This closure of the Strait of Hormuz is quickly causing a shift in the energy market, causing oil prices to rise and in turn causing a ripple effect in the entire global shipping industry. For tanker stocks, this is not noise; this is a real earnings driver. Longer distances, more complex logistics, and higher freight rates are causing a perfect storm that is likely one of the most favorable environments for this industry in quite some time. And this is precisely why stocks such as Frontline Plc (FRO) are again in the spotlight.

Tanker stocks historically perform well in environments of volatility and not necessarily environments of stability. And right now, this market is not only volatile; it is structurally tight. With limited additions in capacity and still strong demand, even minor disruptions cause outsized profitability. But is this a short-term pop or is this more sustainable?

About Frontline Stock

Frontline is one of the largest oil tanker companies in the world, based in Cyprus and owning a large fleet of VLCCs, Suezmax, and Aframax vessels. With a market capitalization of around $7.3 billion, Frontline is right in the middle of the global oil transportation business, and this is an industry that becomes extremely valuable in times of logistics and transportation difficulties.

The stock has performed well in recent times, up by 7.5% in just the last five trading sessions as tanker rates react to geopolitical tensions. But in the longer term, Frontline has significantly outperformed the market in times of shipping tightness and is a high-leverage business for those in the industry. Unlike stocks such as the S&P 500 Index ($SPX), which tend to move gradually in one direction, stocks such as Frontline tend to move in bursts, and this is likely one of those times.

From a valuation perspective, Frontline is trading on a price-to-earnings of 18.27 times and a price-to-sales of 3.72 times. These multiples are not stretched in light of current earnings. Moreover, the current price-to-cash flow of 10.73 times indicates that the market is still not entirely factoring in peak cycle earnings. The key here is that tanker stocks are not valued on multiples, they are cyclical in nature and can see earnings growth explode in a tight market.

Another interesting aspect of Frontline is its return of capital to shareholders. It has announced a $1.03 per share dividend for Q4 2025 alone. Now, this is not something that can be ignored; this is a sign of things to come.

Frontline Beats on Earnings

Frontline has reported a strong fourth quarter for 2025, reporting a profit of $227.9 million, or $1.02 per share, slightly higher on an adjusted basis of $1.03. It also reported revenue of $624.5 million, as it benefited from robust time charter equivalent rates for all vessel classes.

However, it is important to note that the real key here is that its VLCCs earned $74,200 per day, Suezmax tankers $53,800 per day, and Aframax/LR2 vessels $33,500 per day. These rates are healthy. Furthermore, this was done prior to the current geopolitical disruption of the U.S.-Iran War.

The management commentary was full of confidence. They pointed out the fundamental imbalance between oil demand and fleet supply - a situation that has been building for a number of years. To mitigate this, the company is investing in its fleet. They are selling older ships for $831.5 million and investing over $1.2 billion in newer, more efficient vessels. This is not a defensive strategy. This is a forward-thinking strategy.

A strategic aspect to this situation is not always considered. They have entered into one-year time charter agreements for their fleet, which pay as high as $93,500 per day. This serves as a backstop for the company in case spot rates come down. This is a subtle but important move.

