Expand Energy Corporation (EXE) stands as the largest natural gas producer in North America, with a business model centered on supplying gas to both domestic and global markets. The company strategically aligns its expansive production base with regions experiencing rising demand, positioning itself to benefit from the growing importance of natural gas in the evolving global energy landscape. Companies with market capitalizations of $10 billion or more are generally classified as “large-cap stocks,” and Expand Energy easily clears that bar.

With a valuation of roughly $25.9 billion, the company stands firmly in large-cap territory, underscoring its scale and established presence within the energy space. Its strategy is centered on generating consistent returns by utilizing a diversified asset portfolio, maintaining financial discipline, and driving operational efficiency. As natural gas continues to be viewed as a relatively lower-carbon and reliable energy source, Expand Energy remains positioned within a segment of the market that is seeing steady long-term demand.

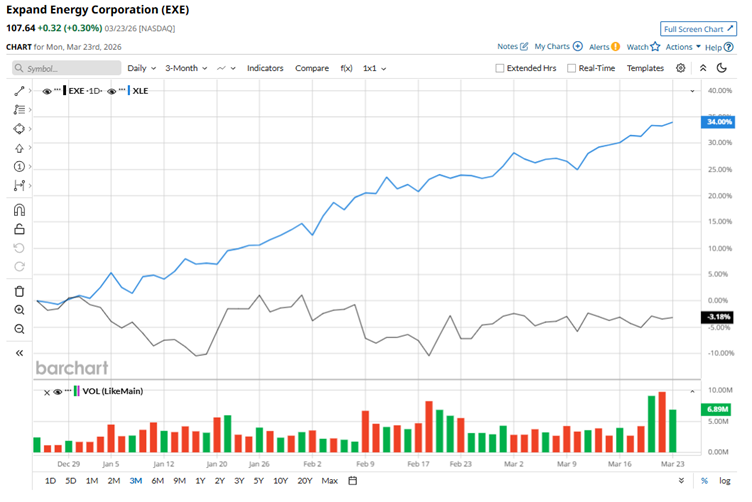

However, despite its strengths, Expand Energy is struggling to win over Wall Street. After climbing to a 52-week high of $126.62 last December, the stock has pulled back sharply, down nearly 15% from that peak. Recent performance hasn’t offered much relief either. Over the past three months, shares have slipped 3.2%, lagging well behind the State Street Energy Select Sector SPDR ETF (XLE), which has surged an impressive 34% over the same period, highlighting the stock’s relative underperformance in an otherwise strong energy market.

The longer-term picture doesn’t offer much improvement. While the stock has inched higher, its gains remain modest, especially when stacked against the Energy Select Sector SPDR ETF, which has delivered a strong 28.9% return over the same period. The stock has been stuck in a tight range, hovering close to both its 50-day and 200-day moving averages since mid-February. This lack of clear direction signals a period of consolidation, with neither bulls nor bears firmly in control.

Unlike most energy stocks that have been lifted by rising geopolitical tensions in the Middle East, Expand Energy has had a tougher start to the year. Its heavy exposure to natural gas has weighed on performance, particularly as concerns around potential oversupply in 2027 continue to dampen sentiment. Still, beneath the volatility, the company’s fundamentals remain resilient.

In its fiscal 2025 fourth-quarter results released on Feb. 17, Expand Energy delivered a strong earnings beat despite a challenging pricing environment for natural gas. Revenue surged to $3.27 billion, up an impressive 63.5% year over year and well ahead of the $2.25 billion estimate. Profitability told an even stronger story. Adjusted EPS jumped to $2.00, marking a remarkable 263.6% increase from the prior year and comfortably topping expectations of $1.89 per share

In a highly competitive energy landscape, EXE has struggled to keep pace with its peers. The stock has notably lagged Coterra Energy Inc. (CTRA), which delivered a 17.7% gain over the past year, highlighting EXE’s relative weakness despite broader sector strength.

Nevertheless, Wall Street’s stance on EXE remains firmly optimistic. Of the 29 analysts covering the stock, the consensus rating lands at a “Strong Buy,” reflecting broad confidence in its outlook. The average price target of $133.67 suggests a potential upside of around 24% from current levels, indicating that, despite recent underperformance, analysts see meaningful room for the stock to rebound.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)