Dividend investors have had plenty to cheer about so far in 2026. Even as the broader S&P 500 ($SPX) has remained in negative territory to open the year, dividend-focused funds like the iShares Core Dividend Growth ETF (DGRO) have quietly done better than the market, returning more than 2% year-to-date (YTD) in early March as investors shifted toward names with steady income.

In a market where protecting capital matters as much as chasing gains, companies that keep lifting their payouts are making it clear how confident they are.

Qualcomm (QCOM) is now the latest chipmaker to join that group. On March 17, the San Diego-based semiconductor giant's board approved an increase in its quarterly cash dividend from $0.89 to $0.92 per share, a 3.4% raise, alongside a new $20 billion stock repurchase authorization that sits on top of an existing $2.1 billion buyback plan.

That move came after QCOM had already given up more than 36% of its 52-week high value, hit by a global memory supply crunch that has slowed smartphone production and weighed on near-term earnings guidance.

With QCOM trading at a discount and the company now stacking a dividend raise on top of the largest buyback authorization in its recent history, is this a value investor's dream setup, or does the stock's pain have more room to run before a real bottom forms? Let’s find out.

What Qualcomm’s Latest Results Say

Qualcomm sits at the center of mobile and connected computing, designing chips and licensing key wireless patents that power smartphones, cars, and a growing range of smart devices.

