Industrial conglomerate GE Aerospace (NYSE:GE) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 17.6% year on year to $12.72 billion. Its non-GAAP profit of $1.57 per share was 9.5% above analysts’ consensus estimates.

Is now the time to buy GE Aerospace? Find out by accessing our full research report, it’s free.

GE Aerospace (GE) Q4 CY2025 Highlights:

- Revenue: $12.72 billion vs analyst estimates of $11.18 billion (17.6% year-on-year growth, 13.8% beat)

- Adjusted EPS: $1.57 vs analyst estimates of $1.43 (9.5% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $7.25 at the midpoint, beating analyst estimates by 1.8%

- Operating Margin: 17.9%, in line with the same quarter last year

- Free Cash Flow Margin: 13.8%, similar to the same quarter last year

- Market Capitalization: $336 billion

Company Overview

One of the original 12 companies on the Dow Jones Industrial Average, General Electric (NYSE:GE) is a multinational conglomerate providing technologies for various sectors including aviation, power, renewable energy, and healthcare.

Revenue Growth

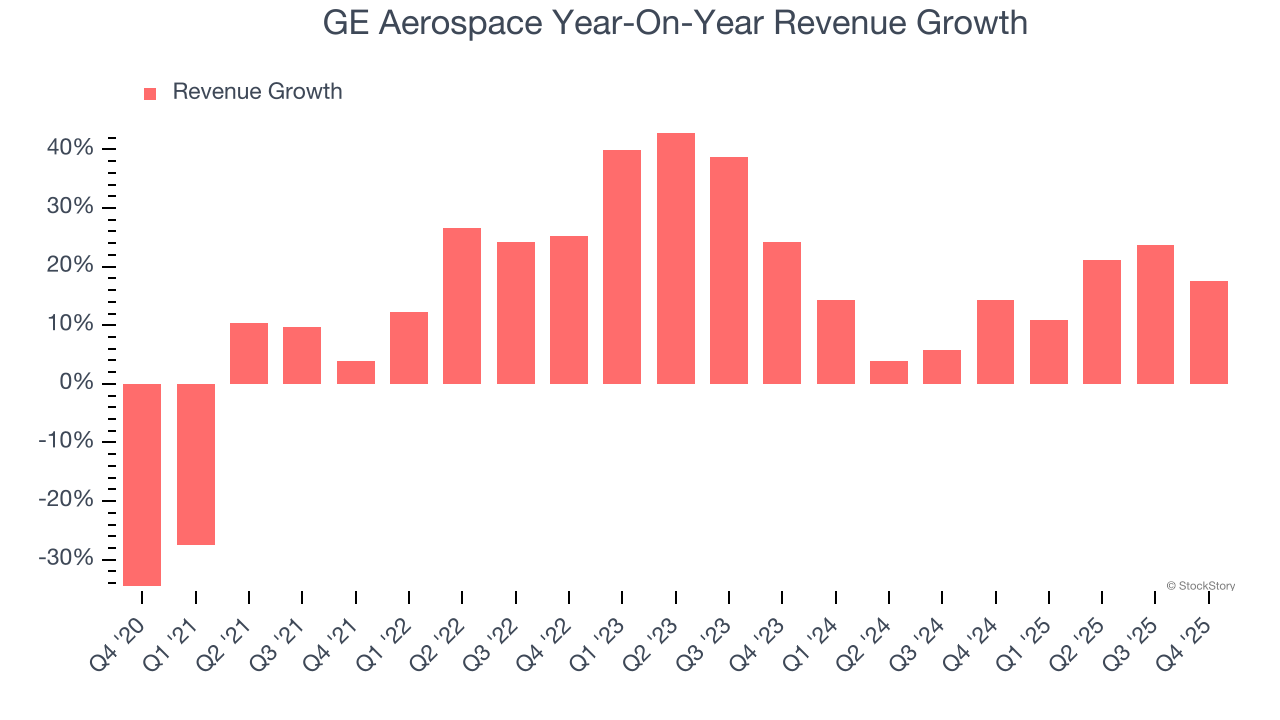

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, GE Aerospace grew its sales at an incredible 15.8% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. GE Aerospace’s annualized revenue growth of 13.9% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, GE Aerospace reported year-on-year revenue growth of 17.6%, and its $12.72 billion of revenue exceeded Wall Street’s estimates by 13.8%.

