/Salesforce%20Inc%20logo%20on%20building-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

Shares of Salesforce (CRM) recently caught investors’ attention after the cloud software giant unveiled a massive capital allocation move that could become a key catalyst for the stock. The company priced a $25 billion senior notes offering, its largest-ever debt issuance, with the proceeds earmarked for an accelerated share repurchase program aimed at returning capital to shareholders.

The announcement triggered a notable bounce in Salesforce stock, as investors interpreted the move as a signal that management sees the shares as undervalued and is willing to aggressively reduce the share count. Also, the debt-funded buyback ties into Salesforce’s broader $50 billion repurchase authorization, positioning the company to meaningfully boost earnings per share through financial engineering while reinforcing shareholder returns.

With Salesforce leaning into buybacks at scale, the $25 billion financing move could act as a powerful near-term catalyst, making the stock a wise investment.

About Salesforce Stock

Salesforce is a leading global provider of cloud-based customer relationship management software, headquartered in the iconic Salesforce Tower in San Francisco, California.

Salesforce’s market cap stands at $180.3 billion, reflecting its status as one of the most valuable enterprise software companies globally. With its comprehensive platform, innovative technology, and scalable business model, Salesforce remains at the forefront of enterprise digital transformation.

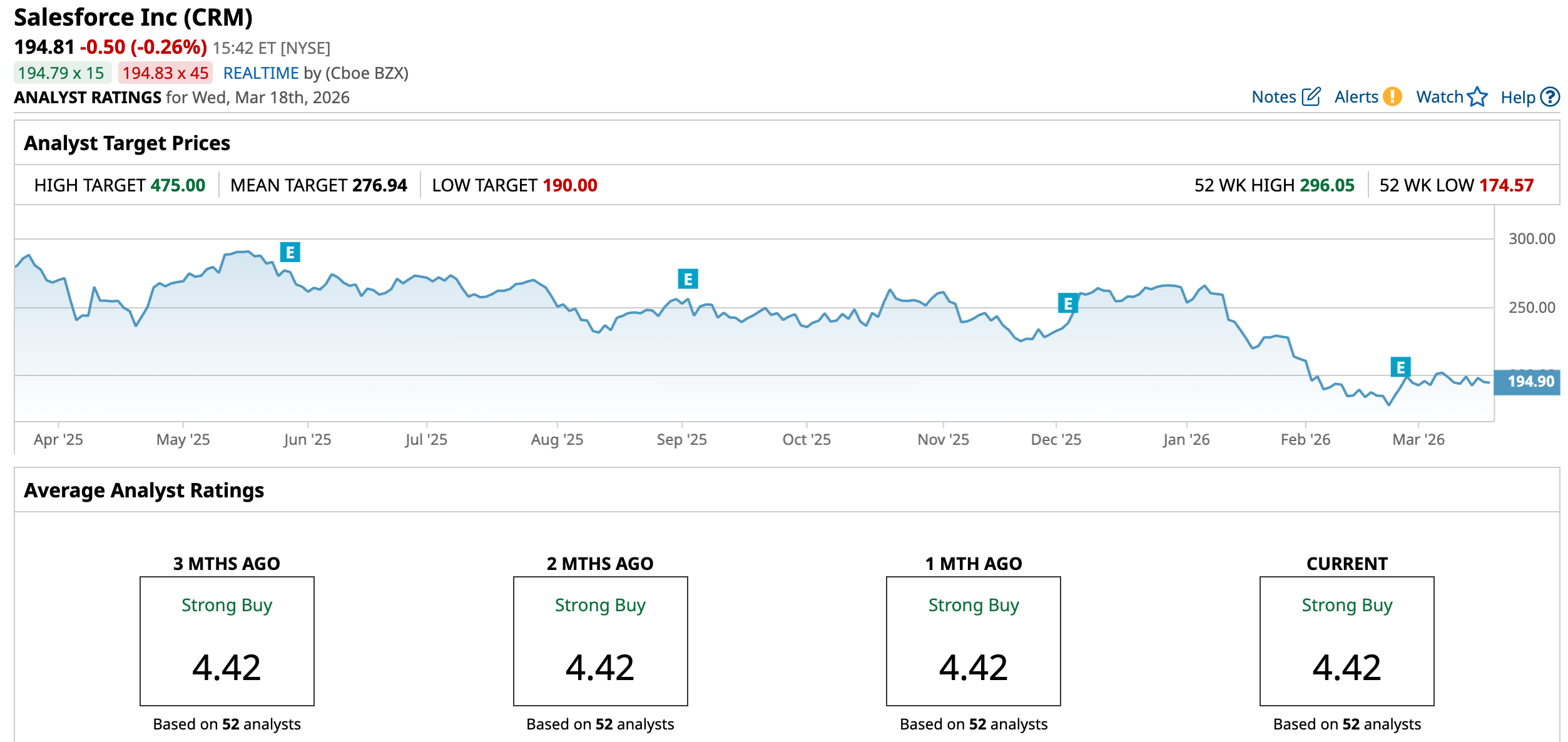

Shares of Salesforce have experienced a challenging stretch over the past year, with the stock underperforming many technology peers despite the company’s strong position in enterprise software. CRM shares have been under pressure in 2026, reflecting investor concerns around slowing enterprise spending and a broader rotation away from high-multiple software names.

Year-to-date (YTD), Salesforce stock has declined around 26.4%, extending a broader pullback. Over the past 52 weeks, the stock has fallen from a high of $296.05, reached in May 2025, to closing the last session at $195.31. The slump has largely been tied to cautious guidance and a perception that Salesforce’s growth has moderated compared with earlier cloud-computing boom years. The stock is down 30% over the past year.

However, sentiment toward the stock improved recently after Salesforce announced a $25 billion debt offering aimed at funding a major share repurchase program. The buyback financing news triggered a surge of 2.7% on Mar. 12, drawing renewed attention to the potential for financial engineering to support earnings per share and stabilize the share price, although it pulled back in the next session by 3.2% (Mar. 13).

