The crypto industry is back in the headlines, and this time, politics is once again driving the momentum. A fresh clash between Washington, Wall Street, and the crypto industry has reignited the debate around digital asset regulation, and the market is already reacting.

At the center of the fight is the CLARITY Act, a proposal meant to finally bring clear rules to the digital asset industry after years in a regulatory gray zone. Supporters say the framework could unlock innovation and broader adoption. But progress has stalled as major banks push back against stablecoins offering yield-like rewards, warning that such incentives could pull deposits away from traditional banking systems.

Just as the debate appeared stuck, Donald Trump stepped in publicly, urging banks to “make a good deal” with the crypto industry and move the legislation forward. His remarks signaled strong political backing for the sector and quickly sparked a rally across the crypto market.

The market loved the political boost, Bitcoin (BTCUSD) jumped 7.78% within hours to around $73,000, while Ethereum (ETHUSD) surged 9.27%. The rally spilled over into crypto stocks as well, with Coinbase Global (COIN) soaring 14.57% and several bitcoin miners rebounding after months of pressure.

With politics tilting in crypto’s favor and legislation still hanging in the balance, is COIN stock still worth buying after this rally?

About Coinbase Stock

Founded in 2012, Coinbase is a Delaware-based crypto giant, boasting a $54.3 billion market cap. As one of the largest exchanges globally, it serves both retail and institutional investors. Beyond trading, it is expanding through global licenses, acquisitions, and innovations like stablecoin payments, crypto cards, and subscriptions, positioning itself as a key architect in the evolution of digital finance.

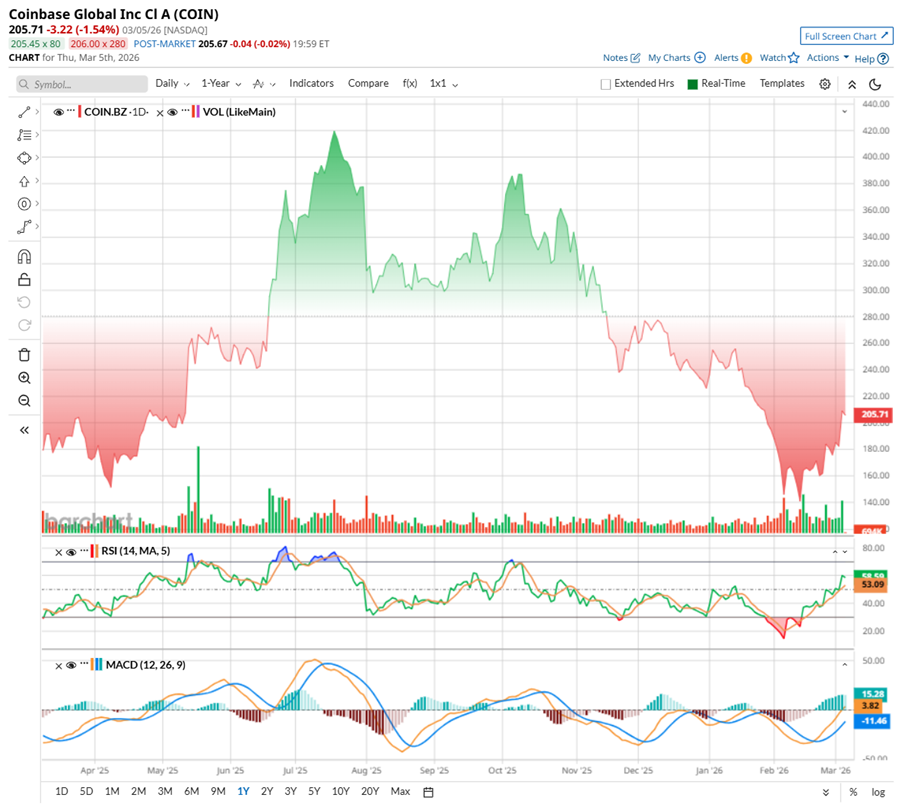

Coinbase’s shares have mostly moved with the ups and downs of the crypto market. When optimism returned and Bitcoin rallied, the stock rode that wave, climbing to a July high of $444.64. But the momentum did not last long. As digital assets cooled off, COIN gave back much of those gains, now down 55.6% from its peak. The pressure has been visible in recent months. Over the past six months, the stock is down about 34.06%, including a 26.89% drop in just the last three months.

