In 2021, when copper was on its way to a new record peak at $4.8985 per pound on the nearby COMEX futures contract, Goldman Sachs analysts called the industrial metal “the new oil” because of its requirements in electric vehicles and other green energy initiatives.

After reaching a pandemic-inspired low of $2.0595 in March 2020, copper has made higher lows and higher highs, reaching a new record in May 2021 and March 2022.

The technical and fundamental factors in the copper market point to a continuation of the bullish trend. The current selloff could create a compelling buying opportunity for the metal as buying on price weakness has been the optimal approach over the past two years.

Interest rates and the dollar are pushing copper lower

On May 4, 2022, the US Federal Reserve will increase the short-term Fed Funds Rate by at least 50 basis points, pushing the rate to 0.75% to 1.00%. The central bank will likely start an aggressive program to reduce its swollen balance sheet, pushing rates higher further out along the yield curve. While the Fed controls short-term interest rates, the market determines medium and longer-term rates.

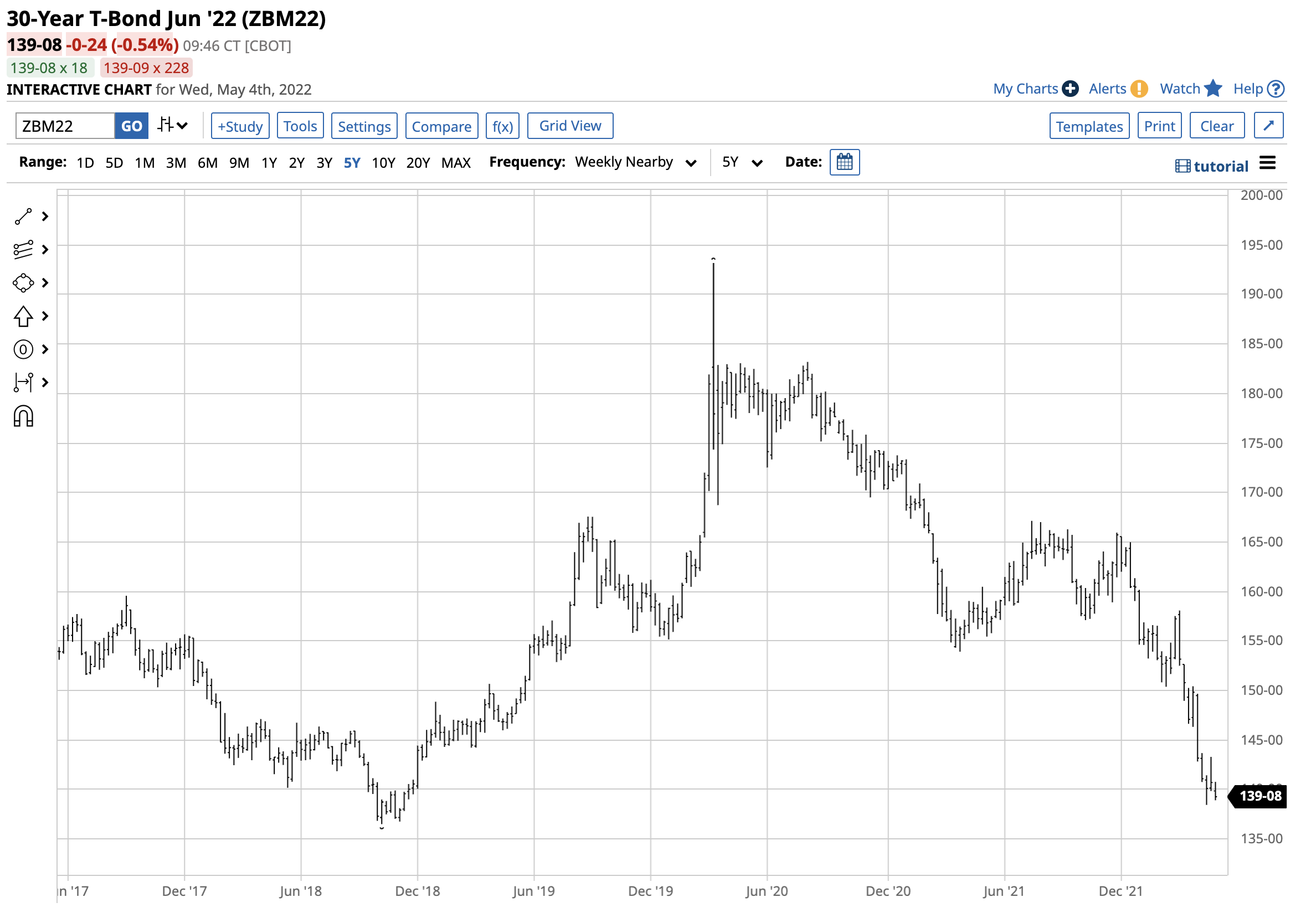

The chart shows the decline in the US 30-Year Treasury bond futures market that took the futures to a 138-14 low. Technical support for the long bond futures is at the October 2018 136-16 low. At the 139 level on May 4, the bonds are threatening to fall below that level to the lowest level since 2014.

Rising interest rates increase the cost of carrying inventories, which tends to weigh on raw material prices, and copper is no exception.

Meanwhile, rising US interest rates have supported a rally in the US dollar.

The US dollar index futures chart highlights the contract reached 103.95 last week, only 0.01 shy of the March 2020 peak. A move over that level will push the dollar to its highest level in two decades, since 2002. The dollar is the world’s reserve currency and the pricing mechanism for most commodities. A rising dollar tends to weigh on commodity prices, and copper is a leading asset class member.

