Electronic component designer Celestica (CLS) is currently cashing in on the artificial intelligence (AI) boom by supplying tech giants with Ethernet switches and other equipment. The spending spree has turned the tide for Celestica, making it the top supplier of 800 Gbps Ethernet switches to leading hyperscale tech giants.

The company also has a longstanding partnership with chip giant Advanced Micro Devices (AMD), which has positioned it as a beneficiary of AMD’s multi-year collaboration with Meta Platforms (META) , whereby the social media giant is set to spend “double-digit billions” per gigawatt on AMD chips and equipment.

With Celestica’s stock up 37% over the past six months, are there any upsides left in it, especially as it cashes in on hyperscaler demand?

About Celestica Stock

Based in Toronto, Canada, Celestica focuses on design, manufacturing, supply chain management, and after-market services. It operates a global network of sites, serving industries such as aerospace, defense, communications, enterprise, healthtech, industrial, and smart energy.

The firm collaborates with top brands to oversee the entire product lifecycle, from initial concepts and production to fulfillment and sustained support. Celestica has a market capitalization of $32.1 billion.

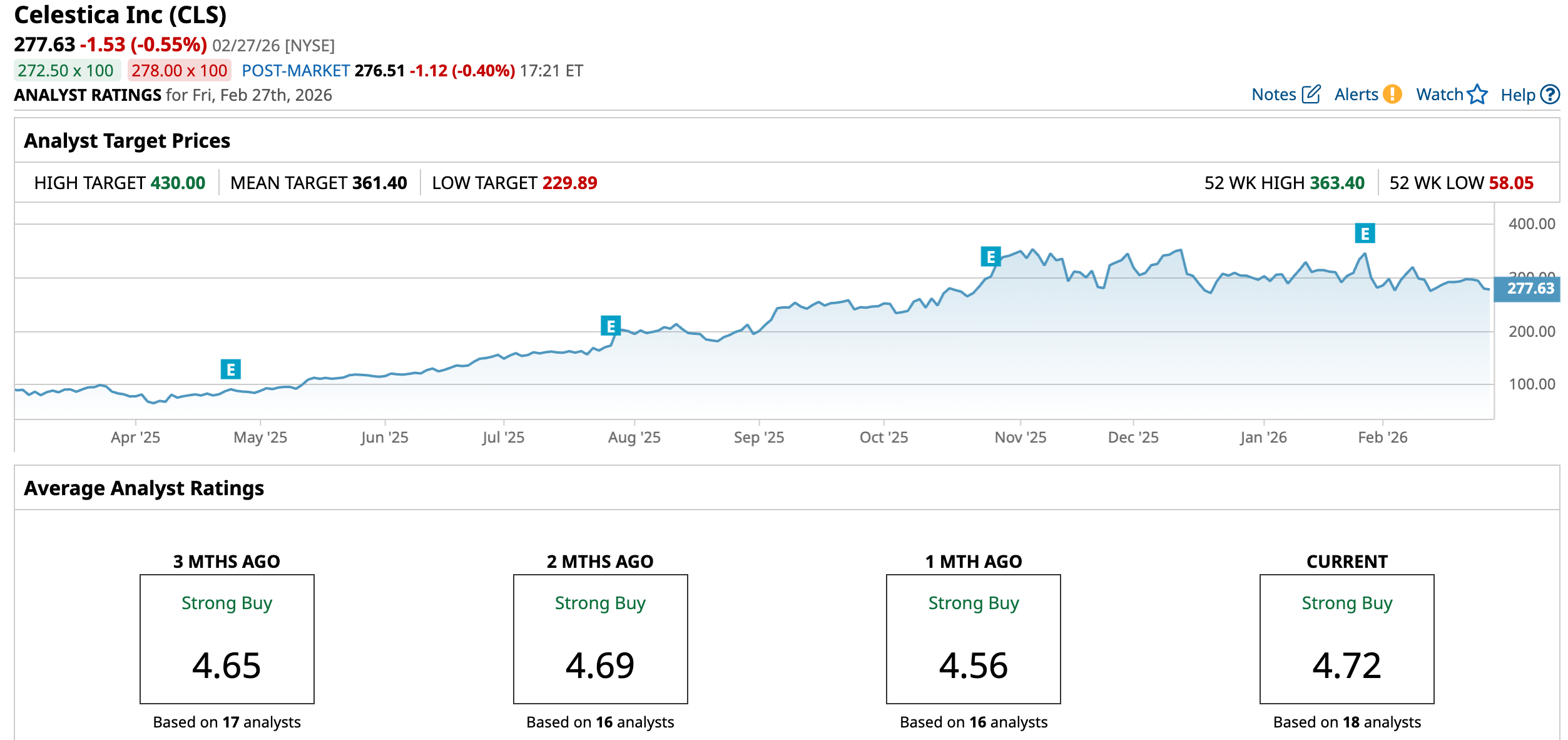

Celestica’s stock has been reaping the gains from AI hyperscaler demand and a solid earnings beat. Over the past 52 weeks, the stock has gained 157.4%, and over the past six months, it has gained 37.4%. On the other hand, the stock is down marginally this year. The shares had reached a 52-week high of $363.40 in Nov. 2025, but are down 23.6% from that level.

On a forward-adjusted basis, Celestica’s price-to-earnings ratio of 35.21x is higher than the industry average of 22.26x.

Celestica Beats Q4 Expectations As Strong AI Demand Fuels Robust Earnings and Bright Outlook

On Jan. 28, Celestica reported strong fourth-quarter results for fiscal 2025, which topped its own expectations by a healthy margin. The company’s revenue increased 43.6% year-over-year (YOY) to $3.65 billion, exceeding its guided $3.33 billion to $3.58 billion range.

