Marvell Technology (MRVL) could turn out to be a top-performing stock in 2026, driven by accelerating artificial intelligence (AI) led demand. The semiconductor company, known for its data infrastructure solutions, recently reported a solid fourth quarter, with revenue and profitability benefiting from strong demand in the data center end market. The company also issued an optimistic outlook for fiscal 2027, signaling that current growth trends are likely to continue.

Supporting Marvell’s product demand is the rising need for advanced data infrastructure. As data centers expand, the need for Marvell’s offerings — including interconnect, switching, and storage products — is expected to accelerate.

Another notable contributor to Marvell's growth has been its custom chip business. The segment experienced a significant ramp in fiscal 2026, with revenue roughly doubling year-over-year (YOY). Custom silicon is increasingly in demand as large tech companies seek specialized chips optimized for their own AI workloads and cloud platforms.

Despite strong growth momentum, Marvell’s valuation remains relatively reasonable given its long-term earnings potential. With accelerating demand and reasonable valuation, MRVL stock has room to run in 2026.

AI Demand to Accelerate Marvell’s Growth

Marvell Technology is positioned for significant growth as accelerating demand for AI infrastructure drives expansion across its data center portfolio. The company expects strong top-line and bottom-line performance in fiscal 2027, supported by solid booking momentum and increasing adoption of its networking and connectivity solutions within cloud and AI infrastructure.

For Q1, Marvell projects revenue of $2.4 billion, implying about 8% sequential growth at the midpoint of guidance. Importantly, the company anticipates similar sequential expansion in each subsequent quarter, suggesting steady acceleration as the fiscal year progresses.

If that trajectory holds, total revenue could exceed $11 billion in fiscal 2027, representing growth of more than 30% YOY. The primary catalyst for Marvell is the ongoing strength in its data center business.

Hyperscale cloud providers and large tech companies are increasing capital expenditures to support AI workloads, and that spending is translating into demand for Marvell’s solutions. Management expects data center revenue to grow roughly 40% YOY in fiscal 2027, supported by strong performance across several key product categories.

One of the fastest-growing areas is Marvell’s interconnect segment. Revenue from this business is projected to grow by more than 50% YOY. Meanwhile, the company’s communications and other end markets are expected to grow at a more modest pace of around 10%.

Looking beyond 2027, Marvell sees further expansion ahead. Even if cloud infrastructure spending moderates slightly, the company expects demand driven by AI workloads to remain strong. Data center revenue is likely to continue growing at a healthy rate, with the interconnect business still outpacing broader cloud infrastructure growth. At the same time, Marvell’s custom silicon segment is expected to at least double YOY, while its Ethernet switching portfolio continues to scale.

Strategic acquisitions are also expected to contribute to Marvell’s growth trajectory. Businesses such as Celestial AI and XConn Technologies could collectively generate around $250 million in revenue by fiscal 2028, according to CEO Matthew Murphy.

Overall, data center revenue is likely to compound at well above 40% for three consecutive years. At the same time, Marvell's total revenue could reach $15 billion in fiscal 2028, representing roughly 40% annual growth and potentially driving adjusted EPS to well above $5, which is higher than the analyst consensus estimate of $4.38.

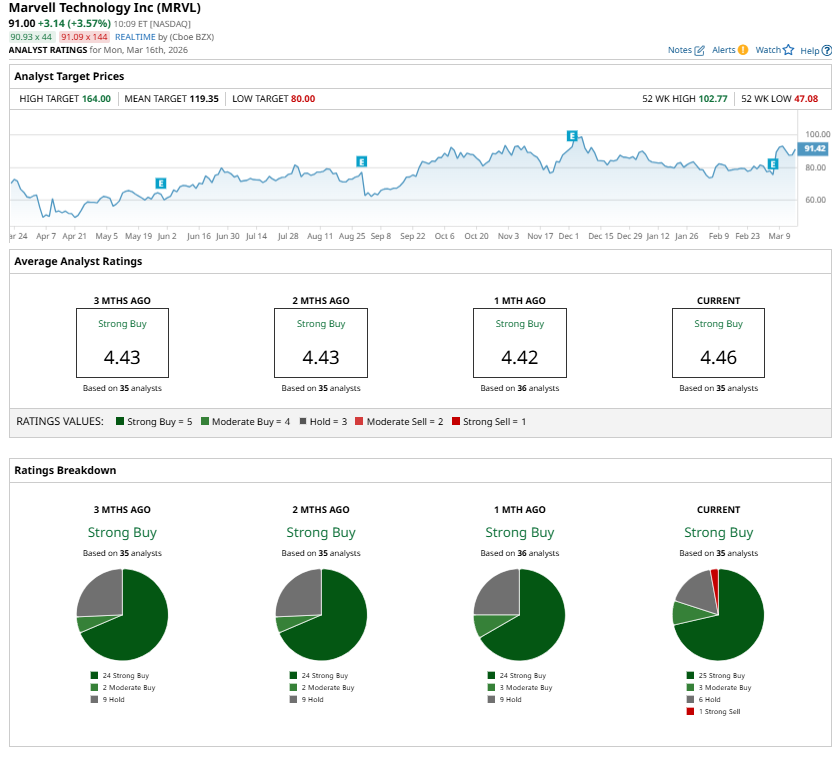

Analysts Are Upbeat About Marvell Stock

The strong demand for Marvell’s data center products, the expected acceleration in its top-line growth rate, and solid bottom-line growth could drive MRVL stock higher.

Wall Street analysts collectively assign MRVL stock a “Strong Buy” consensus rating. Valuation metrics also appear reasonable given the company’s expected growth. Marvell shares currently trade at roughly 29 times forward earnings, which is still attractive given the company’s projected earnings momentum.

Consensus projections indicate that Marvell’s earnings could surge by about 40% in fiscal 2027. Looking further out, growth is expected to remain robust, with an additional 45% increase in EPS estimated for fiscal 2027.

Overall, strong demand and an attractive valuation indicate that MRVL stock has room to run in 2026 and beyond.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)