Energy markets rarely move in straight lines — they react to shockwaves. This week’s tremor came from Venezuela, a nation sitting atop the world’s largest proven oil reserves, suddenly thrust into chaos after a surprise U.S. military strike captured President Nicolás Maduro and his wife, Cilia Flores. The action did not just rattle Caracas, but sent a signal through global oil markets. Any disruption to Venezuela’s fragile export system threatens future supply, and even in a market wrestling with short-term oversupply, longer-dated oil prices tend to reprice risk fast.

That is exactly what unfolded. Crude-linked stocks (CLG26) moved higher as investors began recalibrating for tighter supply dynamics and heavier U.S. involvement in revitalizing Venezuelan oil assets.

Notably, some oil and gas companies may do well in 2026 even if crude prices soften, supported by disciplined capital allocation, strong cash flows, and resilient business models. Against this backdrop, GeoPark Limited (GPRK), Sunoco (SUN), and Cenovus Energy (CVE) could be wise 2026 portfolio additions.

Let’s take a closer look at them.

Oil and Gas Stock #1: GeoPark

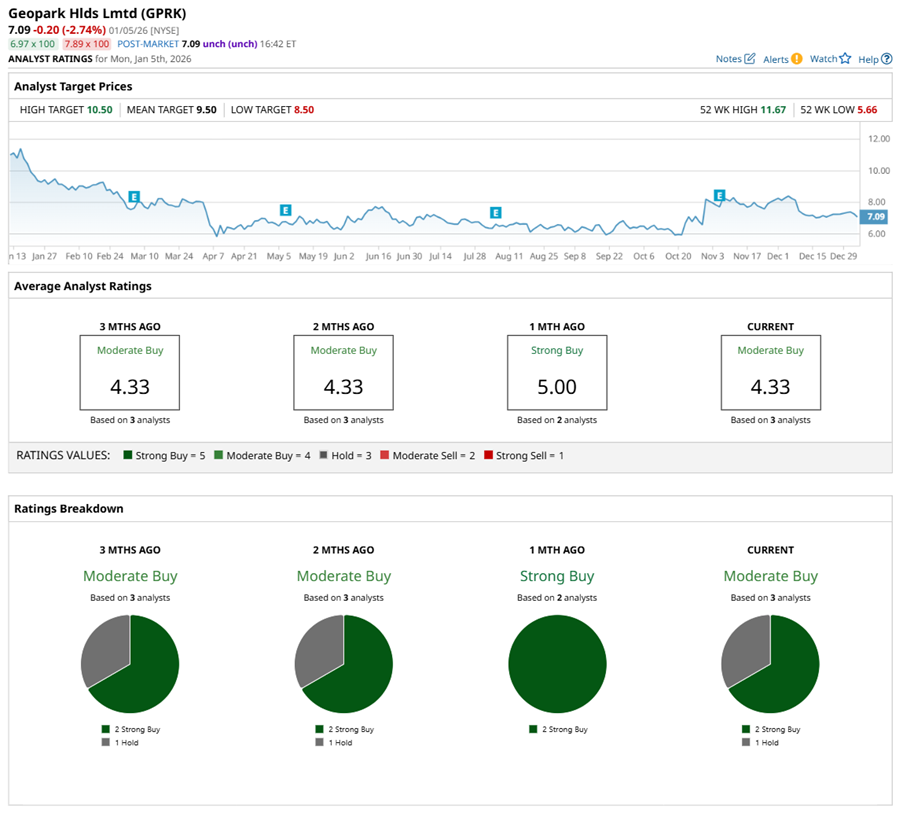

Founded in 2002, GeoPark has steadily built a foothold in Latin America’s energy patch, drilling and producing oil and natural gas across Colombia, Chile, Brazil, Argentina, and Ecuador. Headquartered in Bogotá, Colombia, the company blends regional expertise with operational grit. With a market capitalization of $373 million, GeoPark operates in volatile markets, relying on a seasoned footprint to navigate shifting energy cycles.

From a price-action standpoint, GPRK stock has not had an easy run. The stock is down 40% from its 52-week high of $11.67, reflecting a tough year. Still, momentum is quietly turning, with shares up 10% over the past three months. December brought turbulence, though, as the stock slid sharply on Dec. 9, after Parex Resources (PARXF) walked away from acquisition talks.

