Carvana (CVNA) revolutionizes used car buying with a fully online platform, letting customers browse thousands of inspected vehicles using 360° photos, get instant financing, and choose home delivery or pickup from signature coin-operated vending machines.

Carvana sources cars via auctions and trade-ins, reconditions them at inspection centers, and earns from vehicle sales, financing interest, and protection plans, disrupting traditional dealerships with convenience and transparency.

Founded in 2012, Carvana went public in 2017 and is headquartered in Phoenix, Arizona. It operates exclusively in the United States across 47+ states with 30+ vending machines and reconditioning centers, delivering cars nationwide.

Carvana Stock Lags Short Term

CVNA stock has plunged recently, down 5% over the past five days and 30% in the last month. It edged up 1% over three months but sits 21% lower year-to-date (YTD). Over 52 weeks, shares gained 54% and are now 32% off the $486.89 high. Epic multi-year surges include over 381% over two years and 3122% in three years.

Compared to the S&P 500 Consumer Discretionary Index, CVNA outperformed long-term, with 52-week gains of 54%, topping the index's 40% growth, while three-year gains come to 3,122% (compared to the index's 17%). Short-term, the index declined 7% in a month, highlighting cyclical auto sector risks.

Carvana Drops on Results

Carvana crushed sales expectations in the fourth quarter of 2025 with record revenue of $5.60 billion, up 58% year-over-year (YoY) and beating Wall Street's $5.26 billion forecast. Retail vehicle sales exploded 43% to 163,522 units, 5,000 more than anticipated, while wholesale volumes surged 66%. This propelled total gross profit up 38% to $1.05 billion, showcasing Carvana's operational scale and market share gains in used cars.

However, profitability flagged investor concerns. Profit per retail vehicle fell $244 ($354 adjusted), and wholesale margins contracted 18.2% amid competitive pressures. Adjusted EBITDA reached $511 million but missed the $539 million estimate, with margins narrowing to 9.1% (down 100 basis points) due to higher costs and investments.

Adjusted EPS of $4.22 topped the $1.12 consensus but was inflated by one-time charges, masking underlying trends.

No formal full-year sales guidance was given, but management reiterated ambitions for 3 million annual vehicle sales between 2030 and 2035 and a 13.5% EBITDA margin target in FY2026, signaling confidence in long-term execution despite near-term hiccups.

Should You Buy the Dip in CVNA?

Carvana's Q4 delivered record revenue and unit sales, proving its online used-car model scales impressively amid market recovery. Profitability concerns surrounding declining gross profit per vehicle and margins sparked the 20%+ drop, but these reflect growth investments rather than structural flaws. Adjusted EBITDA still rose to $511 million, and debt reduction to $4.83 billion strengthens the balance sheet.

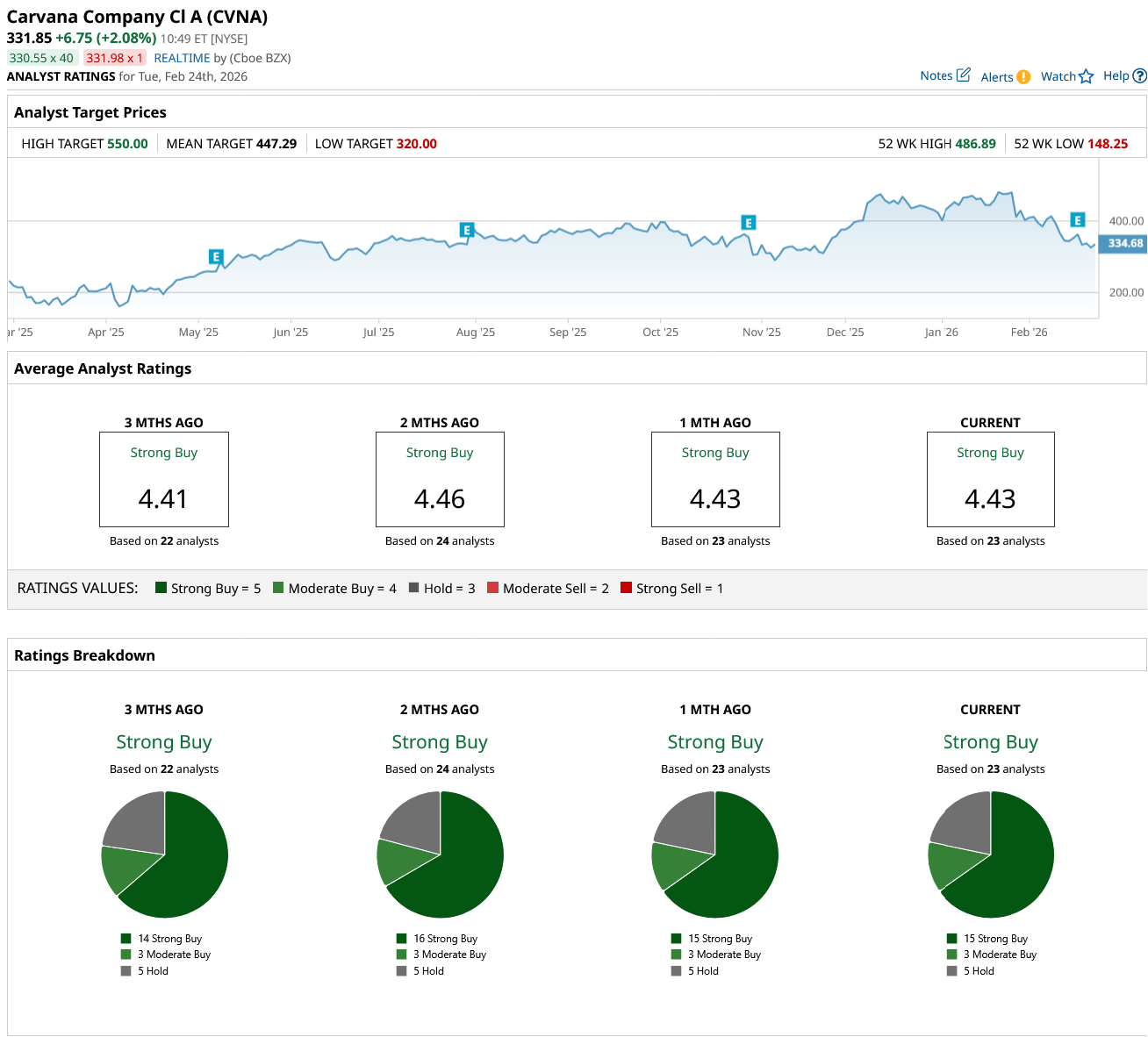

Analyst sentiments remain bullish with a consensus "Strong Buy" rating, with a $447.29 mean target, which implies 35% upside from the current market price. CVNA stock has received 15 “Strong Buy” ratings, three “Moderate Buy” ratings, and five “Hold” ratings from a total of 23 analyst ratings.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)