CRM currently trades at a discount compared to the sector median and its own historical average at 20.45 times forward earnings.

Q4 Earnings Surpassed Projections

Salesforce released its fourth-quarter and full-year fiscal 2026 results on Feb. 25, delivering solid revenue growth and a sizable earnings beat, though the company’s forward outlook tempered some investor enthusiasm.

For the quarter ended January 2026, Salesforce reported revenue of about $11.2 billion, representing 12% year-over-year (YOY) growth. Profitability also improved meaningfully, with adjusted earnings per share (EPS) of $3.81, up from $2.78 in the fourth quarter of fiscal 2025 and comfortably exceeding Wall Street expectations. Its net income climbed to $1.9 billion from $1.7 billion a year earlier.

Salesforce also highlighted strong demand indicators during the quarter. Current remaining performance obligations reached $35.1 billion, up 16% YOY, while total remaining performance obligations rose to about $72.4 billion, up 14% YOY, reflecting a healthy pipeline of contracted future revenue across its cloud software platforms.

For the full fiscal year 2026, Salesforce delivered record revenue of $41.5 billion, representing a 10% growth compared with fiscal 2025. The company continued to generate strong cash flow and returned more than $14 billion to shareholders through buybacks and dividends, reinforcing its focus on capital returns alongside strategic investments.

However, management issued guidance that fell slightly short of expectations. Salesforce projected fiscal 2027 revenue in the range of $45.8 billion to $46.2 billion, while also guiding first-quarter adjusted EPS to about $3.11 to $3.13 with revenue expected between $11.03 billion and $11.08 billion.

Analysts predict EPS to remain flat in fiscal 2027, but surge by 12.4% annually to $10.90 in fiscal 2028.

What Do Analysts Expect for Salesforce Stock?

Recently, Salesforce received renewed support from Truist Securities, which reiterated its “Buy” rating and $280 price target after reports that the company may issue up to $25 billion in debt to fund share buybacks.

Also, last month, Salesforce received continued support from Cantor Fitzgerald, which reiterated its “Overweight” rating and $300 price target following the company’s fiscal 2026 results.

On the other hand, Salesforce received a price target cut from $300 to $250 from Stifel, although the firm maintained its “Buy” rating. The downgrade reflects weakness in core segments such as Tableau, Marketing Cloud, and Commerce Cloud, which offset strong traction in newer initiatives.