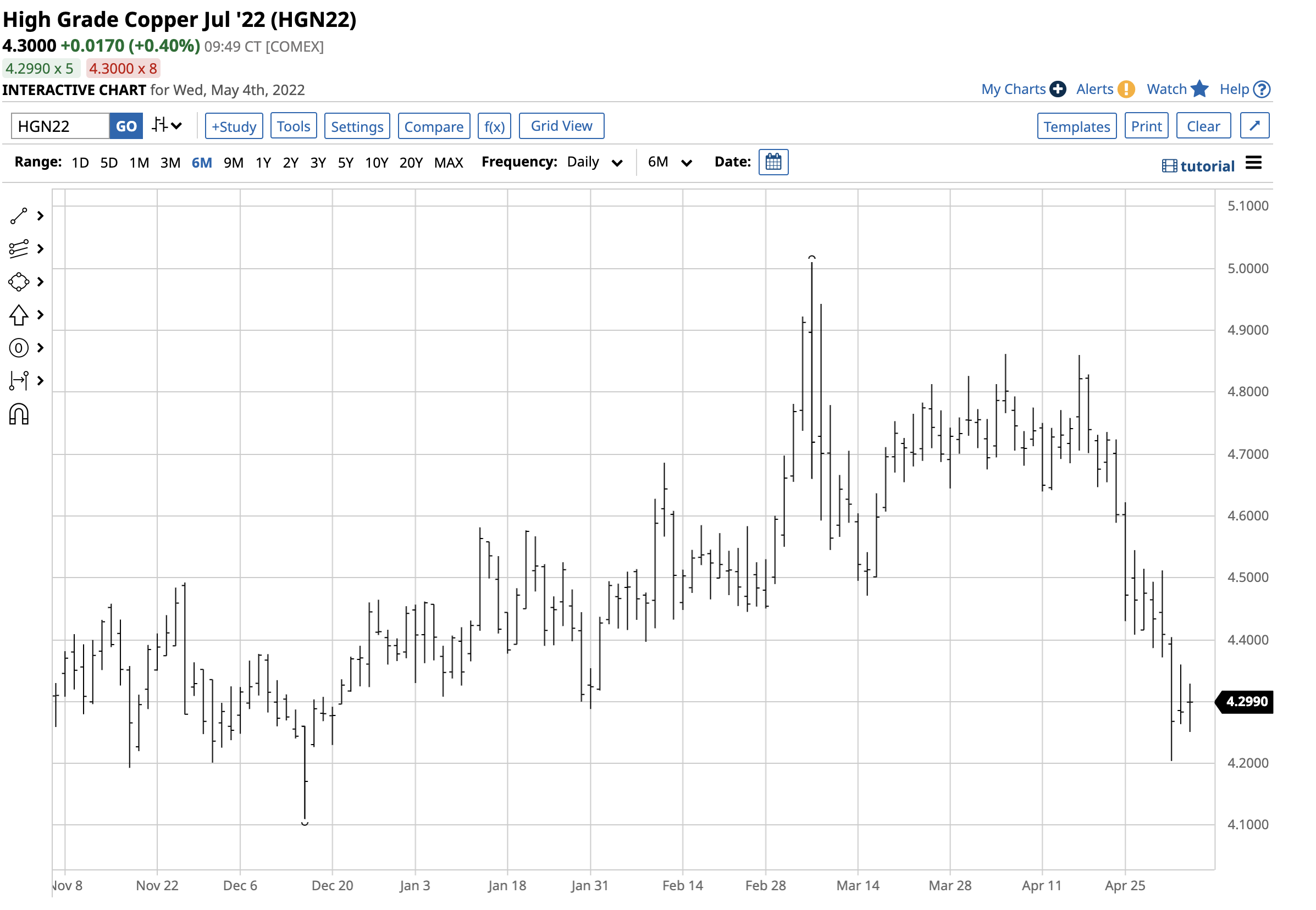

Nearby July COMEX copper futures rose to a record $5.01 per pound high on March 7. After correcting and consolidating between the $4.60 and $4.80 level from March 9 through April 22, copper futures fell through the bottom end of the range, reaching a low of $4.2040 on May 2. The prospects of rising interest rates and a strong Us currency pushed copper to a new low in 2022.