From a valuation standpoint, GeoPark is a quiet bargain hiding in plain sight. The stock trades at just 12.7 times forward adjusted earnings and 0.70 times sales, levels that sit well below sector norms. Even more telling, its price-to-sales ratio undercuts its own five-year average.

Beyond valuation, GeoPark has been steadily rewarding patience. The company has now paid dividends for six consecutive years and reinforced that commitment in December, paying a $0.03 per share quarterly dividend. Its annualized dividend of $0.12 per share, translating to a 1.62% yield, adds a layer of stability in an otherwise choppy energy market.

On Nov. 5, GeoPark announced its fiscal third-quarter earnings results, delivering a solid quarter with higher production, steady pricing, and disciplined cost control, all in line with its 2025 guidance. At the same time, GeoPark continued to tighten its balance sheet, generate solid cash flow, complete the Vaca Muerta acquisition, and roll out a revised dividend program — small moves that add up strategically.

The Latin American oil explorer’s revenue came in at $125.1 million, up 4% sequentially but down 21% year-over-year (YOY), still ahead of expectations. EPS landed at $0.31, matching estimates.

Production was the real anchor. Consolidated average oil and gas output reached 28,136 barrels of oil equivalent per day (boepd), nearly 3% higher than the prior quarter. Year-to-date (YTD) production averaged 28,194 boepd, sitting comfortably at the high end of full-year guidance. By quarter-end, GeoPark had five rigs running, while Vaca Muerta contributed YTD average production of roughly 2,060 boepd.

Profitability remained solid. Adjusted EBITDA totaled $71.4 million, translating to a strong 57% margin. Operating costs held steady at $12.50 per boe, underscoring cost discipline. The balance sheet also looked resilient, with more than $197 million in cash, net debt of $373.4 million, and a low leverage ratio of 1.2.

Looking ahead, GeoPark is playing the long game. By 2030, it is targeting production of 42,000 to 46,000 barrels per day and adjusted EBITDA between $520 million and $550 million, with a net leverage ratio anticipated to be between 0.8 and 1.0.

Analysts tracking the oil and gas explorer project its Q4 earnings to be $0.28 per share, while fiscal 2025 EPS is expected to be around $0.70. Looking ahead to fiscal 2026, EPS is anticipated to be $0.58.

GPRK stock has a consensus “Moderate Buy” rating overall. Of the three analysts covering it, two recommend “Strong Buy,” and one says “Hold.” The average analyst price target for GPRK stock is $9.50, indicating a potential upside of 38%. The Street-high target price of $10.50 implies 53% upside potential from here.

