/PayPal%20Holdings%20Inc%20sign%20on%20building-%20by%20Sundry%20Photography%20via%20Shutterstock.jpg)

PayPal (PYPL) will announce its fourth-quarter 2025 earnings on Feb. 3, and the announcement comes at a time when investor sentiment around the stock remains cautious. While the company has continued to deliver profitable growth, drive monthly active customers, and increase engagement among existing users, its share price has been under pressure. Over the past three months, PYPL stock has fallen nearly 24%, significantly lagging the broader market and many of its peers.

The significant decline in PayPal's stock reflects growing concern about competition in the digital payments industry. PayPal is no longer viewed as the uncontested leader it once was, as major players such as Apple Pay, Shop Pay, and Stripe Link have gained momentum. In addition, the rise of buy-now-pay-later providers has further fragmented the market, gradually eroding PayPal’s dominance.

The broader economic backdrop has also weighed on the stock. With ongoing macroeconomic uncertainty expected to hurt consumer spending, investors remain cautious.

Another key issue is profitability. PayPal has been investing to drive long-term growth, but those efforts may pressure near-term margins and limit bottom-line growth in the coming quarters. This has contributed to the stock’s recent struggles.

Now that the company is approaching its earnings release, historical trends suggest caution may be warranted. PayPal shares have declined after three of the past four quarterly reports, including a 4.6% drop following its third-quarter results.

Options market activity suggests that traders are expecting a post-earnings move of about 7.3% in either direction for contracts expiring Feb. 6. That’s slightly above the stock’s average swing of about 7.1% over the past four quarters.

PayPal Q4 Earnings: What to Expect?

PayPal’s stock may have lagged the broader market recently, but the company is still expected to deliver growth in both revenue and earnings in the fourth quarter, supported by rising payment volumes. That said, the pace of growth could ease slightly compared to earlier in the year.

A key metric to monitor will be transaction margin dollars, which management expects to come between $4.02 billion and $4.12 billion. At the midpoint, that represents 3.5% growth. When excluding interest earned on customer balances, transaction margin dollars are projected to rise about 5%, a step down from the 7% growth PayPal has posted so far this year. This moderation reflects tougher year-over-year (YoY) comparisons, as PayPal is now cycling against a strong consumer spending period from last year’s holiday quarter.

In addition, branded checkout growth, while still positive, is expected to decelerate somewhat from its third-quarter pace, which could weigh on transaction margin expansion.

Still, PayPal could continue to benefit from its core branded checkout business, steady credit trends, improved profitability in its payment services provider (PSP) business, and increasing monetization of Venmo.

PayPal’s user growth and engagement could remain steady in Q4. In the previous quarter, PayPal’s active accounts rose 1% to 438 million, while monthly active accounts increased 2% YoY to 227 million. Transactions per active account, excluding PSP activity, climbed 5%.

Another bright spot could be PayPal’s Buy Now, Pay Later (BNPL) business, which has been gaining traction despite heightened competition. In the third quarter, BNPL volume grew more than 20%, with notable strength in the U.S., and that momentum is expected to carry into Q4.

On the profitability, PayPal’s adjusted earnings per share (EPS) have climbed at a double-digit rate so far in 2025. However, growth may moderate slightly in the fourth quarter as the company invests in growth initiatives. Management is guiding for adjusted EPS of $1.27 to $1.31, representing 7% to 10% growth YoY.

Analysts expect PayPal to report EPS of $1.29 per share, up 8.4% YoY. Notably, PayPal has a solid track record of outperforming expectations, having beaten earnings estimates in each of the past four quarters, including a 12.6% positive surprise in Q3.

The Bottom Line

PayPal is facing rising competition and a challenging macroeconomic backdrop. While PayPal continues to generate profitable growth, expand user engagement, and benefit from areas such as Venmo monetization and BNPL momentum, concerns about slowing transaction-margin expansion and near-term margin pressure remain.

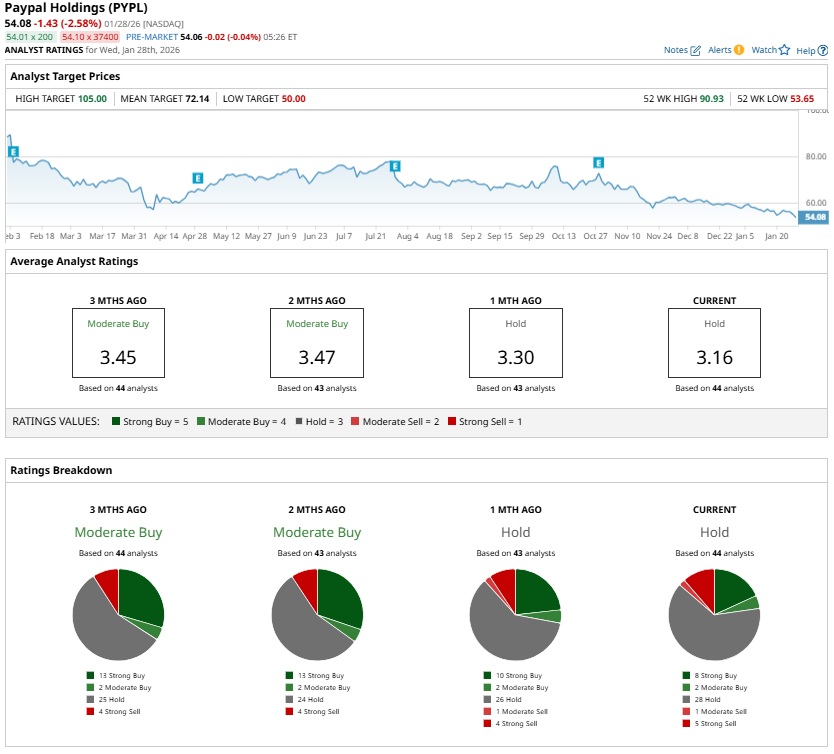

Although the stock has fallen significantly in recent months, investors should take caution ahead of the Q4 earnings release. Analysts maintain a “Hold” consensus rating on PYPL stock ahead of Q4 earnings.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)