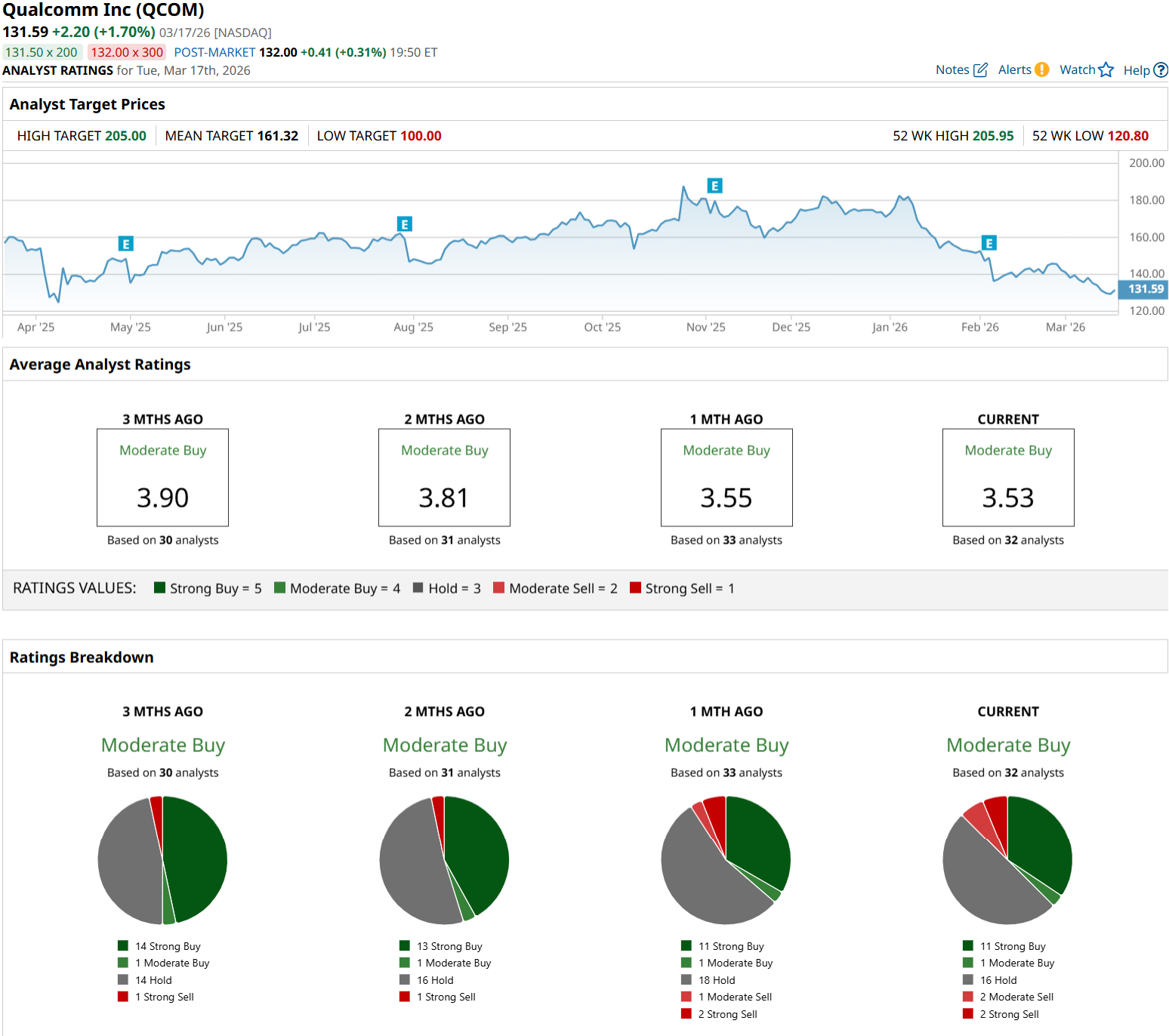

Over the past 52 weeks, that story has not impressed the market, with QCOM shares down about 17%, and YTD they are off another 23%.

That slide has left the stock looking relatively cheap. Qualcomm trades at about 15.44x forward earnings, below the sector average of 21.59x, which suggests investors are paying a lower multiple for the same $1 of expected profit.

The dividend, however, looks like a clear statement. Qualcomm yields about 3.56%, with the most recent quarterly dividend at $0.89 per share, a forward payout ratio near 35%, and a 23-year streak of annual increases that puts it well ahead of the tech sector’s average yield near 1.4%. Management is not just returning cash to shareholders; it is doing so from a solid financial base.

In Q4 CY2025, Qualcomm generated $12.25 billion in revenue, up 5% year-on-year (YoY) and slightly ahead of estimates, with adjusted EPS of $3.50, beating expectations by about 3%. Adjusted operating income was $4.41 billion for a 36% margin, again a bit above forecasts, and free cash flow margin held at a strong 36%, showing how much cash the business throws off to fund those dividends and buybacks.

Not every trend is favorable, though: operating margin slipped to 27.5% from 30.5% a year earlier, and guidance for Q1 CY2026 was cautious, with revenue around $10.6 billion and adjusted EPS at $2.55 at the midpoint, both below analyst expectations. Even so, inventory days fell sharply from 145 to 109, pointing to a better balance between supply and demand.

Qualcomm’s Growth Engines

Qualcomm’s new full-stack robotics architecture is built to run everything from household robots to full-size humanoids, bringing hardware, software, and compound AI together in one platform that can turn prototypes into real machines in the field. The Qualcomm Dragonwing IQ10 Series is the core of this effort, a high-performance, energy‑efficient robotics processor aimed at industrial autonomous mobile robots and advanced humanoids, acting as the “brain of the robot” and extending Qualcomm’s edge‑AI roadmap directly into large-scale robotics.

On the data center side, the early completion of the Alphawave Semi acquisition is meant to speed up Qualcomm’s move beyond client and edge devices into high-speed connectivity and compute inside the data center. Alphawave’s IP and team, now led inside Qualcomm by its co-founder and former CEO Tony Pialis, add high-speed SerDes and interconnect technology that is vital for AI‑heavy infrastructure.

In parallel, Qualcomm is using Adobe (ADBE) GenStudio to rebuild its content supply chain with generative AI, automating and scaling the creation, activation, and measurement of thousands of marketing assets each week so its sales and marketing teams can better support and monetize these new AI and data center offerings.

How Wall Street Sees QCOM Now

For the current quarter, March 2026, analysts expect earnings of $1.89 per share, down from $2.35 a year ago, which works out to a YoY drop of about 19.57%. The next quarter, June 2026, is pegged at $1.83 per share versus $2.29 last year, a 20.09% decline. For the full fiscal year ending September 2026, the Street is looking for EPS of $8.52 compared with $10.07 in the prior year, a 15.39% slide, before a small recovery to $8.72 in fiscal September 2027, just 2.35% growth off that lower base.

Bank of America recently reinstated coverage with an “Underperform” rating and a $145 price target, pointing to the potential loss of Apple business and rising competition as key risks that could hold back long‑term growth.

Even so, the wider analyst group is more positive. Across 32 analysts, the stock has a consensus “Moderate Buy” rating, and the average target price of $161.32 implies roughly 23% upside from recent levels.

Conclusion

For investors weighing Qualcomm’s 3.4% dividend hike, the setup looks like a cautious “yes, but know what you’re buying.” The company is clearly leaning into shareholder returns with a richer payout and a massive buyback while still throwing off enough cash to fund serious bets on robotics, data center connectivity, and AI‑driven marketing. All things put together, QCOM probably works best for dividend‑growth and value‑oriented tech investors who can stomach volatility and wait a couple of years for the growth engines to fully show up in the numbers.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)