/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

Micron (MU) continues to garner positive sentiment ahead of its Q2 earnings next week. Brokerage firm GF Securities just upped its price target on the stock to $571. In a note to clients, analyst Jeff Pu reasoned “We now forecast DRAM contract prices to rise by 100% in 1Q26, followed by >30% QoQ in 2Q26 with further upside given current asking prices in 50-60% range. For Micron, we forecast FY2Q26 revenue to be $23B with [a] gross margin of 77%. Looking ahead, we expect 3Q26 revenue guidance to be $29B and a margin further [to] grow to 83%. In terms of HBM development, we see Micron [sic having] secured its HBM4 order (likely ~10Gbps version) with [a] small patch starting [in] March.”

Not just that, Pu reckons that the demand-supply mismatch scenario will continue to prevail until at least 2027, stating, “Meanwhile, AI-related demand is expected to account for 75+% DRAM demand in 2027, and the short supply may last into 2H27. As [a] result, [the] memory maker’s visibility has greatly improved, and we see 3-5 years [long-term agreements] are now being negotiated.”

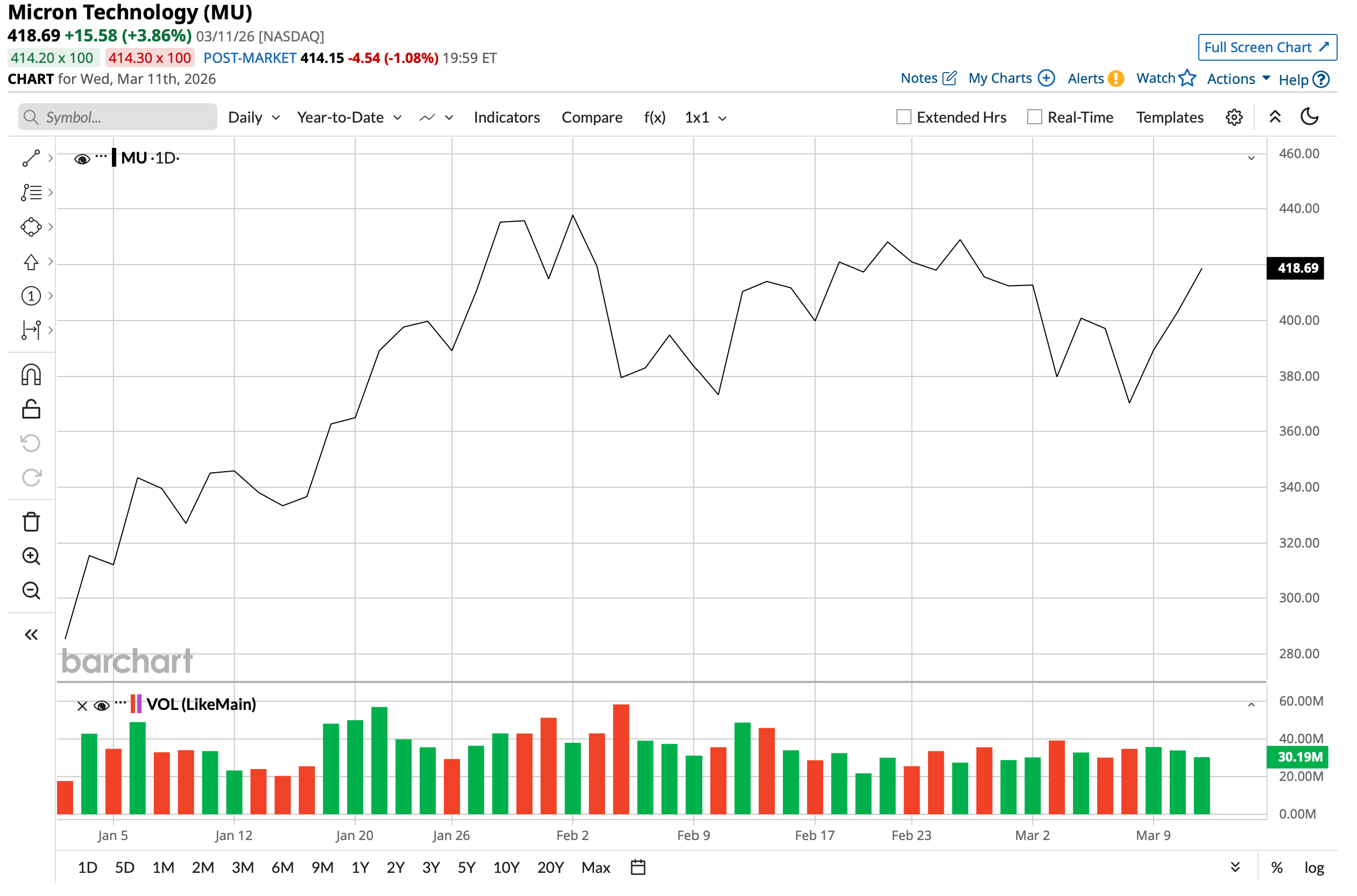

While these are solid reasons to load up on MU stock, shares are already up 42% for the year. Is there any room left for Micron to run?

Why Micron Is the Place to Be in Memory

If you read my latest piece, you can figure out where I am going with this. In short, Micron is still a “Buy” at current levels, and it is not too late. Its presence across the whole memory ecosystem, from High Bandwidth Memory (HBM) to NAND, and its U.S. identity will continue to remain the primary drivers for the stock.

Notably, Micron has already completely sold out its entire 2026 HBM supply, including its upcoming HBM4, under fixed-price, multi-year contracts. And with hyperscalers and the U.S. government actively looking to de-risk semiconductor supply chains away from Taiwan, China, and South Korea, Micron is uniquely positioned.

Additionally, other than its New York and Idaho plants, Micron is expanding its manufacturing base in other geographies as well. the new HBM advanced packaging facility in Singapore is expected to begin contributing meaningful additional supply starting in calendar year 2027. Complementing this, the planned assembly and test plant in India will further expand overall capacity and strengthen the company’s footprint in high-growth regions for memory production.

Finally, Micron's 256GB SOCAMM2 is expected to bring a new area of growth for the company in the realm of AI infrastructure. Micron recently began shipping customer samples of it, which is built on the industry-first monolithic 32Gb LPDDR5X die. This module represents a massive leap over previous generations by offering one third more capacity than its predecessor.

