The Dow is climbing mid-session, up about 0.4%, while the S&P 500 is only slightly positive and the Nasdaq is dipping a bit. Traders brushed off the disappointing ADP report, instead betting that weaker employment data could increase the chances of an interest rate cut next week. Microsoft’s early decline threatened market sentiment, but buyers prevented major losses in other sectors. Russell futures found support at 2468.1 and moved higher, likely boosted by renewed attention from short-term traders reacting to the ADP data. This index, which has mostly been moving sideways or down recently, is getting another look. Technically, the Nasdaq Composite is consolidating within a range dating back to early November but remains above the 50-day moving average at 22985.38 and the near-term 50% retracement level at 22959.14, indicating an upward bias.

Are Indexes giving us a clear signal towards a potential rally into year-end? Not exactly, but the overall tone is cautiously optimistic. The Dow’s gains are stabilizing the market, even as tech stocks weigh on the Nasdaq. Microsoft dropped nearly 2% after reports of cutbacks in AI-related sales quotas, though the company denied these claims, resulting in a partial rebound. Still, the tech sector lagged, with Nvidia dipping slightly, Broadcom falling over 1%, and Micron down more than 1% as AI stocks cooled off. While sellers pressured technology shares, buyers stepped in elsewhere to balance things out. Energy is leading, up 1.6%, while financials and consumer discretionary stocks are also attracting solid interest. Industrials and health care are performing well too. On the downside, tech is down 0.36%, with real estate and utilities trailing. In summary, traders are rotating into cyclical stocks and sectors that stand to benefit from a potential rate cut — it’s a classic “search for value” day, supported by hopes that slowing job growth will prompt the Fed to ease policy. What about the restart of data from the government? Is the ADP weaker jobs report having any effect outside of the reactionary trades past the open today? Quite a lot, but traders are interpreting it positively. ADP showed a drop of 32,000 private payrolls versus an expected gain of 40,000. Normally, such a miss would dampen risk appetite, but with the Fed meeting coming up and rate-cut odds at around 89%, the market sees the softness as further reason for easing. Traders are rooting for a cut, and the jobs data supports that outlook. However, today’s slightly better-than-expected ISM services report helped temper recession worries, encouraging dip buyers. Traders are hopeful the Fed will deliver a rate cut next week, and today’s news fits that narrative. As long as cyclicals continue to attract buying and tech weakness doesn’t spread, the market is likely to hold its current momentum through the close.

The primary focus now is every rumor about the December 10 Fed decision. Buyers are interested but not overly aggressive; they want to be positioned if the Fed finally signals a shift. Here are snapshots of some directional trades we have placed today in the options market, which understandably, isn't for every portfolio. The key here is to know how far an intraday move can push after one as pinpointed the support zone especially after data releases off the economic calendar. Come give us a spin, we are in the process of delivering an options service as an add-on to our current "futures only" alerts. It may change how you look at your trading and investment goals.

Actual NDX options trades

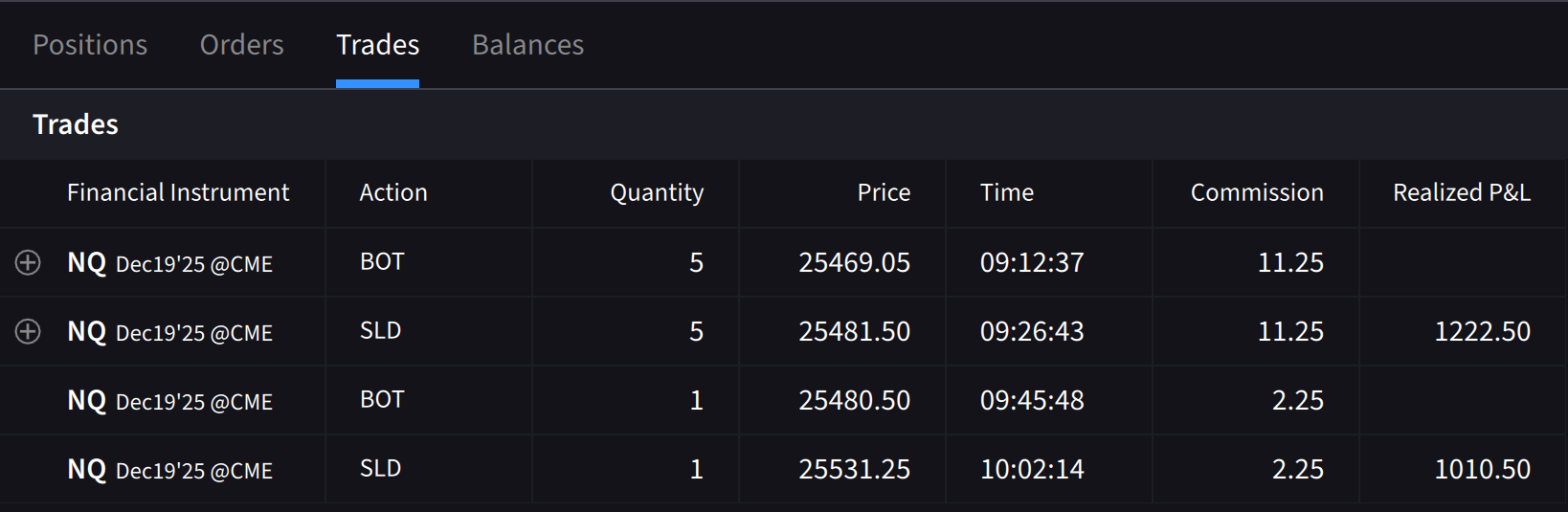

Actual futures trades

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)