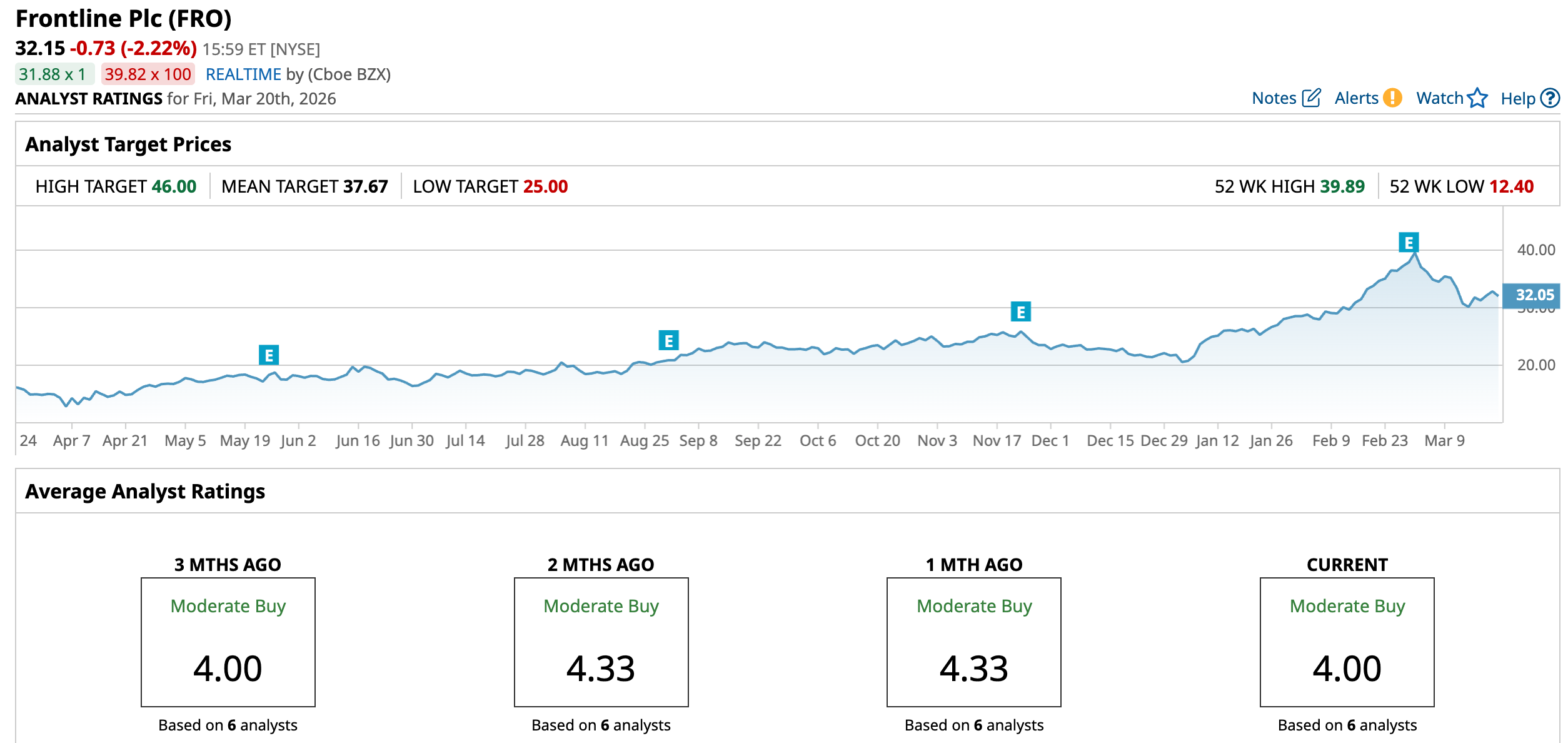

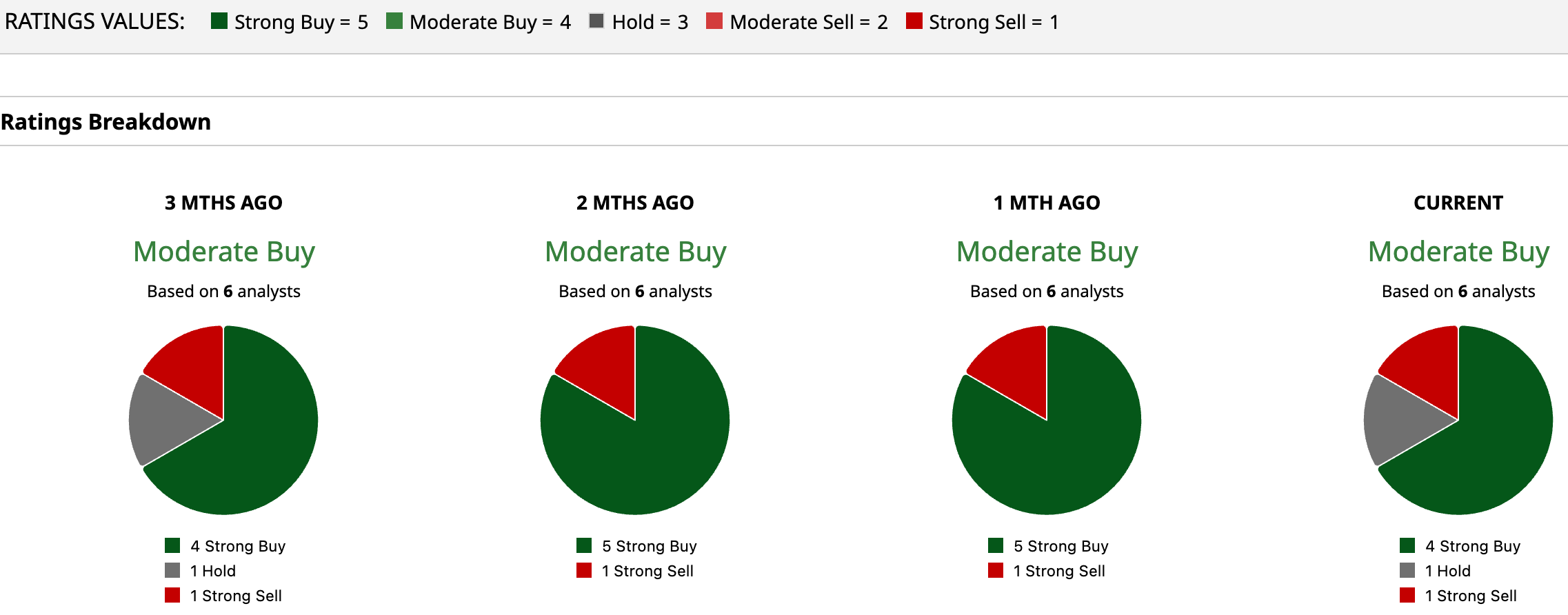

What Do Analysts Expect for Frontline Stock?

Wall Street is positive about Frontline stock with a “Moderate Buy” rating consensus. Analysts have set targets ranging from a low of $25 to a high of $46. The mean is set at $37.67. Based on the current stock price, significant upside potential could be 17.17%.

What is interesting is that analysts have not adjusted their targets for the latest geopolitical events. Most of them were set prior to the Strait of Hormuz incident. If oil tanker rates stay high, it is possible that analysts will increase their targets.

However, this is a situation in which investors should be reminded of the nature of oil tankers. These stocks are notorious for their boom-and-bust nature. When conditions are right, these stocks seem to be unstoppable. However, when rates come back down to normal, earnings can quickly compress.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Intuit%20Inc%20logo-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)