When stacked against conventional RDIMM (Registered Dual In-line Memory Module) peers, the SOCAMM2 truly shines by consuming only a third of the power and occupying just a third of the physical footprint. This translates directly to exceptional total cost of ownership improvements for hyperscalers. Furthermore, the modular design easily supports advanced liquid cooling architectures while delivering a 2.3 times faster time to first token for long context large language model inference. Ultimately, this high-density, highly efficient component allows data centers to maximize rack performance and scale their AI capabilities without blowing out their thermal budgets.

Top-Rated Financials

Micron has produced strong results over the past decade, with revenue and earnings compounding at annual rates of 10.95% and 18.93%, respectively. The company has also delivered earnings beats in each of the last nine quarters.

The fiscal Q1 2026 results (ended November 2025) were particularly robust, with both revenue and earnings coming in well above expectations. Revenue rose 56.6% year over year to $13.64 billion, surpassing consensus by roughly $760 million. Growth was led by the cloud memory and mobile segments, which reported $5.3 billion (up 103.8%) and $4.3 billion (up 65.4%), respectively. The data center business lagged, increasing only 4.3% to $2.4 billion.

Earnings per share surged 167% to $4.78, comfortably beating the $3.96 consensus. This marked the eighth consecutive quarter in which Micron more than doubled year-over-year earnings.

Cash generation was equally impressive. Operating cash flow jumped to $8.4 billion from $3.2 billion in the prior-year quarter. The company ended the period with $9.7 billion in cash and equivalents, far exceeding short-term debt of $569 million.

Looking ahead, management guided fiscal Q2 2026 revenue to a range of $18.3 billion to $19.1 billion, with EPS expected between $8.22 and $8.62. The midpoint implies 132.3% revenue growth and 440% EPS growth year over year.

Valuation metrics remain reasonable in light of the growth outlook. A forward price-earnings ratio of 11.52x and price-cash flow ratio of 9.53x sit below sector medians of 21.46x and 17.13x, while a forward price-sales ratio of 5.80x is only moderately above the sector median of 3.05x. Projected forward revenue growth of 60.46% and EPS growth of 305.39% significantly outpace sector averages of 10.33% and 15.21%, supporting the current premium.