Still, the latest moves suggest the story may be shifting again. Over the past month, COIN has jumped nearly 19.43%, including a 12.14% gain in the last five trading sessions.

The recent rebound is now showing up in COIN’s technical signals as well. Trading volume has begun to pick up, which is often one of the first signs that investors are slowly returning to a stock after a rough stretch. Momentum indicators are also sending more encouraging signals. The 14-day Relative Strength Index (RSI), which had slipped into oversold territory back in February, has climbed back to 54.41. That suggests the heavy selling pressure seen earlier this year is starting to cool.

Plus, the MACD line has crossed above its signal line after staying below it for days, a shift that often hints at strengthening momentum. At the same time, the histogram has turned positive, suggesting buying pressure is gradually returning, and the stock’s upward momentum may continue building.

A Closer Look at Coinbase's Mixed Q4 Numbers

When Coinbase Global reported its Q4 2025 results on Feb. 12, the crypto market was already shaky. Prices were swinging, investor sentiment was mixed, and the numbers reflected that pressure.

Total revenue came in at $1.78 billion, down 22% year-over-year (YOY) but roughly in line with Wall Street’s expectations. Profit took a bigger hit. Non-GAAP EPS landed at $0.66, a sharp fall from $3.37 a year ago, largely because trading activity cooled and transaction fees shrank. Net revenue slipped 22.2% YOY to $1.71 billion.

The real drag came from transaction revenue, which dropped 37% to $982.7 million as trading volumes slowed. But Coinbase still had a few bright spots. Subscription and services revenue climbed 13.5% to $727.4 million, helped by stronger stablecoin income and steady demand for recurring products. Adjusted EBITDA stayed in positive territory, though it was clearly lighter than last year’s blockbuster levels.

Zoom out to the full year, and total trading volume grew to $5.23 trillion, marking a sharp 156% annual jump, showing how active the exchange became whenever crypto markets heated up. In Q4 alone, consumer spot trading totaled $56 billion, slipping 6% from the prior quarter as retail traders cooled off. Institutional spot trading was larger at $215 billion, though that figure also dipped 13% sequentially as big players pulled back a bit.

Importantly, Coinbase’s balance sheet showcased resilience. The company ended the quarter with $11.28 billion in cash and a healthy operating cash flow. Its premium membership product, Coinbase One, also kept gaining traction, reaching nearly one million subscribers. And the company quietly continued building its crypto holdings, adding about $39 million worth of Bitcoin through regular weekly purchases.

Looking ahead, management estimates Q1 2026 subscription and services revenue to land between $550 million and $630 million. Expenses remain elevated, with R&D and G&A projected around $925 million to $975 million, while sales and marketing could reach $215 million to $315 million. Even so, leadership says the bigger story is improving market share, rising engagement, growth of the Base network, and expanding opportunities overseas.

Analysts monitoring Coinbase expect the company’s bottom line to slip by 70.6% YOY to $0.57 per share in Q1, with revenue anticipated to be around $1.59 billion. Looking ahead, adjusted EPS for fiscal 2026 is projected to be around $3.32, down 17.6% YOY. But the tide could turn quickly by the next fiscal year. Adjusted EPS anticipated to surge 31.6% annually to $4.37 in fiscal 2027.

What Do Analysts Expect for Coinbase Stock?

