/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

QUALCOMM (QCOM) built its reputation over the years supplying the chips and connectivity that power modern devices. As artificial intelligence (AI) and 5G reshaped the tech landscape, Qualcomm stood at the center of that shift, benefiting from demand for faster, smarter, and more efficient computing.

Yet 2026 has been far less forgiving. Semiconductor stocks have gone through a broad correction, and QCOM has not been spared. The stock is down 19.2% this year, wiping out much of last year’s progress and drifting back toward levels seen several years ago.

Weak Q2 guidance in early February, linked to memory shortages and slower smartphone production, added fresh doubts. At the same time, geopolitical tensions and a wider tech sell-off have pressured valuations and crushed the stock’s earlier uptrend.

With sentiment fragile and the chart showing clear strain, is this a buy-the-dip opportunity for investors, or a warning sign to remain patient?

About QUALCOMM Stock

San Diego, California-based QUALCOMM is a fabless semiconductor company with a market cap of $150.5 billion. It shines through its Qualcomm CDMA Technologies (QCT), Qualcomm Technology Licensing (QTL), and Qualcomm Strategic Initiatives (QSI) segments, blending chip innovation with technology licensing and strategic investments.

Known for its Snapdragon processors and 5G modems, Qualcomm powers smartphones, smart homes, and connected vehicles. With four decades of expertise, it is expanding intelligent computing through AI, energy-efficient performance, advanced wireless solutions, and its Dragonwing platforms for enterprise and industrial markets.

QCOM has had a rough stretch. The stock trades nearly 37.8% below its 52-week high of $205.95, reached last October. Over the past year, shares have slipped about 10%. The pressure has intensified more recently, with the stock down 21% in the last three months.

In the first week of January, QCOM was trading above $180. Today, it sits just slightly below $140, essentially giving back two years of progress and returning to levels last seen around 2020.

Softer-than-expected Q2 guidance in the recent Q1 report added to concerns about the smartphone cycle and whether Qualcomm can drive meaningful growth beyond it. Investors who have seen similar slowdowns before seem to be losing patience. Adding to the weight, analysts are now turning cautious.

Technically, though, there are early signs of stabilization. The 14-day RSI plunged into deeply oversold territory in February, showing extreme selling pressure. The RSI has since recovered to 35.45, suggesting the worst of the panic may be fading. Plus, QCOM has held support near $132 after the sharp post-earnings drop. Bears have not been able to break below that level. After weeks of steady declines, recent sessions have shown more consistent green days, and that’s a subtle but meaningful shift in tone.

The MACD oscillator suggests momentum may be shifting back to the bulls. The MACD line is trending upward and has crossed above the signal line, while the histogram has turned positive, an early technical sign that buying pressure could be gradually building.

Valuation-wise, QCOM is starting to look cheaper. The stock trades at roughly 12.6 times forward adjusted earnings, a level that sits below both its sector average and its own historical median.

Income investors also have something to like. Qualcomm has raised its dividend for 22 consecutive years. In January, it declared a quarterly payout of $0.89 per share, payable in March. This brings its annualized dividend to $3.56 per share, yielding 2.52%. Plus, its forward payout ratio of 29% hints that the company might keep boosting its dividends in the future.

QCOM Slips After Its Q1 Report

On Feb. 4, after the market closed, QUALCOMM reported first-quarter fiscal 2026 results. Revenue amounted to $12.3 billion, up 5% year-over-year (YOY), while adjusted EPS rose 3% annually to $3.50, both slightly ahead of consensus estimates.

The QTL licensing segment generated $1.6 billion in revenue with strong margins, helped by higher unit volumes and a favorable mix. Meanwhile, the core QCT chip business delivered $10.6 billion in revenue. Handset revenue hit a record $7.8 billion, supported by premium smartphone launches. IoT revenue climbed 9% YOY to $1.7 billion, driven by consumer and networking demand, and automotive revenue rose 15% annually to $1.1 billion as adoption of Snapdragon Digital Chassis platforms gained momentum.

Additionally, Qualcomm returned $3.6 billion to shareholders through buybacks and dividends and ended the quarter with $7.2 billion in cash, generating $5 billion in operating cash flow in Q1.

However, the strong quarter was overshadowed by softer Q2 guidance. Management projected revenue between $10.2 billion and $11 billion and adjusted EPS is estimated to be between $2.45 and $2.65, both below Wall Street’s expectations. The cautious outlook triggered an 8.5% drop in the next session, as investors worried about near-term growth headwinds.

The company faces uncertainty in global memory markets, as AI-driven data center demand diverts supply from smartphones, raising costs. In China, device makers are cutting production and tightening inventories to manage these mounting pricing pressures.