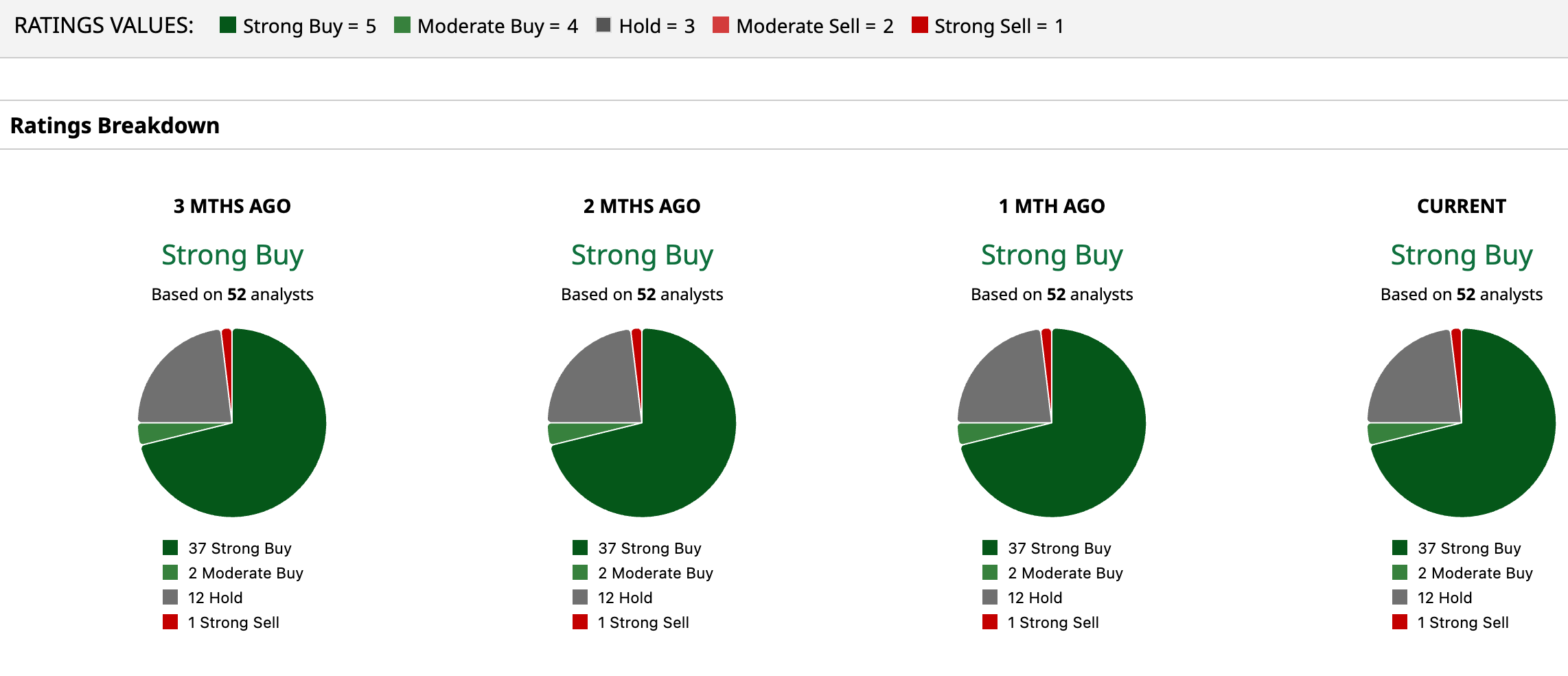

Wall Street is majorly bullish on CRM. Overall, CRM has a consensus “Strong Buy” rating. Of the 52 analysts covering the stock, 37 advise a “Strong Buy,” two suggest a “Moderate Buy,” and 12 analysts are on the sidelines, giving it a “Hold” rating, and one rate it as a “Strong Sell.”

The average analyst price target for CRM is $276.94, indicating a potential upside of 42.16%. The Street-high target price of $475 suggests that the stock could rally as much as 143.8%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Hands%20of%20robot%20and%20human%20touching%20on%20big%20data%20network%20connection%20by%20PopTika%20via%20Shutterstock.jpg)