SentinelOne’s stock price has taken a beating over the past six months, shedding 27.8% of its value and falling to $13.02 per share. This might have investors contemplating their next move.

Following the drawdown, is now the time to buy S? Find out in our full research report, it’s free.

Why Is SentinelOne a Good Business?

Built on the principle of "fighting machine with machine," SentinelOne (NYSE:S) provides an AI-powered cybersecurity platform that autonomously prevents, detects, and responds to threats across endpoints, cloud workloads, and identity systems.

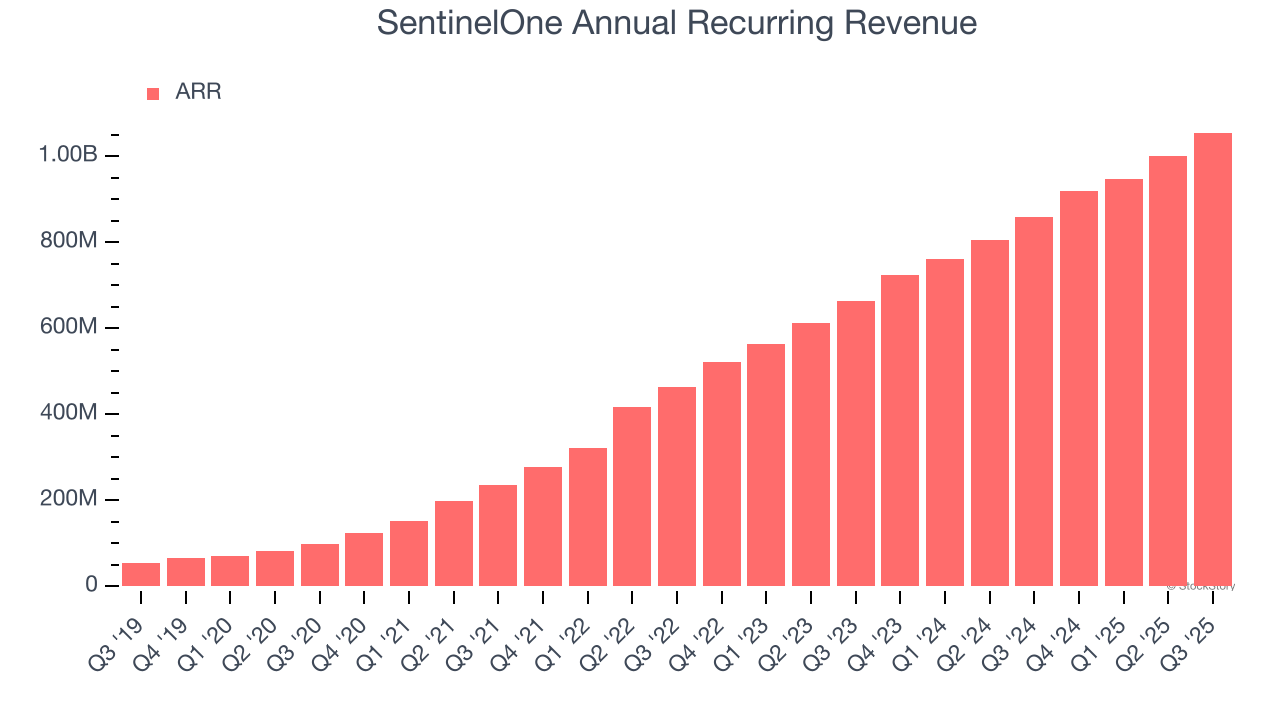

1. ARR Surges as Recurring Revenue Flows In

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

SentinelOne’s ARR punched in at $1.06 billion in Q3, and over the last four quarters, its year-on-year growth averaged 24.6%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes SentinelOne a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect SentinelOne’s revenue to rise by 20.1%. While this projection is below its 29.1% annualized growth rate for the past two years, it is commendable and indicates the market is forecasting success for its products and services.

3. Projected Free Cash Flow Gains to Pump Profits

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the next year, analysts predict SentinelOne’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 4.7% for the last 12 months will increase to 10%, it options for capital deployment (investments, share buybacks, etc.).

Final Judgment

These are just a few reasons SentinelOne is a rock-solid business worth owning. With the recent decline, the stock trades at 3.8× forward price-to-sales (or $13.02 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than SentinelOne

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

/NVIDIA%20Corp%20logo%20on%20phone-by%20Evolf%20via%20Shutterstock.jpg)

/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)

/Broadcom%20Inc%20logo%20on%20building-by%20Poetra_%20RH%20via%20Shutterstock.jpg)