American Airlines (AAL) has stepped into a critical stretch with demand on its side, yet operational friction threatens to steal the spotlight. The carrier commands one of the most powerful networks in the United States, with hubs across eight of the 10 largest metropolitan areas, placing it at the heart of global aviation flows.

That advantage, however, has now met a bottleneck that few airlines can control. The warning from U.S. Transportation Secretary Sean Duffy lands with weight. Staffing shortages at the Transportation Security Administration risk slowing airport throughput, and in extreme cases, could even force temporary shutdowns.

Early signs already paint a strained picture. Security lines stretching up to four hours undermine the very convenience air travel sells. Acting Deputy TSA Administrator Adam Stahl underscored the pressure, noting the system operates at full stretch with little room to absorb shocks, especially at smaller airports.

Timing has sharpened the risk. Spring break demand is peaking, while mega-events like the FIFA World Cup 2026 and the United States Semiquincentennial promise sustained travel momentum. Airlines are expected to handle 171 million passengers this spring, turning what should be a clean tailwind into a delicate balancing act.

Against this backdrop, let us see if grabbing shares of American Airlines could be a wise choice.

About American Airlines Stock

Based in Fort Worth, Texas, American Airlines operates a vast domestic and international network. With a market cap of roughly $7.1 billion, the airline runs more than 6,000 daily flights, connects over 350 destinations across 60+ countries, and serves upwards of 200 million customers each year.

The stock has declined 6% over the past 52 weeks and fallen 15% in the last six months. Recent trading offers a glimmer of stabilization, with a 2.6% gain over the past five trading sessions, hinting that sentiment may be finding a floor.

From a valuation standpoint, AAL stock is trading at 6.24x forward adjusted earnings and just 0.12x sales. Both metrics sit below industry norms and the company’s own five-year averages. The discount signals caution priced in, but it also opens the door for investors willing to look past near-term turbulence.

A Closer Look at American Airlines’ Q4 Earnings

On Jan. 27, American Airlines unveiled its Q4 fiscal 2025 earnings results, wherein revenue rose 2.5% year-over-year (YoY) to $14 billion, landing broadly in line with expectations of $14.04 billion. The growth came despite a $325 million headwind tied to the government shutdown, which weighed heavily on domestic operations.

Passenger unit revenue in the domestic segment declined 2.5%, though management noted it would have turned positive without that disruption. Profitability, however, told a softer story. Non-GAAP net income reached $106 million, while adjusted EPS amounted to $0.16, missing the $0.35 analyst estimate.

Looking ahead, early indicators point to improving momentum. Systemwide revenue for the first three weeks of 2026 has grown at a double-digit pace, driven by strength in premium cabins and corporate travel. Management now expects Q1 unit revenue to turn solidly positive, with total revenue projected to grow between 7% and 10%.

Full-year fiscal 2026 guidance adds another layer of optimism. Adjusted EPS is expected to be between $1.70 and $2.70, alongside free cash flow exceeding $2 billion.

Analysts align with this trajectory. They expect Q1 fiscal 2026 loss per share to narrow 32.2% YoY to $0.40 per share, followed by a sharp EPS rebound of 352.8% from the previous year to $1.63 in 2026 and a further 74.9% growth to $2.85 in fiscal year 2027.

What Do Analysts Expect for AAL Stock?

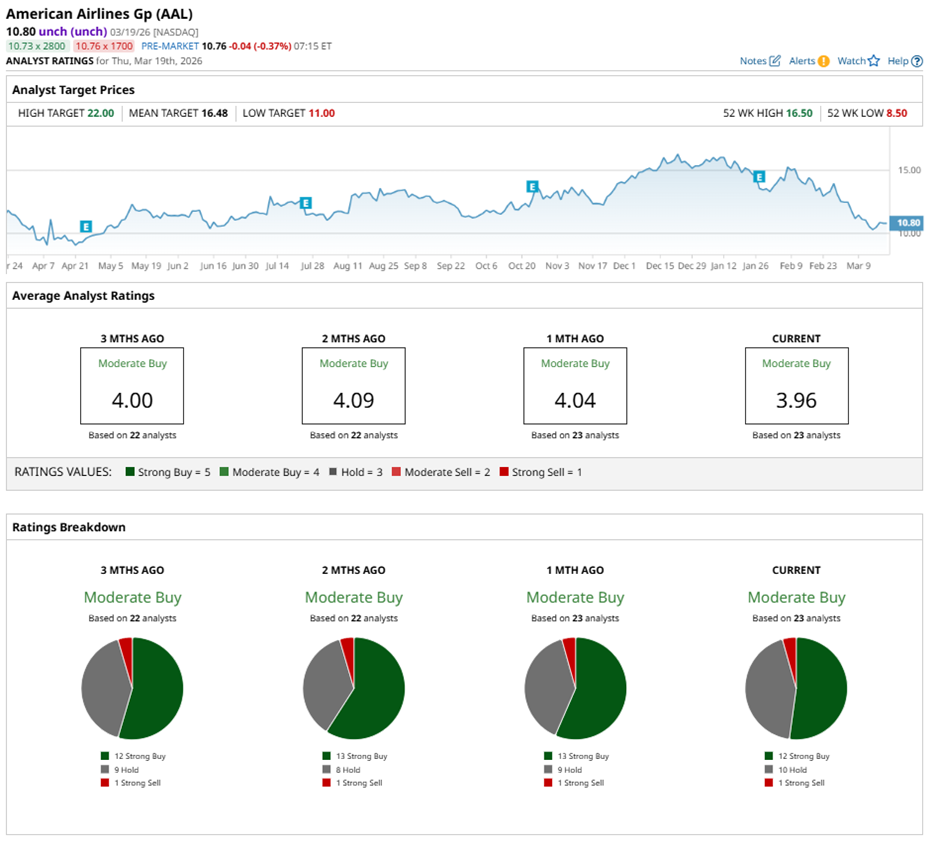

Wall Street maintains a favorable stance on AAL stock, even as near-term uncertainties linger. Among 23 analysts, the consensus rating stands at “Moderate Buy,” out of which 12 recommend a “Strong Buy,” 10 suggest “Hold,” and only one leans toward a “Strong Sell.”

Price targets reinforce the cautiously optimistic view. The average price target of $16.48 implies potential upside of 53%. Meanwhile, the Street-high target of $22 points to a gain of 104% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Visa%20Inc%20gold%20card-by%20hatchpong%20via%20iStock.jpg)