Looking ahead, sell-side analysts expect revenue to grow 1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

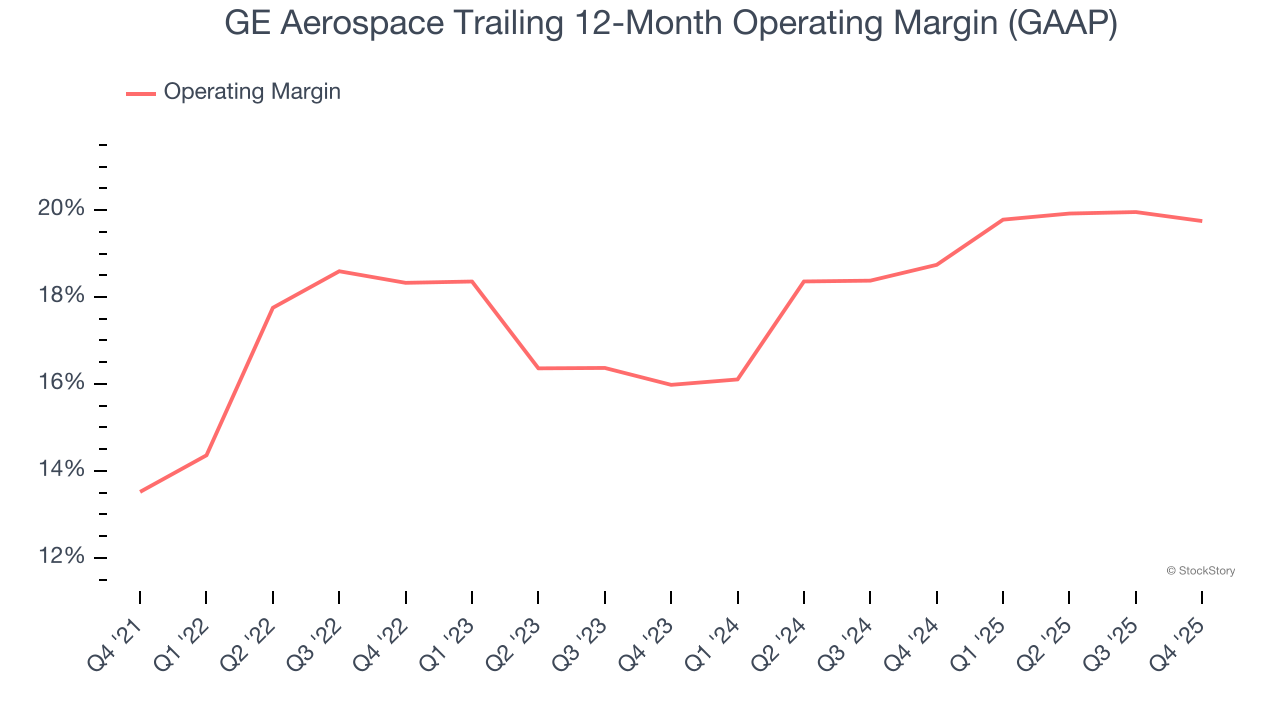

GE Aerospace has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17.7%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, GE Aerospace’s operating margin rose by 6.2 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, GE Aerospace generated an operating margin profit margin of 17.9%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