Oil and Gas Stock #2: Sunoco

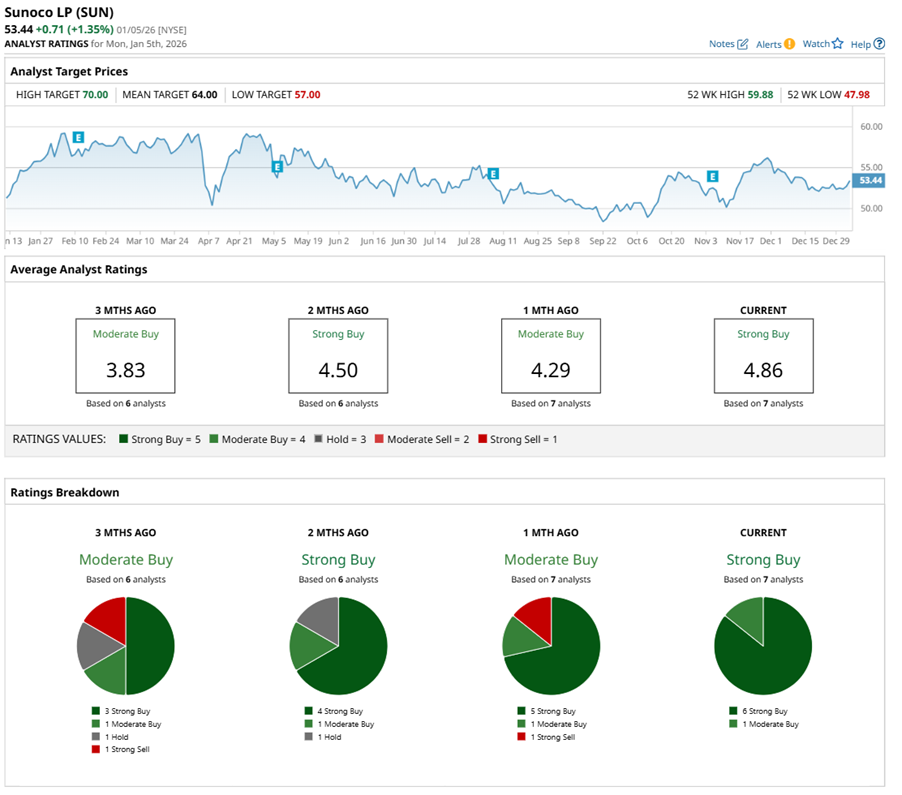

Headquartered in Dallas, Sunoco is a heavyweight in fuel distribution and energy infrastructure, operating across 32 countries and territories spanning North America, the Greater Caribbean, and Europe. Structured as a master limited partnership, it runs roughly 14,000 miles of pipelines and more than 100 terminals.

That backbone supports the distribution of over 15 billion gallons of fuel each year to nearly 11,000 retail locations. With a market cap of $10.8 billion, Sunoco plays a quiet but critical role in energy logistics.

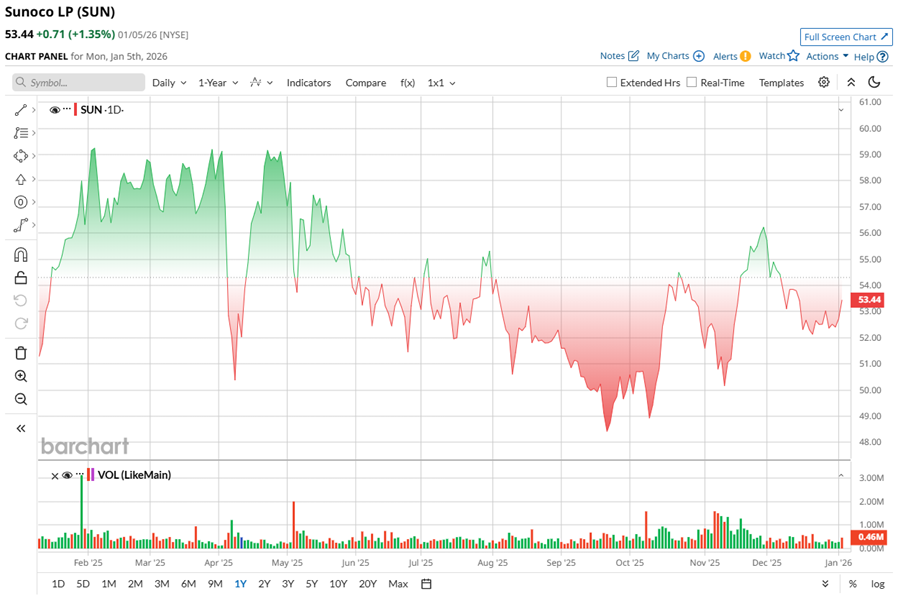

In terms of price performance, SUN stock has cooled slightly, sitting about 10% below its 52-week high of $59.88. Still, the broader trend remains steady, with shares up 4% over the past year and gaining 6% in just the last three months.

SUN stock trades at 0.33 times forward sales, sitting at a clear discount to the sector average. That value story is reinforced by rising payouts. In November, SUN paid a $0.9202 quarterly distribution, or $3.6808 annualized. This marked the fourth-straight quarterly increase, aligning with its plan for at least 5% annual distribution growth.

On Nov. 5, Sunoco reported its Q3 earnings results, delivering a mixed but steady picture. The company topped revenue expectations while falling short on EPS, reflecting both operational momentum and near-term cost pressures. Revenue climbed 5% YOY to $6 billion, while EPS improved sharply to $0.64 from a loss of -$0.26 per share in the prior-year quarter.

Operational performance stood out. Sunoco posted a record adjusted EBITDA of $496 million, up from $470 million a year earlier, underscoring the strength of its fuel distribution model. During the quarter, motor fuel volumes reached 2.29 billion gallons, with fuel margins averaging 10.7 cents per gallon. Cash generation remained solid, though distributable cash flow, as adjusted, slipped to $326 million from $349 million last year.