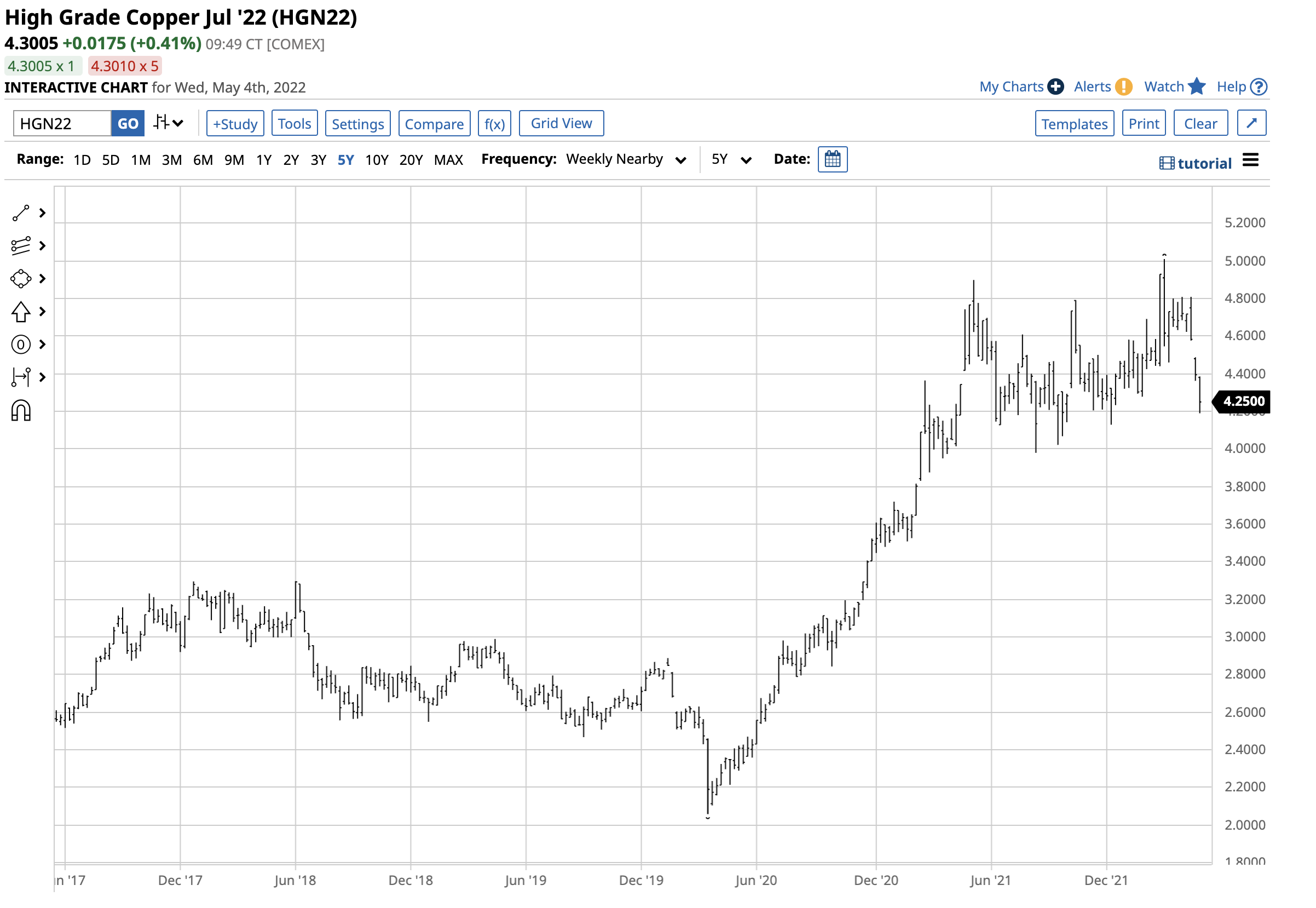

The pattern from May 2021 through August 2021 looks like the current price action

Copper’s recent price decline could be a repeat performance of the move from the May 2021 high to the August 2021 low.

The medium-term chart shows copper futures fell from $4.8985 in mid-May 2021 to a low of $3.98 per pound in August 2021 before climbing to another record peak in March 2022. The first technical support level stands at the mid-December $4.1290 per pound low.

If technical price history repeats, copper is now at a level where scale-down buying could be the optimal approach to the market.

Copper fundamentals point to a deficit over the coming years

Goldman Sachs called copper “the new oil” because EVs, wind turbines, and other environmentally friendly energy initiatives increase the demand side of the metal’s fundamental equation. The investment firm believes copper is on a path to reach $15,000 per ton by 2025. At that level, COMEX futures would exceed the $6.80 per pound level.

Goldman and many other analysts remain bullish on copper because of the rising demand from green energy initiatives. The war in Ukraine has pushed traditional energy prices to the highest level in years, making alternative and renewable energy projects all the timelier and more imperative. Crude oil is above $100 per barrel after eclipsing the $130 level in March. Natural gas at nearly $7.50 per MMBtu is at the highest price since 2008.

Three reasons why copper supplies will struggle to keep pace with the rising demand

While copper demand is booming, increasing supplies will be challenging. At least three factors point to a copper market deficit over the coming years:

- It takes eight to ten years to bring a new copper mine into production. The current demand level trend exceeds existing supplies.

- Traditional energy is a critical input in copper production. The highest oil, gas, and coal prices in years are pushing copper production costs substantially higher, putting upward pressure on prices.

- Addressing climate change limits new mine production, smelting, and refining. Cleaner production will cost a lot more than traditional copper output.

