/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Intel (INTC) stock rallied significantly in 2025, rising about 84%. Moreover, the momentum in INTC stock has sustained in 2026. Even though Intel stock pulled back a bit following weaker-than-expected Q1 projections, it is still up about 25% year-to-date.

With Intel benefiting from AI data center tailwinds, the company could deliver steady growth in 2026. However, to double in 2026, Intel stock should hit $73.8, which implies about 54% upside from its recent closing price of $47.98.

Factors Supporting the Rally in INTC Stock

Intel’s growth trajectory remains solid, led by AI-driven demand. As AI applications spread from large cloud data centers to enterprise systems and eventually personal devices, demand for processors and specialized chips is rising sharply. This trend plays into the strengths of Intel, which remains one of the few semiconductor companies with capabilities spanning chip design, manufacturing, system integration, and advanced packaging.

Intel is also repositioning its product portfolio. While the company continues to defend its personal computer franchise, it is also pushing aggressively into high-growth segments such as data-center processors, AI accelerators, and custom silicon. At the same time, Intel is expanding its semiconductor manufacturing footprint in the U.S., which could make it an increasingly valuable partner for governments and technology firms seeking secure chip supply chains.

While the beginning of 2026 may be somewhat uneven, the broader trajectory appears promising. Management has indicated that supply constraints could weigh on first-quarter results, particularly within the company’s client computing group. However, these pressures are expected to ease starting in the second quarter, with conditions gradually improving throughout the year. As supply normalizes, Intel could see stronger revenue momentum.

Where sentiment is turning more positive is in Intel’s data center and AI (DCAI) business. Enterprises and cloud providers are accelerating investment in server infrastructure. That surge in computing demand is translating into higher spending on processors and specialized chips, segments where Intel already has deep relationships with enterprise customers.

The DCAI segment generated $4.7 billion in revenue in the fourth quarter, representing a 15% sequential increase. Management indicated that revenue could have been meaningfully higher if supply had been sufficient to meet demand. While the industry continues to benefit from more power-efficient CPUs driving a server refresh cycle, the broader trend points to the growing importance of CPUs within hyperscale and enterprise AI data centers as inference-driven AI workloads expand.

Intel is also benefiting from rising demand for networking hardware, driven by the global build-out of AI infrastructure. The company’s custom Application-Specific Integrated Circuits (ASICs) business grew more than 50% in 2025 and increased 26% sequentially, reaching an annualized revenue run rate of $1 billion plus in the fourth quarter. This momentum is likely to sustain in the coming quarters.

Another catalyst is its large x86 ecosystem. The architecture has a massive global installed base of PCs and enterprise systems, giving Intel a large platform from which to introduce AI-enabled hardware.

Overall, these trends suggest that Intel is in a period of transformation. By aligning its manufacturing scale, product strategy, and technological investments with the expanding AI economy, the company is positioning itself to deliver solid growth.

Will Intel Stock Double in 2026?

Intel stock has staged a strong rally over the past year, driven by the company’s ongoing efforts to turn around its business and position itself for growth in the rapidly expanding AI market. As Intel reshapes its product portfolio and focuses on opportunities tied to AI and advanced computing, its long-term prospects remain constructive. However, much of this optimism appears to be reflected in INTC’s current share price following the recent surge.

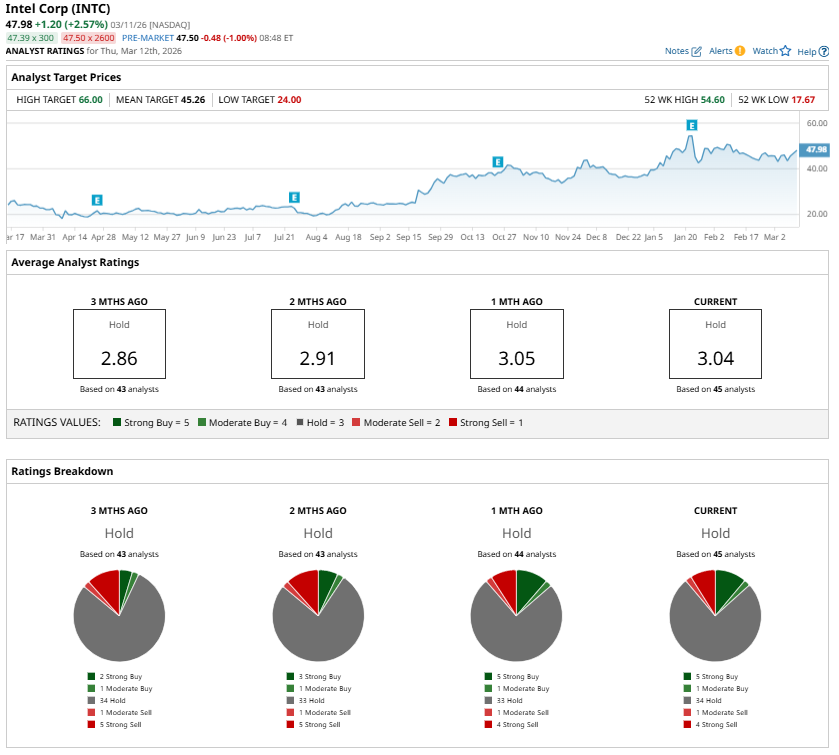

Wall Street analysts currently maintain a consensus “Hold” rating on Intel shares. Notably, the stock is already trading in line with the average analyst price target. Moreover, the highest price target for INTC stock is $66 per share, representing roughly 38% upside from its recent closing price.

In summary, Intel could still deliver gains in 2026 and potentially outperform the broader market. But the expectation for the stock to double is aggressive.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)