Namely, as economic pressures build, several tech firms – including well-known enterprises – have initiated layoffs. With more good jobs on the chopping block, discretionary spending will likely decline. In turn, that will likely impact other sectors, perhaps leading to pink slips in non-tech-related industries.

So, while potentially lower home prices may be a positive, buyers must also ensure they have an income coming in. Otherwise, the discount could end up becoming a trap.

More Stock Market News from Barchart

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)