/CPU%20Chip.jpg)

For decades, investing for me has started and ended with what the chart is telling me. Markets, stocks, and exchange-traded funds (ETFs), via their price behavior, tell us a continuous story. I prioritize listening to that story, not ignoring it.

However, between the start and end of a trade or long-term investment is the other part. It is the part that many investors immerse themselves in, often to the exclusion of technical analysis. I applaud and respect their work, even if my “emphasis pie” in my analysis looks different than theirs.

I’m talking about the factors: valuation, growth, fundamental soundness/quality, and the narrative/news/events surrounding the stock or ETF. Those matter too. My main difference from the masses? I think it all ends up being reflected in the price pattern.

This is why my approach to investing since the 1990s has been to keep up with, acknowledge, but largely ignore most of the ongoing exercise of “why” something may go up or down or sideways in price. Because I’ve become convinced over time that the why matters less than the what — what the price is actually doing and what it is likely to do going forward.

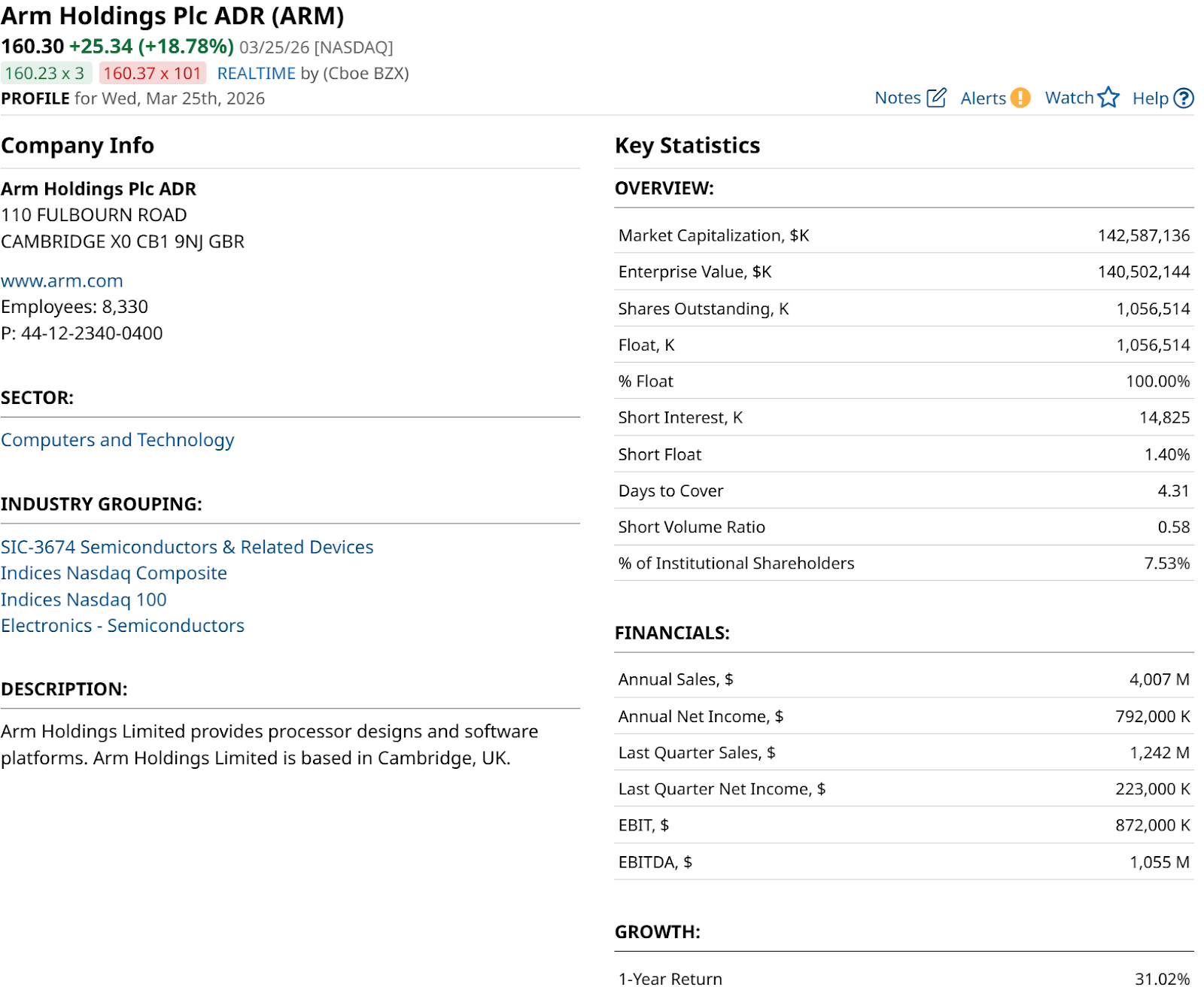

A Closer Look at Arm Holdings

I’m keeping that in mind as I talk about Arm Holdings (ARM), following its 19% spike Wednesday morning. ARM dates back to 1990 and was a public company, then a Softbank Group (SFTBY) division, and then a public company again when spun off in 2023.

