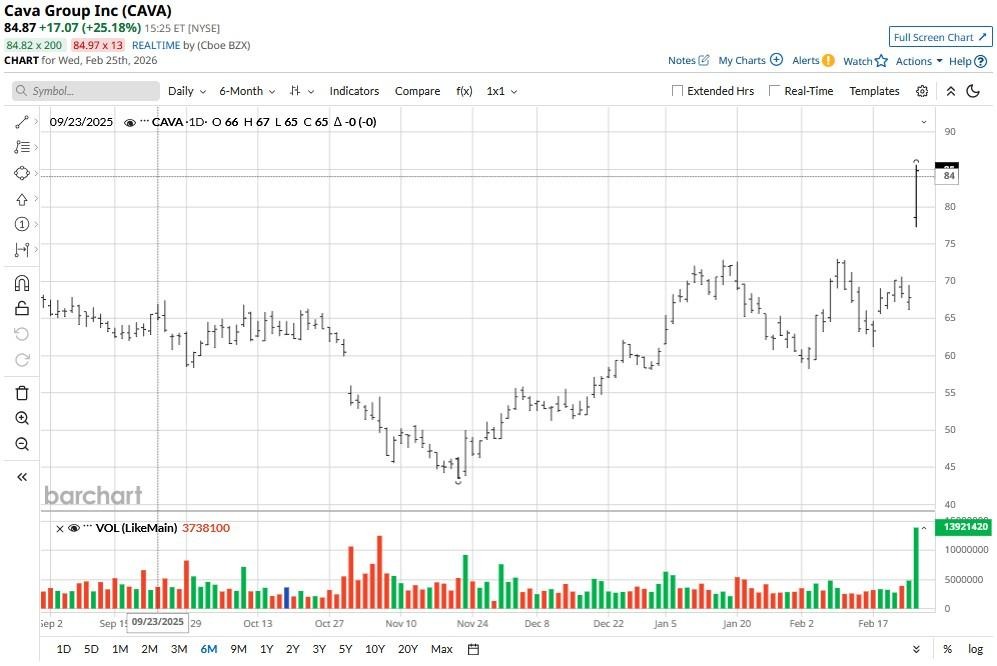

Cava Group (CAVA) jumped about 25% higher on Wednesday after the Mediterranean fast-casual restaurant chain said a strong Q4 helped its full-year revenue surpass $1 billion for the first time. This meteoric run pushed CAVA’s relative strength index (14-day) in the 70s, signaling overbought conditions that often precede a significant correction.

Still, for long-term investors, it’s reasonable to load up on CAVA stock at current levels, especially since it’s still down about 15% versus its 52-week high.

Is it Too Late to Invest in CAVA Shares?

CAVA shares remain worth owning as management plans on opening another 75 restaurants this year, several of them in untapped Midwestern markets, to scale its national footprint in pursuit of sustainable growth.

A 21% year-on-year increase in its revenue to $275 million in the fourth quarter and guidance for about 4% same-store sales growth in 2026 is particularly impressive, given that CAVA has opted for significantly smaller price increases than rivals.

In the fourth quarter, CAVA’s restaurant-level profit margin climbed to 21.4% while its better-than-expected full-year outlook for about $180 million adjusted EBITDA reflects operational discipline and management’s confidence despite commodity and wage pressures.

Note that CAVA broke decisively above its 200-day moving average (MA) on Wednesday as well, which further reinforces that bullish momentum will likely sustain — at least in the near term.

Stifel Raises Price Target on CAVA Stock

Stifel analysts also believe CAVA stock will rip higher from here through the remainder of 2026.

According to them, the company’s Q4 earnings suggest its “differentiated, craveable Mediterranean cuisine” is stealing share from legacy fast-casual rivals.

CAVA managed to defy sector-wide weakness in recent months, and its guidance for same-store sales growth may prove overly conservative as the year unfolds, the analysts added.

In its research note, Stifel also dubbed the firm’s investments in infrastructure (including its assistant general manager program) as a “necessary step to support mid- to high-teens unit growth.”

Together with menu innovation and a fast-growing digital footprint, CAVA looks on track to hitting $90 in 2026, it concluded.

How Wall Street Recommends Playing CAVA Group

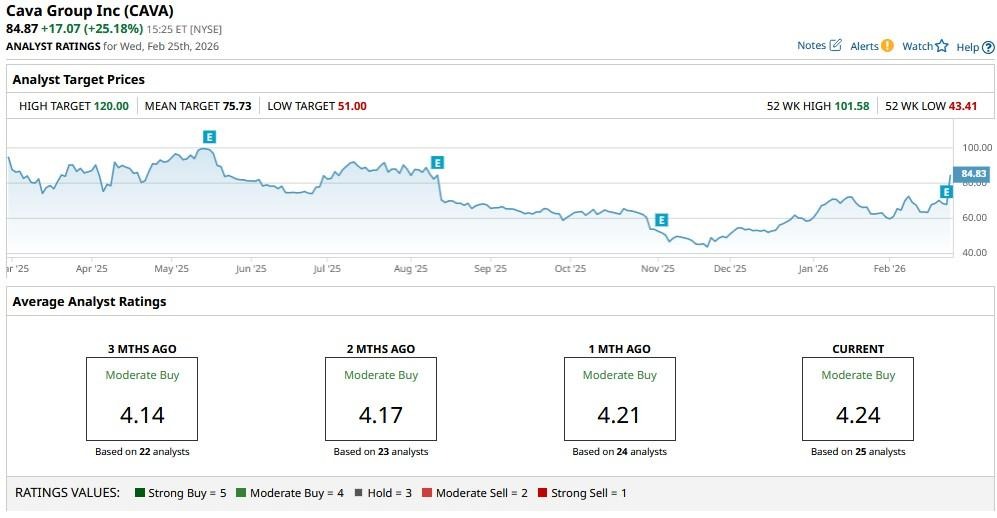

Heading into the earnings print, the consensus “Moderate Buy” rating on CAVA shares came with a $76 mean price target.

However, it’s reasonable to expect upward revisions now that CAVA has reported a blockbuster Q4.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)