Analyst Opinions on MU Stock

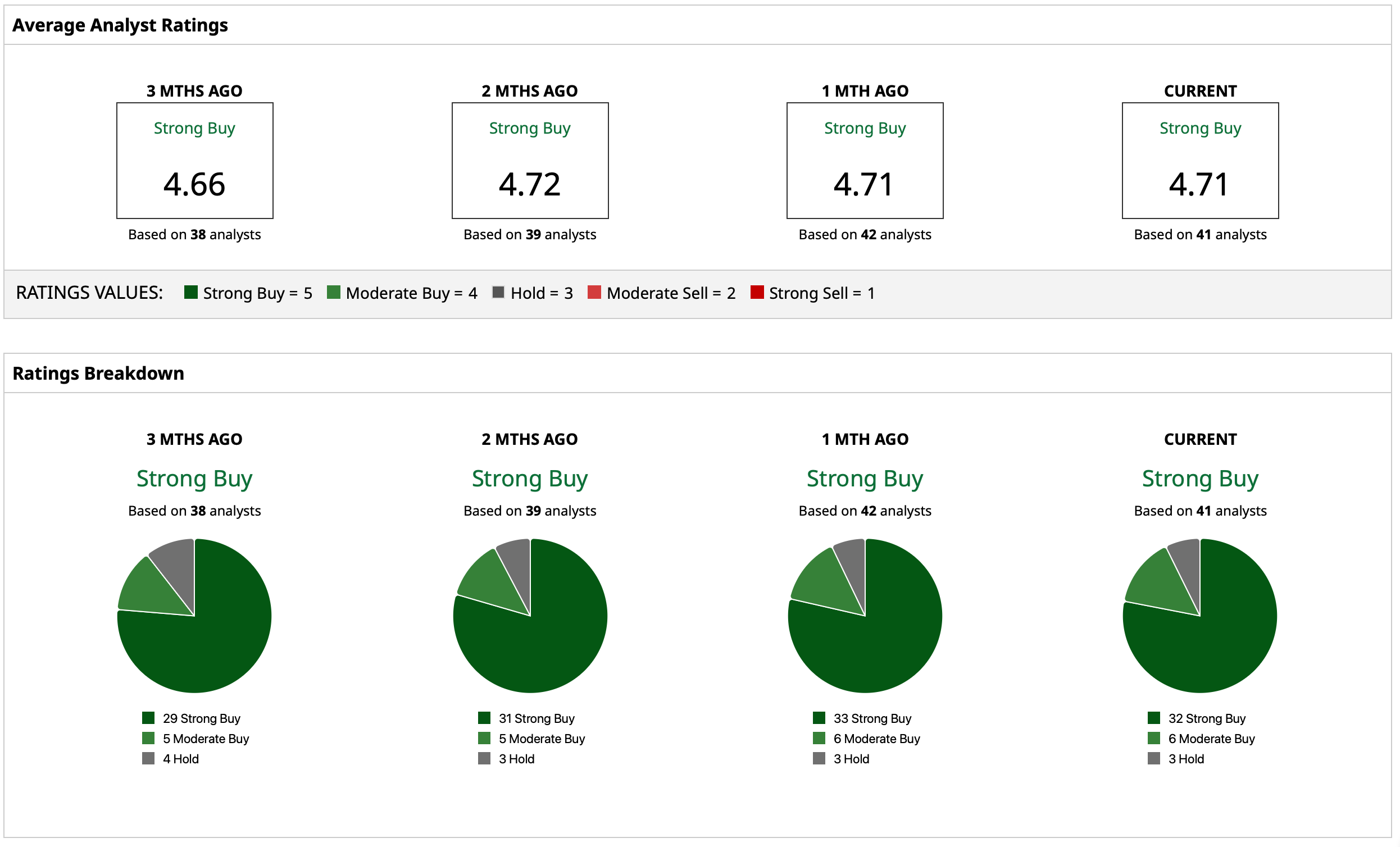

Analysts have deemed MU stock to be a “Strong Buy,” with a mean target price that has already been surpassed. However, the high target price of $571 from GF Securities denotes upside potential of about 34% from current levels. Out of 41 analysts covering the stock, 32 have a “Strong Buy” rating, six have a “Moderate Buy” rating, and three have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)