/Computer%20memory%20closeup%20by%20Nor%20Gal%20via%20Shutterstock.jpg)

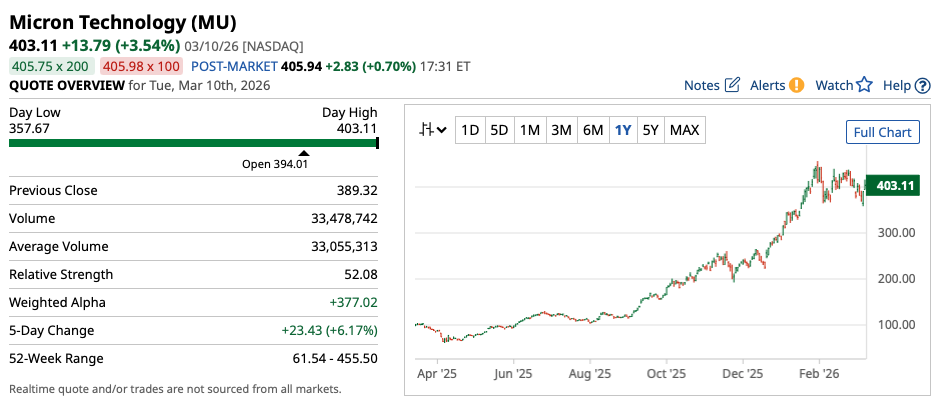

Micron (MU) is among the leading memory-makers in the market. As such, this stock's incredible surge over the past few months has started to catch the attention of many investors, for good reason.

I've touched on Micron's incredible rise a number of times in the past. However, with recent volatility now reshaping expectations around how this stock may perform moving forward (given increased attention around this name), I think it's fair to say that most market participants now find them on one side of this trade or another.

Let's dive into some interesting recent analysis put forward by analysts at BP Paribas, who are still bullish on MU stock despite the incredible four-fold surge we've seen thus far this year. Here's the bull case behind why this particular company could have much further upside potential from here.

Why the Bullish Outlook on Micron?

Micron's past surge has a lot to do with increasingly beneficial supply and demand dynamics for memory makers. An integral piece of the artficial intelligence (AI) supply chain, computing providers need an incredible amount of memory to run their central processing units (CPUs) and graphics processing units (GPUs), meaning that surging chip demand has led to outsized growth in memory demand, which many top suppliers like Micron have struggled to keep pace with.

Thus, as chip demand continues to soar, and investors look for the most profitable angles from which to play the surging demand we're seeing unfold, memory-makers like Micron should be well-positioned to continue growing their top and bottom line numbers at a considerable rate.

With BNP analysts noting that NAND prices are estimated to “increase 55% Q/Q, followed by 5% Q/Q increase in CQ2 predominantly driven by supply-side dynamics as NAND suppliers continue to shift capacity to enterprise storage products while remaining prudent on capacity additions.” That's a big deal.

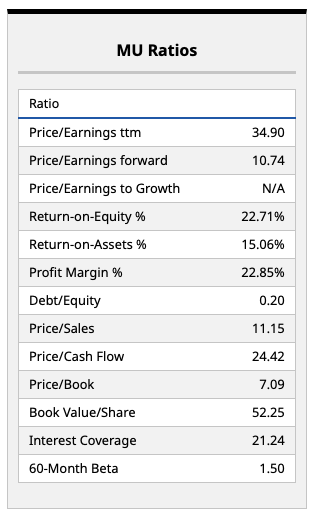

What that ultimately means for Micron moving forward is that market participants are likely to price in higher margins over time. And for a company with a profit margin that's approaching 23%, that's going to be a good thing for investors.

Personally, I'm paying closer attention to Micron's other key ratios, such as its return on equity and return on assets, both of which are well into the double-digits. Those signify this is a company with a solid operating model and significant cash flow, which can fund further growth as Micron reinvests in its core business.

On that note, a price-to-cash-flow ratio of less than 25x signifies a free cash flow yield of a little more than 4% for investors. Thus, even those who have an income mandate within their own portfolios may be able to justify holding a basket of high-quality names like Micron with this kind of free cash flow yield, even as the stock has absolutely taken off this year.

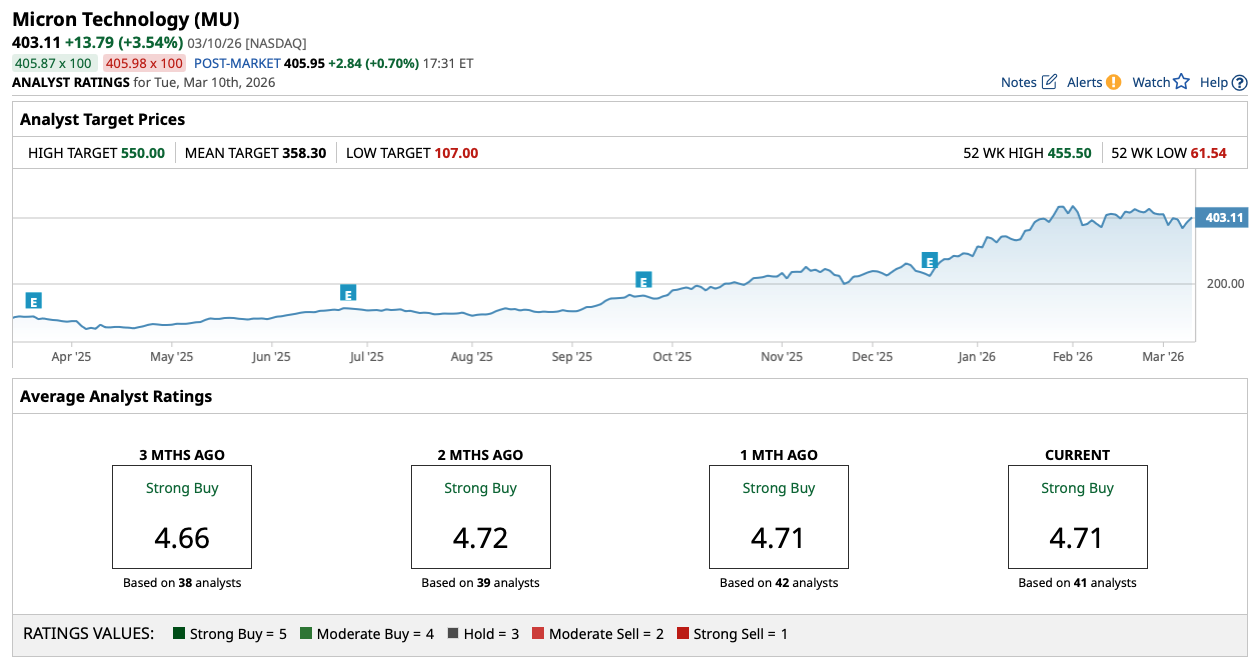

What Do Wall Street Analysts Think of Micron?

The interesting news for investors looking at Micron today is that Wall Street analysts do appear to be behind the curve on this particular name. With a current consensus price target of a little under $360 per share, there's currently around 10% downside baked into MU stock, taking this price target at face value.

That said, as more analysts like BNP upgrade this stock and raise price targets (more such price-target hikes are likely to come, in my view), this is a stock that could have material upside over the next year as analysts and market participants catch on.

We'll see, and it does appear that we're still in the early innings of this memory shortage. But if we do see the kind of demand BNP analysts suggest is on the way, this is a stock that could provide excellent value at current levels.

On the date of publication, Chris MacDonald did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)