/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

AI-focused infrastructure stocks have been red-hot as companies race to build massive GPU-based clouds. Smaller “neocloud” providers alongside giants like Microsoft (MSFT) and Nvidia (NVDA) are in a frenzy of deals and capacity builds. But now, there are also relatively new companies getting in focus along with big tech Gaints.

One company drawing fresh interest is Nebius Group (NBIS). Recently, Bank of America initiated coverage with a “Buy” rating and a $150 price target. That calls for roughly 30% upside from current levels. The move follows a year when Nebius shares have surged on excitement over AI demand and big contracts.

As bottlenecks on Intel (INTC) and AMD (AMD) GPUs are alleviated, specialized AI cloud companies are gaining attention. BofA highlighted that Nebius is the leader in the fast-growing AI Infra-as-a-Service (IaaS) market, and the recent surge in the stock has been compared and contrasted to other AI infrastructure success stories despite its already-stratospheric rise.

About NBIS Stock

Spun out of Yandex in 2024, Nebius Group is an AI cloud infrastructure firm that focuses on ultra-large GPU data centers for AI workloads. Nebius sells “AI infrastructure,” leasing compute clusters to train and serve models, so clients like startups or enterprise AI teams avoid building their own farms. Its customers include Microsoft and Meta (META), and it even operates smaller tech subsidiaries: Toloka AI data platform, TripleTen edtech, and Avride autonomous driving, inherited from Yandex. Nebius’s growth hinges on selling capacity on its purpose-built GPU supercomputers.

Over the past year, NBIS stock has exploded. In the last 12 months, Nebius jumped roughly 320%. That rocket ride was fueled by news of massive deals and funding: for example, Nebius announced a $27 billion AI-cloud agreement with Meta, initially $12 billion, with $15 billion more optional, and raised over $4 billion through convertible notes. Unsurprisingly, then, analysts have kept upping their price targets, e.g., BWS Financial lifted its PT to $200 on the Meta deal.

Nebius still trades at very high valuations compared with most cloud companies. Even after pulling back from late-2025 highs, the stock trades above 40× enterprise value to sales. The company generated about $530 million in 2025 revenue, while its enterprise value is around $22 billion. Its trailing price-to-sales ratio is close to 55×. Bank of America also noted that some valuation models suggest Nebius appears expensive relative to its estimated fair value. Investors buying the stock are now betting that several years of rapid growth will justify the high valuation. Supporters argue Nebius could generate $7 billion to $9 billion in revenue by 2026, which could help support the premium.

Bank of America’s Call

On March 24, Bank of America became the latest firm to weigh in. Its analysts initiated coverage with a “Buy” rating and a $150 target. BofA highlighted Nebius’s “large addressable market” of $419 billion in AI infrastructure by 2028 and strategic contracts with Meta and Microsoft. The report called Nebius’s offering a “huge opportunity” for customers to train models without building their own data centers. Notably, BofA’s team said Nebius’s positioning with key hyperscalers could let it capture an outsized share in distributed AI compute.

Overall, the fresh coverage from a heavyweight like BofA adds weight to the bullish case, but it didn’t send prices sharply higher, perhaps because investors had been eyeing such a report coming. Still, BofA’s stamp that Nebius is “strategically positioned” has likely broadened investor interest. And with the stock already volatile after bonds and partnership news, the upgrade may tighten Nebius’s narrative as a top AI-cloud pick.

Quarter to Quarter: Scaling Rapidly at Cost

In Q4, Nebius missed estimates on both revenue and earnings yet showed a company in hypergrowth mode. Revenues surged to $227.7 million in Q4, up 547% year-over-year (YoY) from $35.2 million. On a full-year basis, 2025 sales were $529.8 million, a 479% jump. The lion’s share came from its core AI cloud segment. Management said core cloud revenue alone grew 830% YoY in Q4.

Losses are still large, however. Q4 net loss from continuing operations widened to $249.6 million versus $122.9 million a year earlier, driven by heavy operational spending and depreciation. Even on a non-GAAP basis, adjusted net losses more than doubled. The company is not profitable yet, which CEO Arkady Volozh describes as a tradeoff for growth. He said the team scaled capacity and delivered it to customers quickly and reliably, adding that demand remained strong even before new capacity came online.

Nebius continues to spend heavily as it expands. It generated about $834 million from operations in Q4 but spent around $2.06 billion on capital projects, mainly data center equipment. Free cash flow was therefore deeply negative at roughly negative $1.2 billion in the quarter. Liquidity remains solid, however. Nebius ended 2025 with about $3.68 billion in cash and equivalents, up from $2.43 billion a year earlier.

Looking ahead, Nebius reiterated aggressive guidance. Management confirmed its 2026 revenue target of $3.0 billion to $3.4 billion. Analysts expect the company to remain unprofitable, with consensus forecasts for FY2026 EPS between negative $1.10 and negative $0.81 per share as spending continues. Nebius is also targeting about 40% adjusted EBITDA margins next year as scale improves.