When I see a stock spike like that, I want to run to the charts and figure out, “Is that it?” Like Oracle (ORCL) last year, when it rallied more than 30% in a day, then slowly eroded that gain. Or, is this a true reawakening that is the rare — but sometimes viable — “bell they ring at the bottom.” So, the charts will wait a minute in this case.

This explosive leg up in ARM stock effectively ends the stock's recent sideways consolidation and marks a fundamental transformation in its business model. For decades, Arm operated as the Switzerland of chips, quietly licensing architecture to the world's tech giants. That era is over. The catalyst for Wednesday's vertical move is the company officially entering the physical silicon business with its first in-house data center chip, the AGI CPU.

Wall Street is treating this pivot as a total repricing event rather than a simple product launch. Analysts at Guggenheim and HSBC have recently scrambled to raise their price targets as high as $240, arguing that the market is still undervaluing a game-changing shift toward AI infrastructure.

The company is now projecting that its new chip architecture will generate $15 billion to $24 billion in annual revenue within five years. To put that in perspective, ARM generated roughly $4 billion in total revenue in 2025.

So, this is no longer a royalty story. It is a direct hardware play aimed at capturing 15% of a $100 billion data center market.

Now that we know what’s going on in the real world, let’s look at the world that matters most when it comes to our money: the charts.

What Does ARM’s Chart Say About the Stock’s Next Move?

This daily view is hopeful but inconclusive. Because while there’s still room for a very popular topping point around $180 a share, that 11% up from here carries a lot of risk. I’ll use my ROAR score analysis below to show why, after we review the weekly chart.

And when I do, as shown below, I have to say, it’s the same darn picture. Except for one very important feature, via the PPO indicator in the bottom section of the chart.

That’s a crossover from a very low level. Translation: The stock is trying to lift off, but the risk is still high since PPO is still floating below the 0.00 level. We simply have to look at the same type of view back in April of last year. It looks the same, doesn’t it? If that history repeats, a 20% move higher in ARM would not surprise me.

But that’s a trade. Investment-wise, the bigger issue is how markets now function around stocks like this, in the tech sector. Case in point, that same 2025 move up and down — $80 to $180 and back to $100, all in the space of eight months! That’s one way to make a 25% profit.

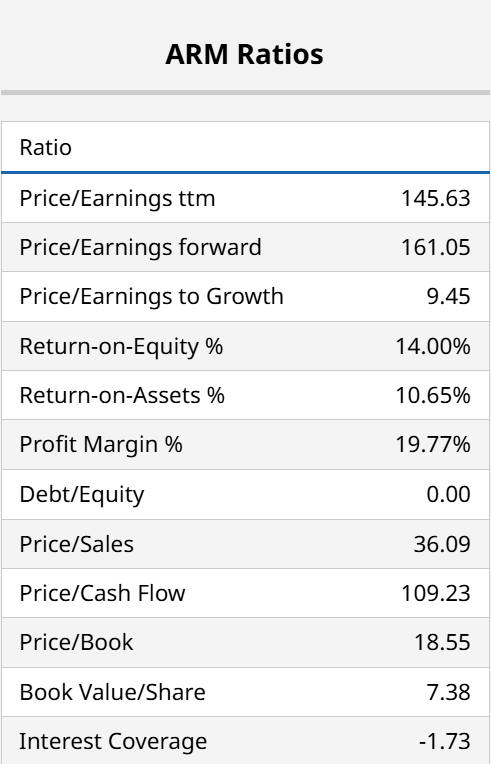

The fundamental risk remains valuation. Even with the new revenue projections, Arm trades at a forward price-to-earnings (P/E) ratio of more than 160x. Too rich for me, albeit those are figures that do not reflect the company’s new direction. Nor does it reflect the new risks to competing in that field. Or, the AI trade-fade risk that continues to be a market-wide overhang.

Wednesday’s move is a reminder of why chasing individual high flyers can lead to wasted research when the underlying index correlations remain so high. If the Nasdaq 100 (QQQ) takes a breather, even a fundamental breakout like ARM stock will likely face a gravity check.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)