Connectivity & Cloud Solutions (CCS), which comprises its communications and enterprise (servers and storage) end markets, did the heavy lifting, generating $2.86 billion in revenue. This segment’s margin was 8.4%, up from 7.9% in the prior-year period. Celestica’s non-GAAP EPS was $1.89, up 70.3% YOY and higher than the company’s $1.65 to $1.81 guided range.

Celestica’s results coming in hotter than its own expectations have led the company to raise its current-year outlook. It raised the 2026 revenue outlook by $1 billion to $17 billion, while its adjusted EPS outlook was raised from $8.20 to $8.75.

In addition, the company is envisioning helping its largest customers with their long-term AI investments, with multi-year capacity roadmaps. Celestica is planning to expand its manufacturing capacity in the U.S. (scheduled for completion in 2027) to bolster its ability to support the production of complex data center hardware, including Google Tensor Processing Unit (TPU) systems. Hence, it’s not a surprise that it’s expected to incur higher capex this year, approximately $1 billion, or about 6% of the current annual revenue outlook.

Wall Street analysts have a positive view about Celestica’s bottom-line trajectory. For the current quarter, its EPS is expected to grow by 96% YOY to $1.96. For fiscal 2026, the company’s EPS is projected to increase by 49.9% annually to $8.35, followed by a 45% increase to $12.11 in fiscal 2027.

What Analysts Think About Celestica’s Stock

Post the Q4 earnings, analysts at Barclays maintained a bullish “Overweight” rating on Celestica’s stock and raised the price target from $359 to $391. Moreover, analysts have stated that the company’s upward revision of its revenue outlook is conservative and that further revisions may be made this year.

They are also positive about the company’s growing exposure to high-growth end markets tied to next-generation computing infrastructure. On the other hand, Citigroup’s analyst Atif Malik lowered the price target from $375 to $338, while maintaining a “Buy” rating.

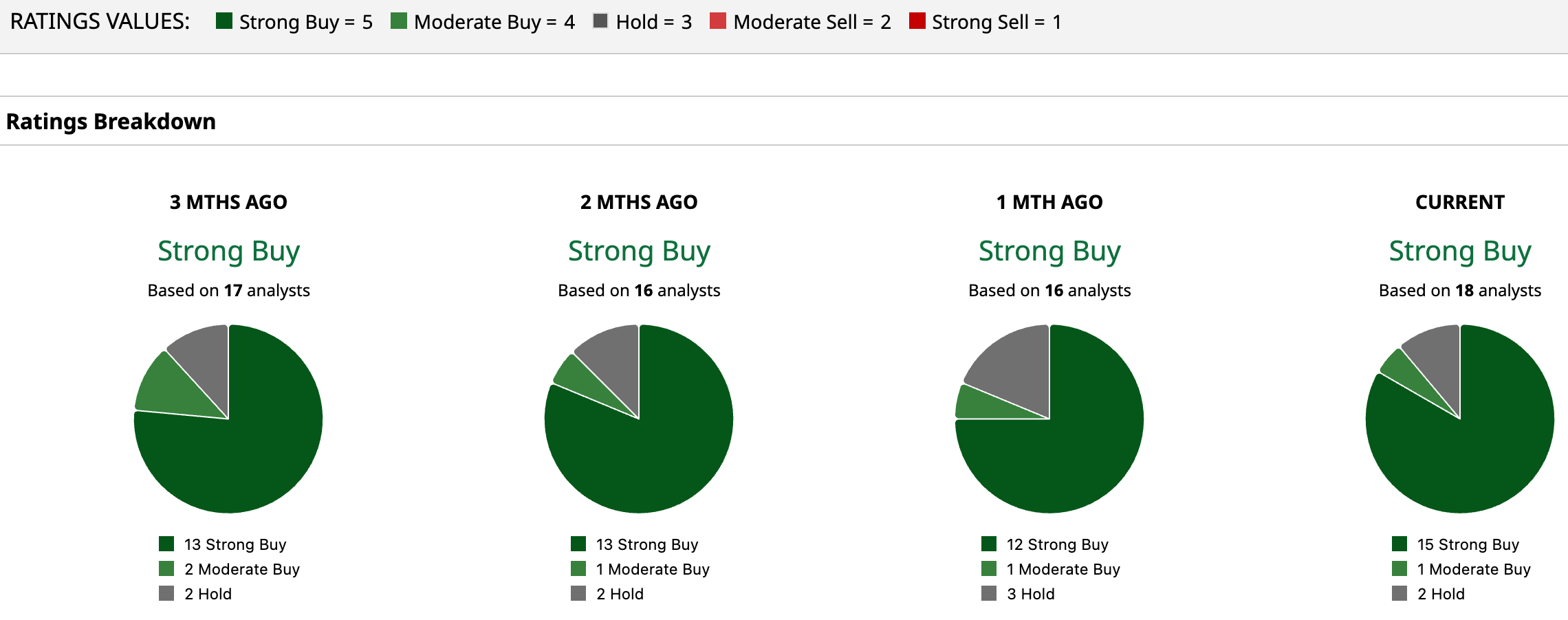

Celestica is gaining praise on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 18 analysts rating the stock, a majority of 15 analysts have given it a “Strong Buy” rating, one analyst rated it “Moderate Buy,” while two analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $361.40 represents a 30.2% upside from current levels. The Street-high price target of $430 implies a 54.9% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)