/DaVita%20Inc%20sign%20on%20building-by%20photo-denver%20via%20Shutterstock.jpg)

DaVita Inc. (DVA), headquartered in Denver, Colorado, provides kidney dialysis services for patients suffering from chronic kidney failure. Valued at $10 billion by market cap, the company operates kidney dialysis centers and provides related lab services in outpatient dialysis centers.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and DVA perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the medical care facilities industry. DVA is a trusted leader known for quality care and innovation in kidney care. Its integrated approach offers services from diagnosis to transplant support, making it a comprehensive healthcare provider. Its focus on personalized care at scale has built strong patient trust and brand equity, solidifying its market dominance of over 25 years.

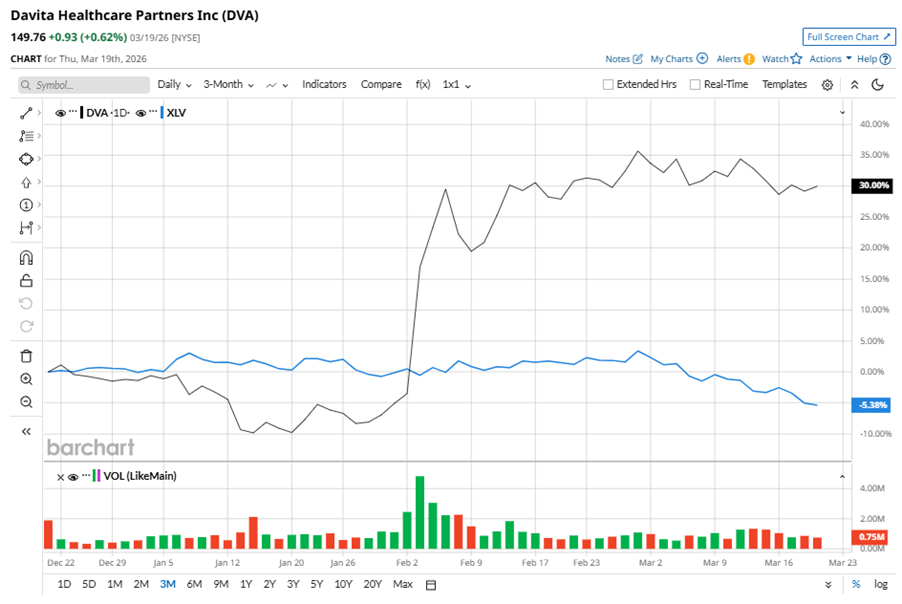

Despite its notable strength, DVA slipped 6.1% from its 52-week high of $159.42, achieved on Mar. 2. Over the past three months, DVA stock has gained 30%, outperforming the State Street Health Care Select Sector SPDR ETF’s (XLV) 5.4% decline during the same time frame.

Shares of DVA rose 15.1% over the past six months, outperforming XLV’s six-month 6.8% gains. Meanwhile, the stock dipped slightly over the past 52 weeks, mostly aligning with XLV’s marginal losses over the last year.

To confirm the bullish trend, DVA has been trading above its 50-day and 200-day moving averages since early February.

DVA's outperformance is driven by revenue growth and disciplined execution in Integrated Kidney Care. Its strong patient outcomes and cost control offset higher health benefit costs.

On Feb. 2, DVA reported its Q4 results, and its shares closed up more than 21% in the following trading session. Its revenue was $3.6 billion beating analyst estimates by 3.2%. The company’s adjusted EPS of $3.40 surpassed analyst estimates of $3.19.

In the competitive arena of medical care facilities, Fresenius Medical Care AG (FMS) has lagged behind DVA, with 10.8% losses over the past 52 weeks and a 12.6% downtick on a six-month basis.

Wall Street analysts are cautious on DVA’s prospects. The stock has a consensus “Hold” rating from the eight analysts covering it, and the mean price target of $151 suggests a marginal potential upside from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Eli%20Lilly%20%26%20Co_%20by%20Tada%20Images%20via%20Shutterstock.jpg)