Mega-Deals and Expansion

Nebius has kept busy in early 2026 with several big headlines. The marquee news was Nvidia’s investment. On March 11, Nvidia announced a strategic partnership and a $2 billion investment in Nebius. The deal means Nvidia will supply hardware like Rubin GPUs, Vera CPUs, etc., and work with Nebius on designing “AI factories.” Nvidia CEO Jensen Huang praised Nebius as “an AI cloud designed for the agentic era,” and Nebius’s Arkady Volozh noted it will let them build “one of the first and largest clouds for all AI builders.”

However, Nvidia's backing is a strong signal; it not only confirms Nebius’s deep relationships with chipmakers but also helps Nebius accelerate its buildout, helping it reach 5 GW of capacity by 2030.

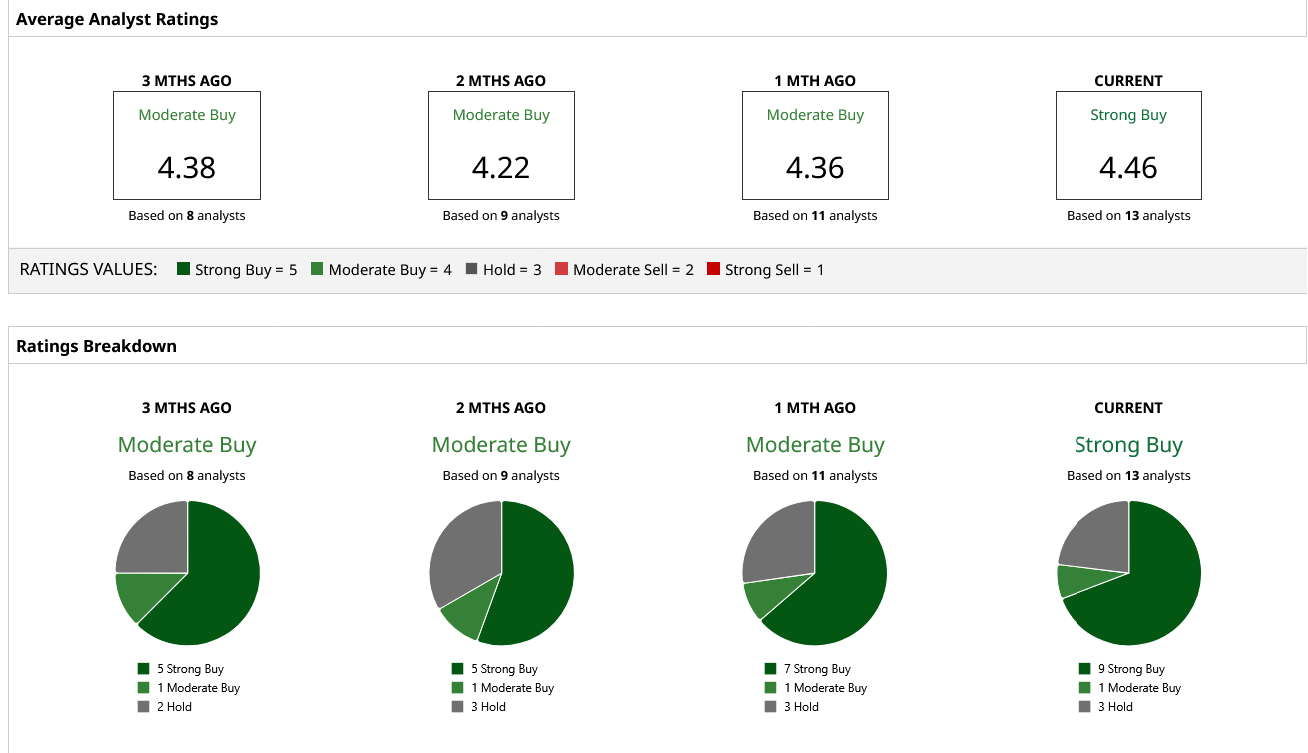

What Analysts Are Saying About NBIS Stock

Wall Street analysts are largely bullish on NBIS Stock with a consensus “Strong Buy” rating. The group of 13 analysts has set a 12‑month median target of roughly $169, an upside premium of about 48%. Collectively, the Street expects Nebius to deliver explosive revenue growth to the multi-billions and only gradually improve profitability. The key debate remains whether those long-term prospects are worth paying a steep price for today. As one analyst put it, Nebius’s run “reinforces its position” as a top AI cloud play, but one reliant on phenomenal execution.

In my opinion, BofA’s bullish call adds confidence that Nebius still has runway, but anyone buying at current levels is banking on nearly a tripling of revenue within a year or two. If Nebius hits its 2026 sales targets and smooths out its losses, current metrics could prove reasonable. If not, the high bar will loom large. As one analyst likes to say, Nebius was “built for AI since day one,” and investors must decide if that genesis is enough to sustain today’s lofty expectations.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)