The management believes that the core handset demand is still solid, supported by strong December-quarter shipments and a healthy Snapdragon pipeline. However, near-term caution remains as OEMs trim production, leading to softer chipset orders. Q2 QCT handset revenue is expected around $6 billion, down sequentially. Management believes growth will rebound once memory supply and pricing conditions normalize.

On a brighter note, QCT IoT revenue is projected to grow in the low teens annually, while automotive revenue is expected to accelerate more than 35%, reflecting strong momentum in connected vehicle platforms.

Analysts predict QUALCOMM’s Q2 EPS to decline 19.6% YOY to $1.89. Looking ahead, EPS is projected to slip 15.4% YOY to $8.52 in fiscal 2026, but then rise by 1.1% to $8.61 in fiscal 2027.

What Do Analysts Expect for QCOM Stock?

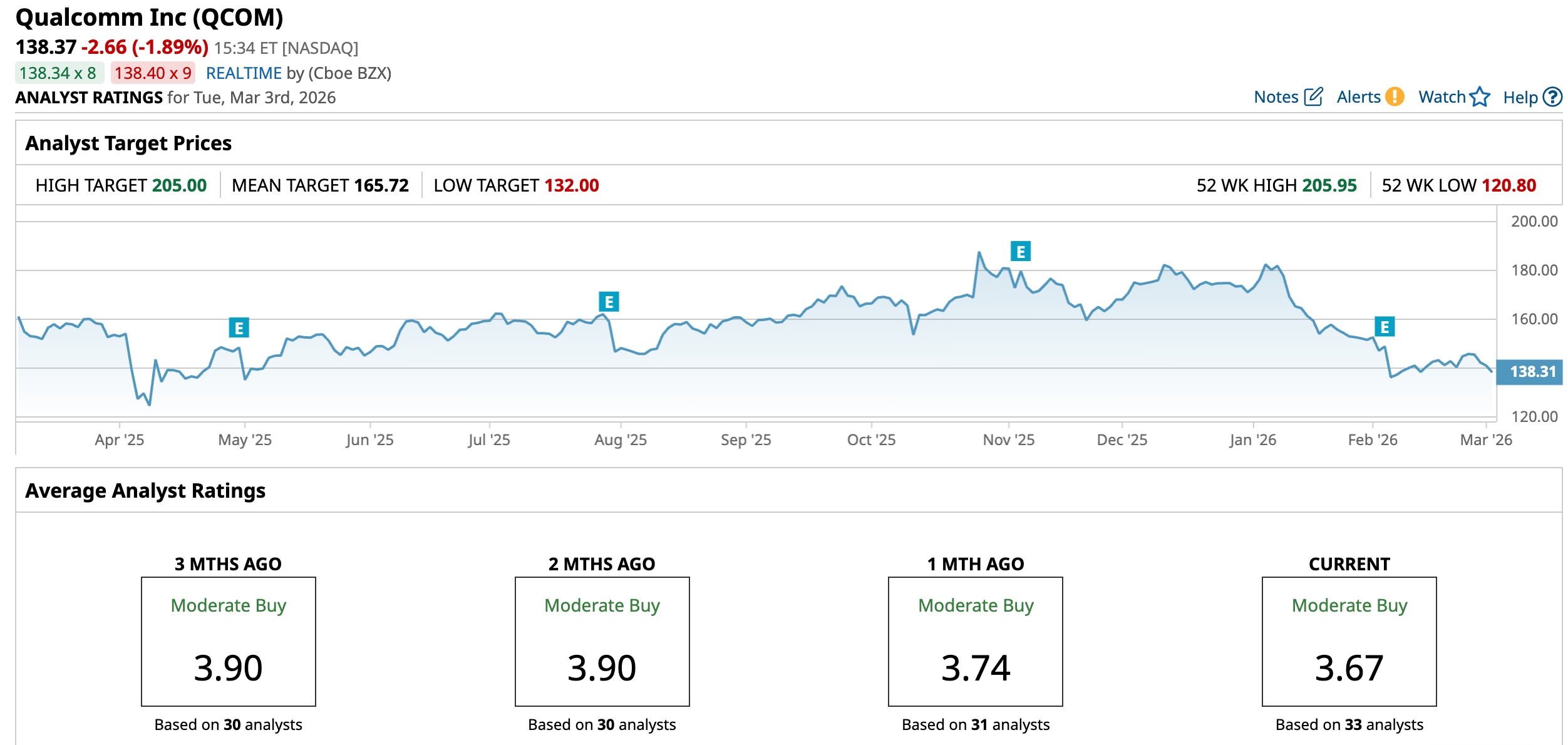

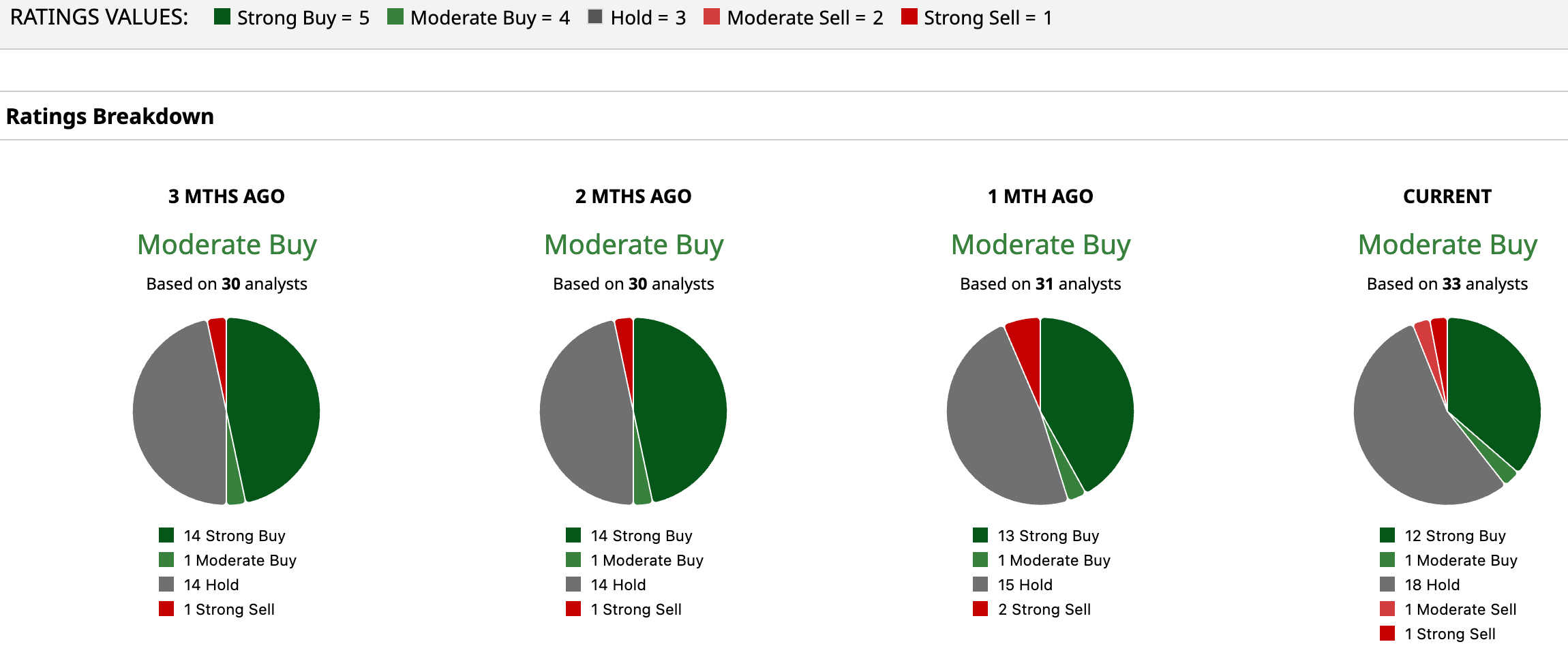

After QUALCOMM’s Q2 outlook, multiple brokerages have expressed caution on QCOM stock. Yet some are optimistic. Overall, Wall Street rates QCOM stock a “Moderate Buy.” Out of the 33 analysts that cover the stock, 12 suggest a “Strong Buy,” one recommends a “Moderate Buy,” 18 analysts are playing it safe with a “Hold” rating, one has a “Moderate Sell,” and the remaining one rates it a “Strong Sell.”

Based on its mean target price of $165.72, QCOM stock has upside potential of 19.8% from current levels. Its Street-high target price of $205 implies the stock could rally as much as 48% in the next 12 months.

Final Thoughts on QCOM Stock

QUALCOMM sits at a crossroads. The stock has clearly taken technical and sentiment damage in 2026. Yet the business itself remains profitable, cash-generative, and reasonably valued, with steady dividend growth and expanding opportunities in automotive and IoT.

Early technical signals suggest selling pressure may be easing, though earnings estimates still point to near-term softness. For long-term investors who believe memory conditions will normalize and growth will reaccelerate, this pullback could offer an opportunity. For others, waiting for clearer momentum may be the safer path.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)