Meanwhile, the war in Ukraine is an inflation accelerant. The Fed’s response to rising inflation with higher US interest rates is taking a backseat to global price and supply distortions caused by Russia’s invasion, sanctions, and retaliation. Moreover, the Chinese-Russian “no-limits” alliance creates an ideological bifurcation with the US and Europe on the other side. Markets reflect the economic and geopolitical landscapes. Copper and other raw material markets face production and logistical issues given the dramatic shift caused by tensions between Russia/China and the US/Europe.

The bottom line is copper prices will likely find a bottom during the current correction and resume the upward price trajectory.

Watch the August 2021 low, a critical technical support level

Picking tops or bottoms in any market is challenging. Prices tend to rise fall to irrational, illogical, and unreasonable levels. Bull or bear market corrections can be nasty, shaking the confidence of even the most committed bull or bear.

The copper market crashed from $4.8985 in March 2021 to a low of $3.98 per pound in August 2021, where it found a bottom. While the 18.8% correction lasted only five months, it was ugly for those holding long positions. Copper only traded below $4 per pound on one trading day. The August 2021 low is the critical technical support level for the copper market, but that does not mean the red metal cannot reach a lower level before finding a bottom during the current correction.

I believe fundamentals will eventually take copper to new and higher highs on a path towards Goldman Sachs’ 2025 $15,000 per ton target. Moreover, the upside target could be low, as markets often rise well above forecast levels when the bulls drive prices higher.

I am a scale-down buyer of copper and copper mining shares from the current price levels, leaving plenty of room to add to long positions at illogical, irrational, and unreasonable levels. I never look to pick bottoms in any market. However, the fundamentals for the copper market and potential for higher highs are compelling for the coming years, justifying the risk of a buying program during the current selloff.

/Advanced%20Micro%20Devices%20Inc_%20office%20sign-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)

/The%20sign%20for%20Marvell%20Technology%20out%20front%20of%20a%20corporate%20office%20by%20Valeriya%20Zankovych%20via%20Shutterstock.jpg)