The balance sheet remains a point of confidence. Sunoco ended Q3 with no borrowings on its revolving credit facility, which was expanded to $2.5 billion following the Parkland transaction. As of Sept. 30, 2025, long-term debt stood at roughly $9.5 billion, with about $1.5 billion of liquidity still available. Net leverage was 3.9 times adjusted EBITDA.

Strategically, the completion of the company's Parkland acquisition marks a major milestone, creating the largest independent fuel distributor in the Americas. Management expects the deal to be immediately accretive, with more than $250 million in synergies targeted by 2028.

Sunoco’s 2026 outlook sets a confident, forward-looking tone. Management expects adjusted EBITDA of $3.1 billion to $3.3 billion, supported by roughly $125 million in Parkland synergies, disciplined capital spending, and steady acquisition-driven growth. With major maintenance planned, leverage returning to target levels, and distributions targeted to grow at least 5%, Sunoco is positioning for another year of rising cash flow and consistent returns.

Analysts tracking Sunoco expect its EPS for Q4 to increase 123% YOY to $1.67, with fiscal 2025 EPS to be around $3.76. Over the longer term, fiscal 2026 profit is projected to be $7.36 per share.

SUN stock has a consensus “Strong Buy” rating overall — an upgrade from the “Moderate Buy” rating a month back. Out of the seven analysts offering recommendations for the stock, six suggest a “Strong Buy" while one advises a “Moderate Buy.”

The average analyst price target of $64 suggests that SUN stock has 19% upside potential from current price levels. The Street-high price target of $70 indicates that the stock could rally as much as 30% from here.

Oil and Gas Stock #3: Cenovus Energy

Founded in 2009 and based in Calgary, Alberta, Cenovus Energy is a fully integrated Canadian oil and gas producer with deep roots in oil sands, conventional resources, and thermal projects. With operations spanning exploration through production, the company balances scale with discipline, while keeping sustainability, Indigenous reconciliation, and responsible development front and center. Today, Cenovus carries a market capitalization of about $33 billion.