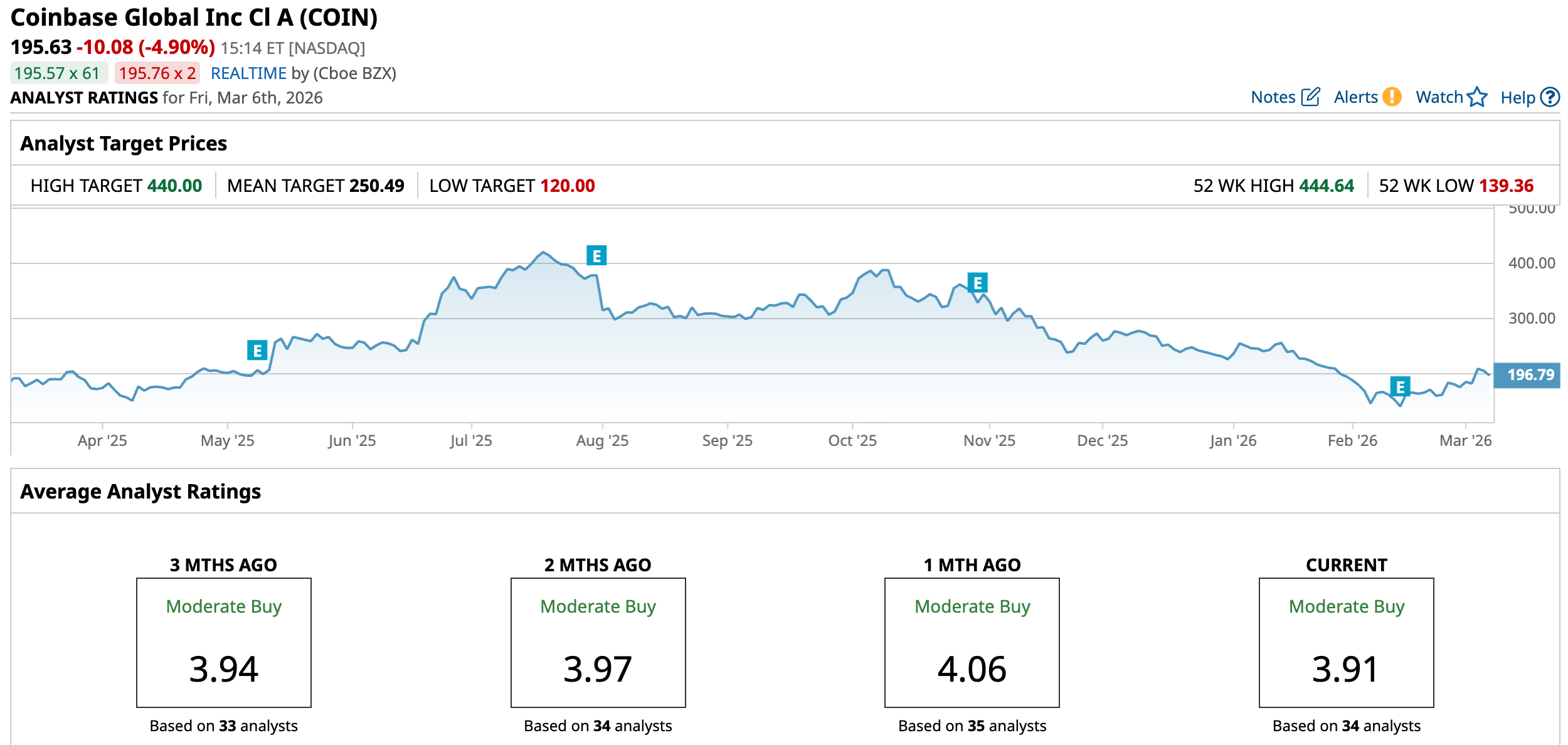

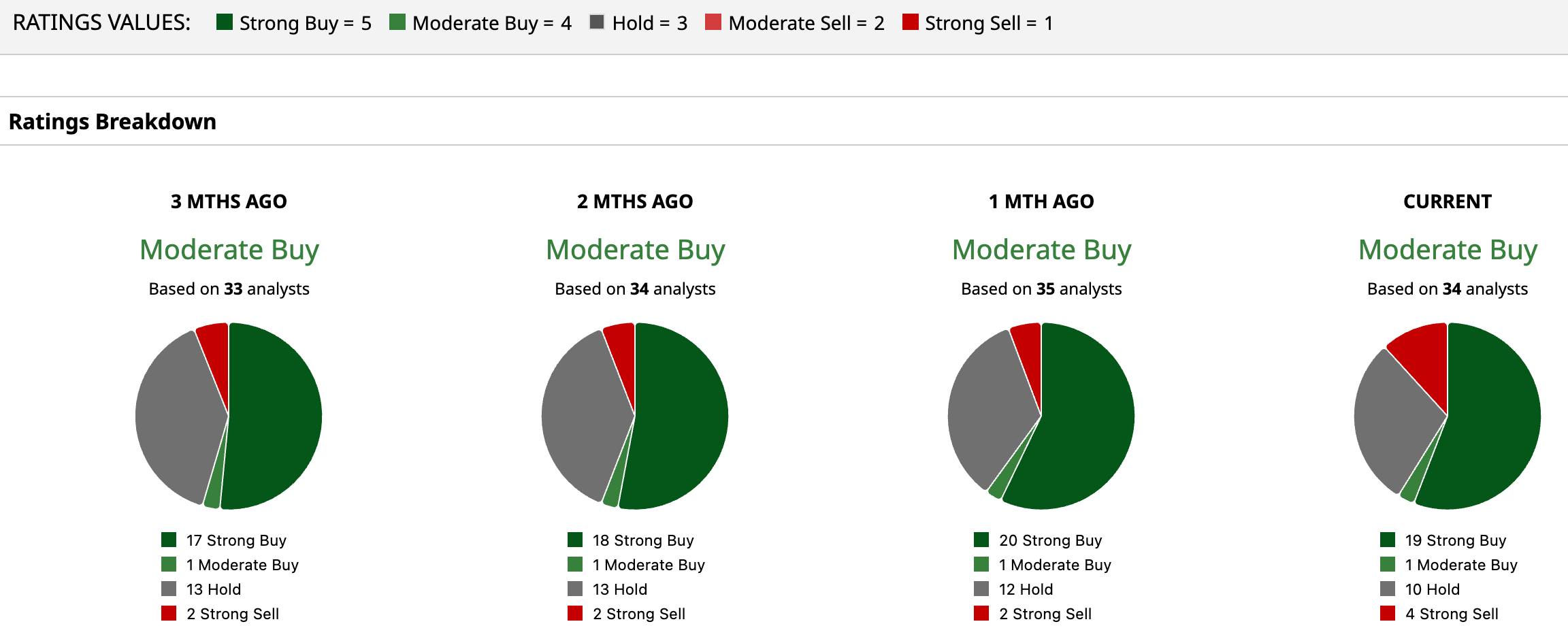

Wall Street has not exactly turned bearish on Coinbase, but it has turned more cautious. The stock is having a “Moderate Buy” consensus rating overall. Out of 34 analysts, 19 now rate it a “Strong Buy,” one calls it a “Moderate Buy.” 10 analysts are playing it safe with a “Hold,” and the remaining four are outright bearish with a “Strong Sell” rating.

The mean price target of $250.49 implies rebound potential of 28%. Meanwhile, the Street’s highest projection of $440 suggests COIN stock could rise as much as 124.9% from here.

Final Thoughts on COIN Stock

The latest support from Donald Trump has once again thrown crypto into the spotlight, giving the sector a short-term sentiment boost, but also reminding investors how closely politics and digital assets are now intertwined. Headlines can move markets quickly, but long-term value will still depend on regulation, adoption, and sustained user activity.

Beyond the political noise, Coinbase Global continues evolving from a pure trading platform into a broader financial marketplace, with multiple products now generating significant recurring revenue. That diversification could help smooth out the volatility tied to crypto cycles. Institutional confidence also appears to be holding up, and Coinbase is expanding into 24/5 commission-free stock and ETF trading.

Still, between regulatory uncertainty and the ever-swinging mood of digital assets, COIN is not exactly a sleepy investment. For patient investors comfortable with sharp ups and downs, the stock may offer long-term potential, but it is likely to remain a bumpy ride.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)