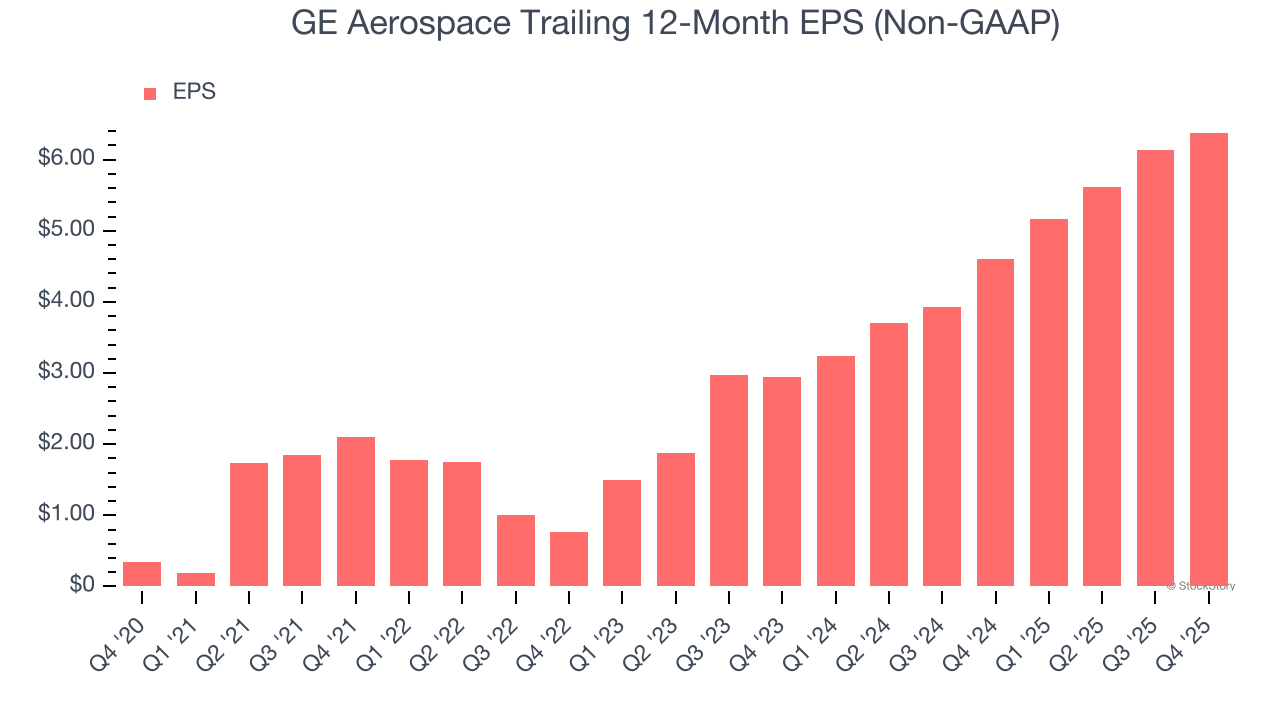

GE Aerospace’s EPS grew at an astounding 79.3% compounded annual growth rate over the last five years, higher than its 15.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

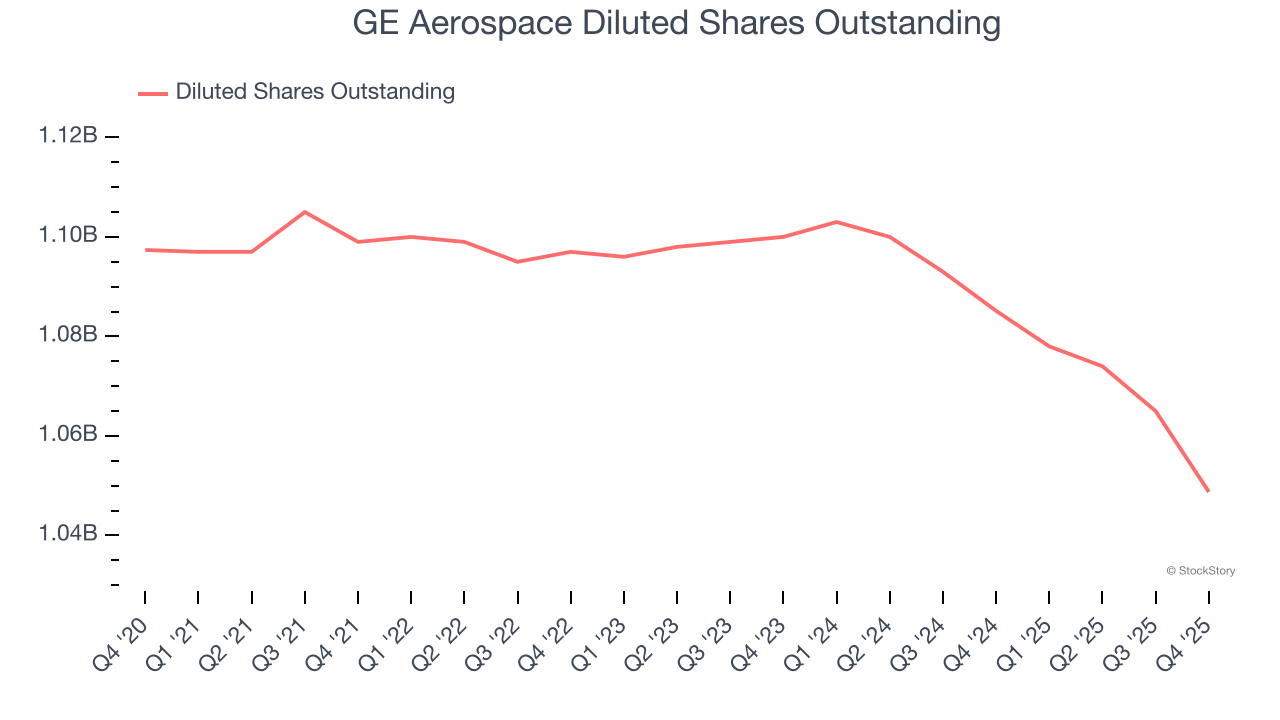

Diving into GE Aerospace’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, GE Aerospace’s operating margin was flat this quarter but expanded by 6.2 percentage points over the last five years. On top of that, its share count shrank by 4.4%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For GE Aerospace, its two-year annual EPS growth of 47.1% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, GE Aerospace reported adjusted EPS of $1.57, up from $1.32 in the same quarter last year. This print beat analysts’ estimates by 9.8%. Over the next 12 months, Wall Street expects GE Aerospace’s full-year EPS of $6.38 to grow 10.4%.

Key Takeaways from GE Aerospace’s Q4 Results

We were impressed by how significantly GE Aerospace blew past analysts’ revenue expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. Investors were likely hoping for more, and shares traded down 1.8% to $312.71 immediately following the results.

Big picture, is GE Aerospace a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

/AI%20(artificial%20intelligence)/AI%20software%20engineering%20by%20Tapati%20Rinchumrus%20via%20Shutterstock.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Apple%20Inc%20phone%20and%20data-by%20Anderson%20Reis%20via%20Shutterstock.jpg)