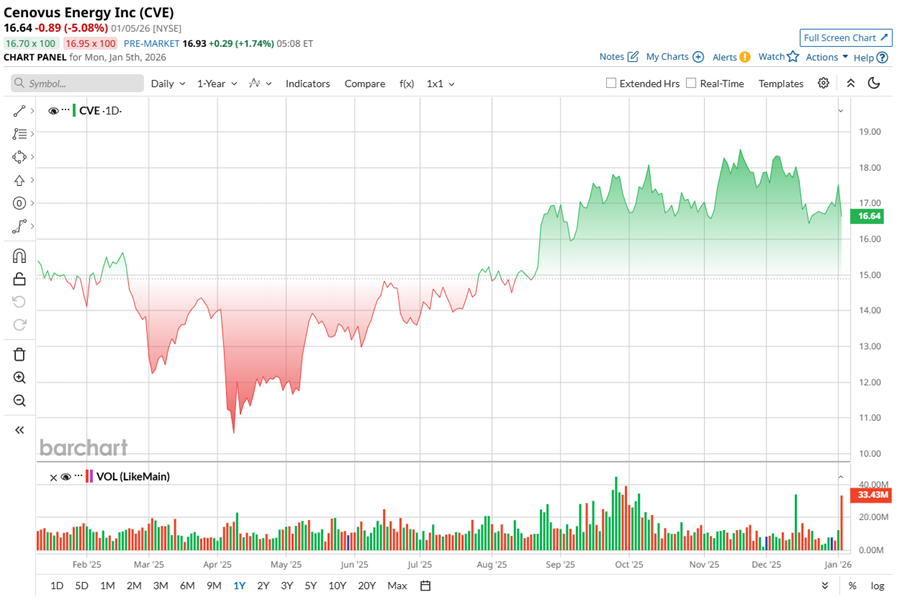

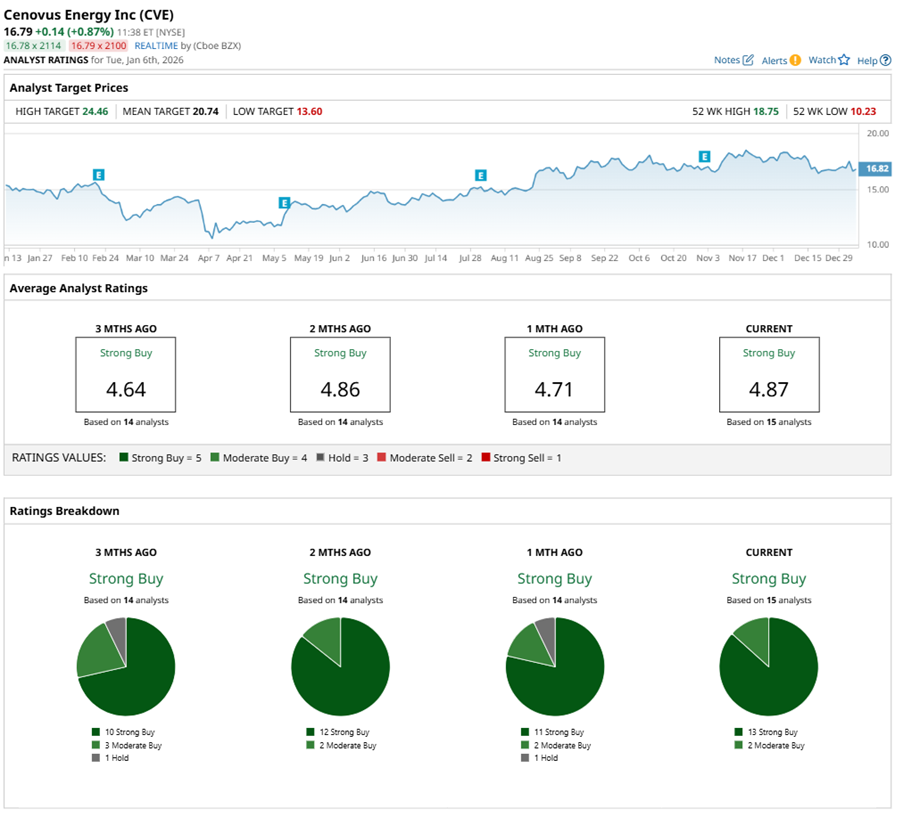

Shares of Cenovus Energy have taken a breather, sitting 16% below the 52-week high of $18.75. Still, the bigger picture looks steadier. Shares are up 1% over the past year and have climbed 12% in the last six months, suggesting momentum remains intact.

From a valuation angle, Cenovus Energy tells a steady, shareholder-friendly story. The stock trades at 11.9 times forward earnings and just 0.74 times forward sales, both sitting comfortably below sector averages.

That discount pairs well with a long-standing dividend track record. Cenovus has rewarded shareholders for 16-straight years, paying a forward annual dividend of $0.58 per share. That translates to a healthy 3.38% yield, while a manageable 43% payout ratio suggests the dividend is well supported and built to endure through commodity cycles.

Cenovus Energy’s fiscal Q3 update, released on Oct. 31, delivered a confident snapshot of execution across the business. The company beat Wall Street expectations on both the top and bottom line, with total revenue climbing to CA$13.2 billion and EPS rising to CA$0.72, comfortably ahead of projections.

Operationally, the quarter set records. Total upstream production reached 832,900 boepd, up sharply from 771,300 boepd a year earlier and marking the highest upstream output. That performance was driven by the Oil Sands segment, which posted record production of roughly 642,800 boepd. Downstream operations also impressed. Crude oil processed volumes rose to 605,300 barrels per day (bbls/d) versus 543,500 bbls/d last year.

Cenovus paired operating strength with shareholder returns, sending CA$1.3 billion back to investors during the quarter. This included CA$918 million in share buybacks and CA$356 million in dividends. As of Sept. 30, 2025, the company held CA$1.9 billion in cash, reflecting a solid financial position.

Looking ahead, management reaffirmed its 2025 outlook. Full-year upstream production is guided between 805,000 boped and 845,000 boepd, and capital spending is expected to be between CA$4.6 billion and CA$5 billion, signaling steady momentum into year-end.

Analysts tracking Cenovus Energy expect its profit per share for the quarter to increase 560% YOY to $0.33. Fiscal 2025 profit is expected to climb 26% YOY to $1.54 per share, then decline by 8% to $1.42 per share in fiscal 2026.

Sentiment remains firmly bullish. Cenovus holds a consensus “Strong Buy” rating, with 13 of the total 15 analysts backing it as a “Strong Buy” and two analysts calling CVE stock a “Moderate Buy.”

The average analyst price target of $20.74 indicates potential upside of 32% from current price levels. However, the Street-high price target of $24.46 suggests that the stock could rally as much as 56% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)