TKO Group Holdings, Inc. (TKO), headquartered in New York, provides sports entertainment services, as well as focuses on organizing live events. Valued at $37.7 billion by market cap, the company is also involved in the merchandising of video games, apparel, equipment, trading cards, memorabilia, digital goods, and toys.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and TKO definitely fits that description, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the entertainment industry. TKO’s strength lies in its dominant UFC and WWE brands, driving media rights, events, and sponsorship deals.

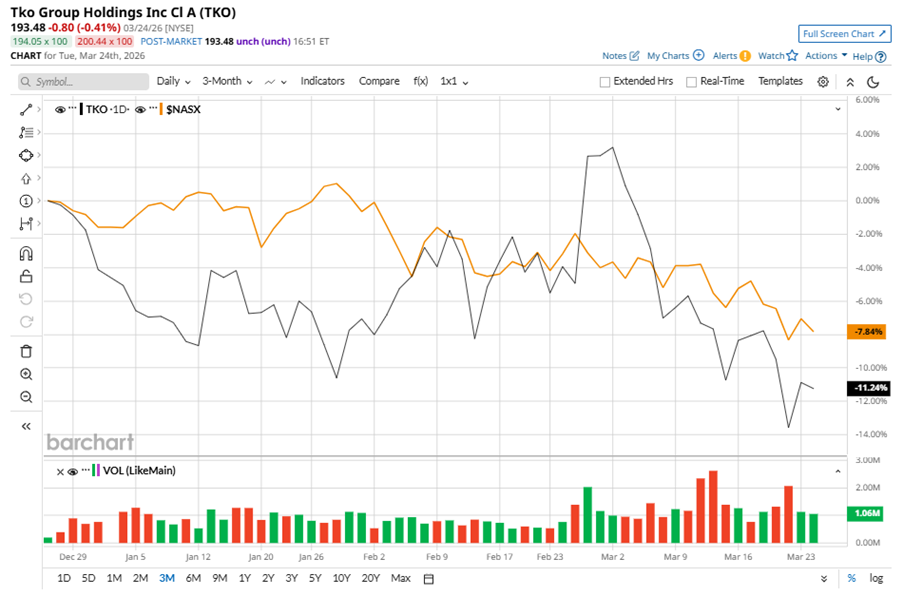

Despite its notable strength, TKO slipped 14.7% from its 52-week high of $226.94, achieved on Feb. 26. Over the past three months, TKO stock declined 11.2%, underperforming the Nasdaq Composite’s ($NASX) 7.8% losses during the same time frame.

Shares of TKO fell 1.2% on a six-month basis but climbed 26.5% over the past 52 weeks, outperforming NASX’s six-month 3.3% dip and 19.7% returns over the last year.

To confirm the bullish trend, TKO has been trading above its 200-day moving average over the past year, with slight fluctuations. However, the stock is trading below its 50-day moving average since early March, with minor fluctuations.

On Feb. 25, TKO reported its Q4 results, and its shares closed up over 8% in the following trading session. Its loss of $0.08 per share fell short of Wall Street expectations of EPS of $0.14. The company’s revenue was $1.04 billion, surpassing Wall Street forecasts of $1.02 billion. TKO expects full-year revenue in the range of $5.7 billion to $5.8 billion.

TKO’s rival, Madison Square Garden Sports Corp. (MSGS) has taken the lead over the stock, with a 44.6% gain over the past six months and a 57.6% uptick over the past 52 weeks.

Wall Street analysts are reasonably bullish on TKO’s prospects. The stock has a consensus “Moderate Buy” rating from the 23 analysts covering it, and the mean price target of $233.06 suggests a potential upside of 20.5% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Apple%20logo%20-%20by%20Pexels%20via%20Pixabay.jpg)